14.3: Sinking Fund Schedules

- Page ID

- 22154

Individuals and businesses should always plan to save toward their future goals. A sinking fund represents one way of accomplishing this, earning interest while regular contributions build up, all to reach a specified target at the end of the period.

For instance, let’s say you are a production manager. In your desk inbox a consultant’s report warns about the worrisome state of your production facilities and warehousing operations. Because your current production machinery is really showing its age, you need to replace it within three years. Meanwhile, increasing demand makes a new warehouse in Scarborough necessary within five years. The costs of each project are forecast at $1 million and $3 million, respectively. You see in the financial reports for the company that your company averages annual net profits of about $750,000. Your company needs to start setting aside the required funds now for these urgent projects.

On your way home, you pass by a newly constructed residential neighborhood. You have your eye on a starter home there with a list price of approximately $325,000. The 5% down payment required by the mortgage lender is $16,250. You have been making end-of-month contributions of $239 for the past four years into a savings plan earning 5% compounded monthly. On a whim, you head into the development, where you find a show home currently on the market for $250,000. You are quite smitten with the home and know that it will not take long to sell. Before putting in an offer, you wonder if your savings plan has enough funds to meet the 5% down payment requirement today.

Sinking Funds

A sinking fund is a special account into which an investor, whether an individual or a business, makes annuity payments such that sufficient funds are on hand by a specified date to meet a future savings goal or debt obligation. In its simplest terms, it is a financial savings plan. As the definition indicates, it has either of two main purposes:

- Capital Savings. When your goal is to acquire some form of a capital asset by the end of the fund, you have a capital savings sinking fund. What is a capital asset? It is any tangible property that is not easily converted into cash. Thus, saving up to buy a home, car, warehouse, or even new production machinery qualifies as capital savings.

- Debt Retirement. When your goal is to pay off some form of debt by the end of the fund, then you have a debt retirement sinking fund. Perhaps as a consumer if you were able to get a 0% interest plan with no payments for one year; you might want to make monthly payments into your own savings account such that you would have the needed funds to pay off your purchase when it comes due. Businesses usually set up these funds for the retirement of stocks, bonds, and debentures.

Whether the sinking fund is for capital savings or debt retirement, the mathematical calculations and procedures are identical. Now, why discuss sinking funds in the chapter about bonds? Many bonds carry a sinking fund provision. Once the bond has been issued, the company must start regular contributions to a sinking fund because large sums of money have been borrowed over a long time frame; investors need assurance that the bond issuer will be able to repay its debt upon bond maturity. For example, in the chapter opener the profits needed to repay the financing for the Bipole III project will not just miraculously appear in the company's coffers. Instead, over a period of time the company will accumulate the funds through saved profits.

To provide further assurance to bondholders, the sinking fund is typically managed by a neutral third party rather than the bond-issuing company. This third-party company ensures the integrity of the fund, working toward the debt retirement in a systematic manner according to the provisions of the sinking fund. Investors much prefer bonds or debentures that are backed by sinking funds and third-party management because they are less likely to default.

In the case of bonds or debentures, sinking funds are most commonly set up as ordinary simple annuities that match the timing of the bond interest payments. Thus, when a bond issuer makes an interest payment to its bondholders, it also makes an annuity payment to its sinking fund. In other applications, any type of annuity is possible, whether ordinary or due and general or simple.

Complete Ordinary Sinking Fund Schedules

A complete sinking fund schedule is a table that shows the sinking fund contribution, interest earned, and the accumulated balance for every payment in the annuity. It is very similar to an amortization schedule except that (1) the balance increases instead of decreasing, and (2) the interest is being earned instead of being paid.

The Formula

To complete the sinking fund schedule, you must calculate the interest earned and thus apply Formula 13.1, which calculates the interest portion of a single payment:

\[INT=BAL \times\left((1+i)^{\frac{CY}{PY}}-1\right) \nonumber \]

Aside from that formula, the table is mathematically simple, requiring only basic addition.

