5.S: Marketing and Accounting Fundamentals (Summary)

- Page ID

- 22092

Key Concepts Summary

5.1: Cost-Revenue-Net Income Analysis (Need to Be in the Know)

- The three different types of costs

- How to determine the unit variable cost

- Calculating net income when you know total revenue and total cost

- Calculating net income when you know the contribution margin

- Comparing varying contribution margins by calculating a contribution rate

- Integrating all of the concepts together

5.2: Break-Even Analysis (Sink or Swim)

- Explanation of break-even analysis

- How to calculate the break-even point expressed in the level of output

- How to calculate the break-even point expressed in total revenue dollars

The Language of Business Mathematics

- blended cost

-

A cost that comprises both fixed cost and variable cost components.

- break-even analysis

-

An analysis of the relationship between costs, revenues, and net income with the sole purpose of determining the point at which total revenue equals total cost.

- break-even point

-

A quantity that represents the level of output (in units or dollars) at which all costs are paid but no profits are earned, resulting in a net income equal to zero.

- contribution margin

-

The amount each unit sold adds to the net income of the business.

- contribution rate

-

A contribution margin expressed as a percentage of the selling price.

- cost

-

An outlay of money required to produce, acquire, or maintain a product, which includes both physical goods and services.

- economies of scale

-

The principle that, as production levels rise, per-unit variable costs tend to become lower as efficiencies are achieved.

- fixed cost

-

A cost that does not change with the level of production or sales.

- net income

-

The amount of money left over after all costs are deducted from all revenues.

- total fixed cost

-

The sum of all fixed costs that a business incurs.

- total cost

-

The sum of all costs for the company, including both the total fixed costs and total variable costs.

- total revenue

-

The entire amount of money received by a company for selling its product, calculated by multiplying the quantity sold by the selling price.

- total variable cost

-

The sum of all variable costs that a business incurs at a particular level of output.

- unit variable cost

-

The assignment of total variable costs on a per-unit basis.

- variable cost

-

A cost that changes with the level of production or sales.

The Formulas You Need to Know

Symbols Used

\(CM\) = unit contribution margin

\(CR\) = contribution rate

\(n\) = number of pieces of data, which in this chapter is the level of output

\(NI\) = net income

\(S\) = unit selling price of the product

\(TFC\) = total fixed cost

\(TR\) = total revenue

\(TVC\) = total variable cost

\(VC\) = unit variable cost

Formulas Introduced

Formula 5.1 Unit Variable Cost: \(VC=\dfrac{TVC}{n}\)

Formula 5.2 Net Income Using a Total Revenue and Cost Approach: \(NI=n(S)-(TFC+n(VC))\)

Formula 5.3 Unit Contribution Margin: \(CM=S-VC\)

Formula 5.4 Net Income Using Total Contribution Margin Approach: \(NI=n(CM)-TFC\)

Formula 5.5 Contribution Rate if Unit Information Is Known: \(CR=\dfrac{CM}{S} \times 100\)

Formula 5.6 Contribution Rate if Aggregate Information Is Known: \(CR=\dfrac{TR-TVC}{TR} \times 100\)

Formula 5.7 Unit Break-Even: \(n=\dfrac{TFC}{CM}\)

Formula 5.8 Dollar Break-Even: \(TR=\dfrac{TFC}{CR}\)

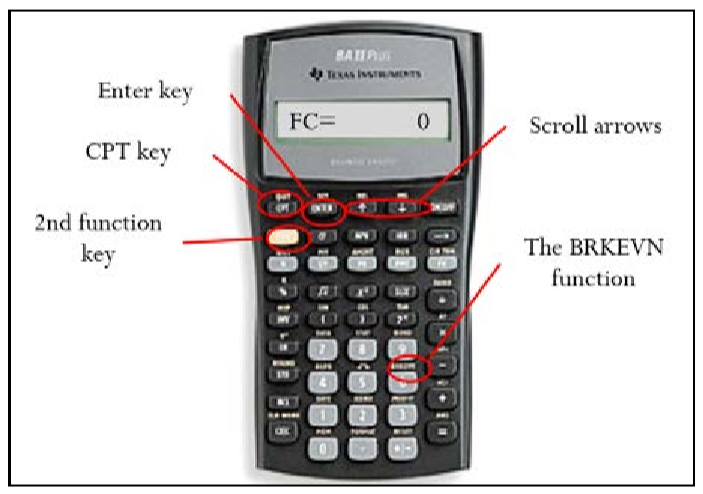

Technology

Calculator

Net Income or Break-Even

- 2nd Brkevn to open the function

- To clear the memory before entering any data, press 2nd CLR Work after opening the function. Use and to scroll through the function.

- Enter four of the following variables and press Enter after each to save:

\(FC\) = Total fixed costs

\(VC\) = Unit variable cost

\(P\) = Selling price per unit

\(PFT\) = Net income

\(Q\)= Level of output

- Press CPT on the unknown variable (when it is on the screen display) to compute.