How It Works

Follow these steps to develop a complete sinking fund schedule:

Step 1: Draw a timeline. Identify all of your time value of money variables (\(N, IY, FV_{ORD}, PMT, PV, PY, CY\)). If either \(N\) or \(PMT\) is unknown, solve for it using an appropriate formula. Remember to round \(PMT\) to two decimals.

Step 2: Set up a sinking fund schedule following the template below, (the cells are marked with the step numbers that follow). The number of payment rows in your table is equal to the number of payments in the annuity (\(N\)).

| Payment Number |

Payment Amount at End ($) (\(PMT\) |

Interest Earned or Accrued ($) (\(INT\)) |

Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| 0 - Start | N/A | N/A | (3) |

| 1 | (4) | (5) | (6) |

| ... | |||

| Last Payment | |||

| Total | (9) | (9) | N/A |

Step 3: Fill in the present value of the annuity (\(PV\)). You typically start with a zero balance when you save toward a future goal, although sometimes you may make an immediate lump-sum deposit to start the account.

Step 4: Fill in the rounded annuity payment (\(PMT\)) all the way down the column, including the final payment row.

Step 5: Calculate the interest portion of the sinking fund’s current balance (\(INT\)) using Formula 13.1. Round the number to two decimals for the table, but keep track of all decimals throughout.

Step 6: Calculate the new balance by taking the previous un-rounded balance on the line above and adding both the annuity payment and the un-rounded interest on the current row. Round the result to two decimals for the table, but keep track of all decimals for future calculations.

Step 7: Repeat steps 5 and 6 for each annuity payment until the schedule is complete.

Step 8: Since all numbers are rounded to two decimals throughout the table, check the table for the "missing penny.” This is the same "missing penny" concept as discussed in the Chapter 13 amortization schedules. Ensure that previous balances plus current payments and interest equal the new balance. If not, adjust the interest earned amount as needed. Do not adjust the balance in the account or the payment. Make as many penny adjustments as needed; they typically appear in pairs such that when you must increase one line by one penny, another subsequent line reduces the interest by one penny.

Step 9: Total up the principal payments made and interest earned for the entire schedule.

Important Notes

When you work with sinking fund schedules, remember three key considerations with respect to the annuity type, final payment adjustment, and the rounding of the sinking fund payment:

- You can use the ordinary sinking fund schedule for both simple and general annuities.

- Under a simple sinking fund, the payments and interest always occur together on the same line of the schedule, which raises no complications of realized versus accrued interest.

- However, for the general annuity, although you could create a table where interest is converted to principal between each annuity payment, it makes no fundamental or mathematical difference in the balance of the fund at any given time. Therefore, this textbook’s sinking fund schedules reflect the interest earned regardless of whether it has been converted to principal or remains in accrued format as of each annuity payment date.

- You are not legally required to be precise when saving up for a future goal. You do not need to adjust the final payment to bring the sinking fund to an exact balance. If the account balance is marginally below or above the goal, you can either top it up as needed or use the extra funds for another purpose.

For the above reason, the sinking fund annuity payment amount is frequently rounded off to a convenient whole number. In this textbook you will be clearly instructed if such rounding is to occur; otherwise, use the exact annuity payment rounded to two decimals.

Your BAII Plus Calculator

Although the calculator has no function called "sinking fund," sinking funds have the same characteristics as amortization schedules. Therefore, use the AMORT function located on the 2nd shelf above the \(PV\) key to create the sinking fund schedule. You can find full instructions for the AMORT function in Chapter 13. The key difference in using this function for sinking funds is that the principal grows instead of declines.

With respect to the cash flow sign convention, your \(PV\) (if not zero) and \(PMT\) are negative, since money is being invested into the account. The \(FV\) is a positive number, since it can be withdrawn in the future. As in Chapter 13, you need to input all time value of money buttons accurately before accessing this function.

The \(BAL\) and \(INT\) outputs are accurate and true to definition. The \(BAL\) represents the balance in the fund. The \(INT\) represents the interest earned for the specified payments. The \(PRN\) output is also accurate, but its definition is changed to represent the total of the annuity payments made and the interest earned. It represents the total increase in the balance of the fund over the course of the specified payments.

In an amortization schedule, the interest portion for each payment steadily declines with each annuity payment. What do you think happens to the interest earned with each payment in a sinking fund?

- Answer

-

It steadily gets larger since the principal balance is increasing instead of decreasing.

The City of Winnipeg issued a $500,000 face value bond with three years until maturity. It will make contributions at the end of every six months to a sinking fund earning 5.8% compounded semi-annually. Construct a complete sinking fund schedule and calculate the total principal contributions and interest components. Add text here.

Solution

You are to construct a complete sinking fund schedule for the bond. The schedule needs to provide the total principal contributions, which is the same as the total payments (\(PMT\)) made to the fund, as well as the total interest (\(INT\)) earned.

What You Already Know

Step 1:

The timeline for the City of Winnipeg’s sinking fund appears below.

\(FV_{ORD}\) = $500,000, \(IY\) = 5.8%, \(CY\) = 12, \(PY\) = 2, Years = 3, \(PV\) = $0

How You Will Get There

Step 1 (continued):

Solve for the ordinary sinking fund annuity payment (\(PMT\)) using Formulas 9.1, 11.1, and 11.2 (rearranging for \(PMT\)).

Step 2:

Set up the sinking fund schedule.

Steps 3 and 4:

Fill in the original principal with zero (since this is the opening balance) and payment column with the \(PMT\) from step 1.

Steps 5 to 7:

Use Formula 13.1 to calculate the interest and add the row to get the new balance for each line.

Step 8:

Check for the "missing penny."

Step 9:

Sum the interest portion as well as the total payments for the principal contribution.

Perform

Step 1 (continued):

\(i=5.8 \% / 2=2.9 \% ; N=2 \times 3=6\) payments

\[\$ 500,000=PMT\left[\dfrac{\left((1+0.029)^{\frac{2}{2}}\right]^{6}-1}{(1+0.029)^{\frac{2}{2}}-1}\right] \nonumber \]

\[PMT=\dfrac{\$ 500,000}{\left[\dfrac{\left[(1+0.029)^{\frac{2}{2}}\right]^{6}-1}{(1+0.029)^{\frac{2}{2}}-1}\right]}=\$ 77,493.07 \nonumber \]

Steps 2 to 7 (with some calculations) are detailed in the table below.

| Payment Number | Payment Amount at End ($) (\(PMT\)) | Interest Earned or Accrued ($) (\(INT\)) | Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| 0 - Start | $0.00 | ||

| 1 | $77,493.07 | (1) $0.00 | (2) $77,493.07 |

| 2 | $77,493.07 | (3) $2,247.30 | (4) $157,233.44 |

| 3 | $77,493.07 | (5) $4,559.77 | (6) $239,286.28 |

| 4 | $77,493.07 | $6,939.30 | $323,718.65 |

| 5 | $77,493.07 | $9,387.84 | $410,599.56 |

| 6 | $77,493.07 | $11,907.39 | $500,000.02 |

| Total | $464,958.42 | $35,041.60 |

(1) \(\text { INT }=\$ 0 \times\left((1+0.029)^{\frac{2}{2}}-1\right)=\$ 0\)

(2) \(\text { New Balance }=\$ 0.00+\$ 77,493.07+\$0.00=\$ 77,493.07 \)

(3) \(\text { INT }=\$ 77,493.07 \times\left((1+0.029)^{\frac{2}{2}}-1\right)=\$ 2,247.298945\)

(4) \(\text { New Balance }=\$ 77,493.07+\$ 77,493.07+\$ 2,247.298945=\$ 157,233.4389\)

(5) \(\text { INT }=\$ 157,233.4389 \times\left((1+0.029)^{\frac{2}{2}}-1\right)=\$ 4,559.769729 \)

(6) \(\text { New Balance }=\$ 157,233.4389+\$ 77,493.07+\$ 4,559.769729=\$ 239,286.28 \)

Steps 8 to 9:

There are no rounding errors and the table is correct. Total the interest and principal contributions.

Calculator Instructions

| Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| END | 6 | 5.8 | 0 |

Answer: -77,493.06705 Rekeyed as -77493.07 |

500000 | 2 | 2 |

| Payment | P1 | P2 | BAL (Output) | INT (Output) |

|---|---|---|---|---|

| 1 | 1 | 1 | -77,493.07 | 0 |

| 2 | 2 | 2 | -157,233.439 | 2,247.29903 |

| 3 | 3 | 3 | -239,286.2788 | 4,559.769732 |

| 4 | 4 | 4 | -323,718.6508 | 6,939.302084 |

| 5 | 5 | 5 | -410,599.5617 | 9,387.840875 |

| 6 | 6 | 6 | -500,000.019 | 11,907.38729 |

| Total | 1 | 6 |

-500,000.19 Note: Total contributions are \(PMT \times 6\) |

35,041.59901 |

The complete sinking fund schedule is shown in the table above. The total interest earned by the City of Winnipeg is $35,041.60 in addition to the $464,958.42 of principal contributions made. Note that the fund has an extra $0.02 in it after the three years.

Partial Ordinary Sinking Fund Schedules

For the same reasons as with amortization schedules, sometimes you are interested in creating partial sinking fund schedules for a specified range of payments and not the entire sinking fund. This may be because of any of the following reasons:

- The sinking fund schedule is too long.

- Your sole interest is in the interest portion during a specific period of time for accounting and tax purposes.

- You are assisting in the financial planning of the individual or organization at a particular point in time.

How It Works

For a partial sinking fund schedule, follow almost the same procedure as for a complete sinking fund schedule, with the following notable differences:

Step 2: Set up the partial sinking fund schedule according to the template provided here. The table identifies the corresponding step numbers.

Step 3: Calculate the balance accumulated in the account immediately before the first payment of the partial schedule. Recall the three calculations required to determine this value:

| Payment Number |

Payment Amount at End ($) (\(PMT\)) |

Interest Earned or Accrued ($) (\(INT\)) |

Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| Preceding Payment # | N/A | N/A | (3) |

| First Payment Number of Partial Schedule | (4) | (5) | (6) |

| ... | |||

| Last Payment Number of Partial Schedule | |||

| Total | (9) | (9) | N/A |

- Calculate the future value of the original principal. Use Formulas 9.1 (Periodic Interest Rate), 9.2 (Number of Compounding Periods for Single Payments), and 9.3 (Compound Interest for Single Payments).

- Calculate the future value of all annuity payments already made. Apply Formulas 11.1 (Number of Annuity Payments) and 11.2 (Ordinary Annuity Future Value).

- Sum the above two calculations to arrive at the principal balance (BAL) immediately before the first payment required in the partial sinking fund schedule.

Things To Watch Out For

When you use Excel to create amortization schedules, recall that your template does not correct for the “missing penny.” The situation is no different with respect to sinking fund schedules. Therefore, a schedule generated using the Excel template may have the occasional penny difference on any given line since each displayed number is rounded to two decimals, but the total interest and total principal are always correct since the un-rounded numbers are used in their calculations.

The Alberta Capital Finance Authority (ACFA) issued a $200,000 face value bond with five years until maturity. The sinking fund provision requires payments to be made at the end of every quarter into a fund earning 4.4% compounded quarterly. Create a partial sinking fund schedule for the third year. Calculate the total interest earned and total contributions made in the third year.

Solution

You are to construct a partial sinking fund schedule for the third year of the loan along with the total interest earned and total contributions for the year.

What You Already Know

Step 1:

The timeline for the bond appears below.

\(FV_{ORD}\) = $200,000, \(IY\) = 4.4%, \(CY\) = 4, \(PY\) = 4, Years = 5, \(PV\) = $0

How You Will Get There

Step 1 (continued):

Solve for the ordinary sinking fund annuity payment (\(PMT\)) using Formulas 9.1, 11.1, and 11.2 (rearranging for \(PMT\)).

Step 2:

Set up the partial sinking fund schedule according to the template.

Step 3:

There is no single payment at the beginning (\(PV\) = $0). Calculate just the future value of the first eight annuity payments using Formulas 11.1, and 11.2. The balance in the account prior to the third year is equal to the \(FV_{ORD}\).

Step 4:

Fill in the payment column for the four payments made in the third year.

Steps 5 to 7:

Use Formula 13.1 to calculate interest and add the row to get the new balance for each line.

Step 8:

Check for the "missing penny."

Step 9:

Total up the interest portion as well as the total payments for the principal contribution.

Perform

Step 1 (continued):

\(i=4.4 \% / 4=1.1 \% ; N=4 \times 5=20 \) payments

\[\$ 200,000=PMT\left[\dfrac{\left[(1+0.011)^{\frac{4}{4}}\right]^{20}-1}{(1+0.011)^{\frac{4}{4}}-1}\right] \nonumber \]

\[PMT=\dfrac{\$ 200,000}{\left[\dfrac{\left[(1+0.011)^{\left.\frac{4}{4}\right]^{20}-1}-1\right.}{(1+0.011)^{\frac{4}{4}}-1}\right]}=\$ 8,994.98 \nonumber \]

Steps 2 to 7 (with some calculations, including step 3) are detailed in the table below.

| Payment Number |

Payment Amount at End ($) (\(PMT\)) |

Interest Earned or Accrued ($) (\(INT\)) |

Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| 8 | (1) $74,792.09 | ||

| 9 | $8,994.98 | (2) $822.71 | (3) $84,609.78 |

| 10 | $8,994.98 | $930.71 | $94,535.47 |

| 11 | $8,994.98 | $1,039.89 | $104,570.34 |

| 12 | $8,994.98 | $1,150.27 | $114,715.59 |

| Total | $35,979.92 | $3,943.58 |

(1) Step 3:

\(N=4 \times 2=8\) payments;

\(FV_{ORD}=\$8,994.98\left[\dfrac{\left[(1+0.011)^{\frac{4}{4}}-1\right]}{(1+0.011)^{\frac{4}{4}}-1}\right]=\$ 8,994.98\left[\dfrac{0.091463}{0.011}\right]=\$ 74,792.0893\)

(2) \(INT=\$ 74,792.0893 \times\left((1+0.011)^{\frac{4}{4}}-1\right)=\$ 822.712982 \)

(3) \(\text { New Balance }=\$ 74,792.0893+\$ 8,994.98+\$ 822.712982=\$ 84,609.78229 \)

Steps 8 to 9:

In this case there are no rounding errors and the table above is correct. Total the interest and principal contributions.

Calculator Instructions

| Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| END | 20 | 4.4 | 0 |

Answer: -8,994.980862 Re-keyed as -8994.98 |

200000 | 4 | 4 |

| Payment | P1 | P2 | BAL (Output) | INT (Output) |

|---|---|---|---|---|

| 8 | 8 | 8 | -74,792.0893 | Not needed |

| 9 | 9 | 9 | -84,609.78228 | 822.712982 |

| 10 | 10 | 10 | -94,535.46989 | 930.707605 |

| 11 | 11 | 11 | -104,570.3401 | 1,039.890169 |

| 12 | 12 | 12 | -114,715.5938 | 1,150.273741 |

| Total | 9 | 12 |

-114,715.5938 Note: Total contributions are \(PMT \times 4\) |

3943.584497 |

The partial sinking fund schedule for the third year is shown in the table above. ACFA contributed $35,979.92 to the fund and earned total interest of $3,943.58.

Sinking Funds Due Schedules

While ordinary sinking funds are typical for bonds, capital savings sinking funds can take any form. Whether saving personally for the down payment on a house or saving at work for the acquisition of a warehouse, the investor determines the timing of the annuity payments. Sinking funds due require a small modification to the headers in the sinking fund due schedule, as illustrated in the table. Recall that the payment occurs at the beginning of the payment interval.

| Payment Number |

Payment Amount at BGN ($) (\(PMT\)) |

Interest Earned or Accrued ($) (\(INT\)) |

Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| 0 - Start | N/A | N/A | (3) |

| 1 | (4) | (5) | (6) |

| ... | |||

| Last Payment | |||

| Total | (9) | (9) | N/A |

- Ensure that any unknown variables like \(PMT\) are calculated by an annuity due formula.

- The first payment occurs at the beginning of the first time period. Hence, this first payment receives interest, unlike the first payment in an ordinary annuity, which receives no interest during the first time period because it is paid at the end.

In accordance with the practice for previous schedules, do not distinguish between earned and accrued interest for general sinking funds due. Both amounts are represented in the third column of the table. If you need a partial sinking fund due schedule, its structure is the same as the table for ordinary sinking funds, although the headers change to match the table above.

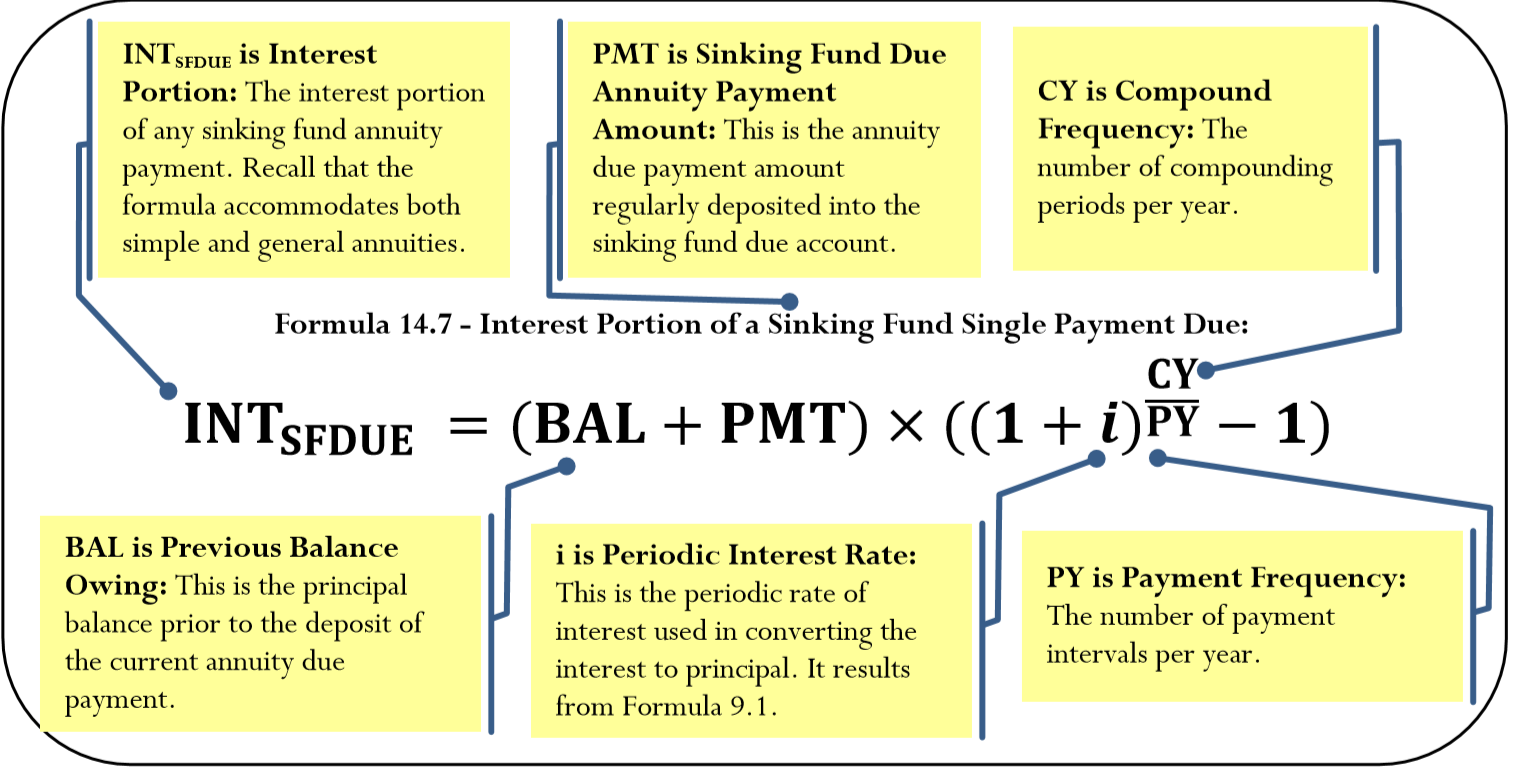

The Formula

Calculating the interest portion in a sinking fund due schedule requires a slight modification to Formula 13.1 for the interest portion of a single payment. In an annuity due, the payment is deposited at the beginning of the payment interval and therefore accrues interest during the current payment interval. This means that you must add the annuity payment to the previous balance before calculating interest.

How It Works

The steps for creating either a complete or partial sinking fund due schedule remain much the same as for an ordinary sinking fund schedule. You require the following adaptations:

- Step 2: Use the sinking fund due table instead of ordinary sinking fund table.

- Step 5: Use Formula 14.7 instead of Formula 13.1.

Important Notes

Your BAII Plus Calculator.

Probably the most significant change occurs here. The AMORT function is designed only for ordinary amortization, but you can easily adapt it to sinking funds due. These changes are similar to the adaptations required for amortization schedules due.

- P1 and P2: In a sinking fund due, since the first payment occurs today (time period 0), the second payment is at time period 1, and so on. So the payment number of a sinking fund due is always one higher than the payment number of an ordinary sinking fund; always add 1 to the payment number being calculated. For example, if interested only in payment seven, set both P1 and P2 to 8. Or if interested in the payment range 14 through 24, set P1 = 15 and P2 = 25.

- BAL: To generate the output, the payment numbers are one too high. This results in the balance being increased by one extra payment. To adapt, manually decrease the balance by removing one payment (or with BAL on your display, use the shortcut key sequence of − RCL PMT =).

- INT and PRN: Both of these numbers are correct. Recall that PRN reflects the sinking fund payment (\(PMT\)) and interest amount (\(INT\)) together.

In an effort to be more environmentally friendly, Bernard is considering leasing a Chevrolet Volt. The lease terms require a down payment of $2,000. To save up, Bernard starts making quarterly contributions today for the next year into a fund earning 5.3% semi-annually. Create a sinking fund due schedule and calculate his total payments and interest.

Solution

You are to construct a complete sinking fund due schedule for car savings along with the total interest (\(INT)\) and total principal contributions, or the total payments (\(PMT\)) made to the fund.

What You Already Know

Step 1:

The timeline for the car down payment savings plan appears below.

\(FV_{DUE}\) = $2,000, \(IY\) = 5.3%, \(CY\) = 2, \(PY\) = 4, Years = 1, \(PV\) = $0

How You Will Get There

Step 1 (continued):

Solve for the sinking fund due annuity payment (\(PMT\)) using Formulas 9.1, 11.1, and 11.3 (rearranging for \(PMT\)).

Step 2:

Set up the sinking fund due schedule.

Steps 3 and 4:

Fill in the original principal with zero (since this is the opening balance) and the payment column with the \(PMT\) from step 1.

Steps 5 to 7:

Use Formula 14.7 to calculate interest and add the row to get the new balance for each line.

Step 8:

Check for the "missing penny."

Step 9:

Total up the interest portion as well as the total payments for the principal contribution.

Perform

Step 1 (continued):

\(i=5.3 \% / 2=2.65 \% ; N=4 \times 1=4\) payments

\[\$ 2,000=PMT\left[\dfrac{\left[(1+0.0265)^{\frac{2}{4}}\right]^{4}-1}{(1+0.0265)^{\frac{2}{4}}-1}\right] \times(1+0.0265)^{\frac{2}{4}} \nonumber \]

\[PMT=\dfrac{\$ 2,000}{\left[\dfrac{\left.(1+0.0265)^{\frac{2}{4}}\right]^{4}-1}{(1+0.0265)^{\frac{2}{4}}-1}\right] \times(1+0.0265)^{\frac{2}{4}}}=\$ 483.87 \nonumber \]

Steps 2 to 7 (with some calculations) are detailed in the table below:

| Payment Number |

Payment Amount at BGN ($) (\(PMT\)) |

Interest Earned or Accrued ($) (\(INT\)) |

Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| 0 - Start | $0.00 | ||

| 1 | $483.87 | (1) $6.37 | (2) $490.24 |

| 2 | $483.87 | (3) $12.82 | (4) $986.93 |

| 3 | $483.87 | $19.36 | $1,490.16 |

| 4 | $483.87 | $25.98 | $2,000.02 |

| Total |

(1) \(INT_{\mathrm{SFDUE}}=(\$ 0+\$ 483.87) \times\left((1+0.0265)^{\frac{2}{4}}-1\right)=\$ 6.369356\)

(2) \(\text { New Balance }=\$ 0.00+s 483.87+\$ 6.369356=\$ 490.239356 \)

(3) \(\text { INT}_{SFDUE }=(\$ 490.239356+\$ 483.87) \times\left((1+0.0265)^{\frac{2}{4}}-1\right)=\$ 12.822555\)

(4) \(\text { New Balance }=\$ 490.239356+\$ 483.87+\$ 12.822555=\$ 986.931911 \)

Steps 8 to 9:

Adjust for the "missing pennies" (noted in red) and total the payments and interest.

| Payment Number |

Payment Amount at BGN ($) (\(PMT\)) |

Interest Earned or Accrued ($) (\(INT\)) |

Principal Balance Accumulated at End of Payment Interval ($) (\(BAL\)) |

|---|---|---|---|

| 0 - Start | $0.00 | ||

| 1 | $483.87 | (1) $6.37 | (2) $490.24 |

| 2 | $483.87 | (3) $12.82 | (4) $986.93 |

| 3 | $483.87 | $19.36 | $1,490.16 |

| 4 | $483.87 | $25.98 | $2,000.02 |

| Total | $1,935.48 | $64.54 |

Calculator Instructions

| Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| BGN | 4 | 5.3 | 0 |

Answer: -483.865761 Rekeyed as -483.87 |

2000 | 4 | 2 |

| Payment | P1 | P2 | BAL (Output) | INT (Output) |

|---|---|---|---|---|

| 1 | 2 | 2 | -490.239356 | 6.369 |

| 2 | 3 | 3 | -986.931911 | 12.822555 |

| 3 | 4 | 4 | -1,490.162611 | 19.360699 |

| 4 | 5 | 5 | -2,000.017519 | 25.984907 |

| Total | 2 | 5 | -2,000.017519 | 64.537518 |

The complete sinking fund due schedule is shown in the table above. The total interest earned by Bernard is $64.54 in addition to the $1,935.48 of principal contributions made. Note that the fund has an extra $0.02 in it because of rounding.