10.1: Application - Long-Term GICs

- Page ID

- 22124

Recall that Guaranteed Investment Certificates (GICs) are investments offering a guaranteed rate of interest over a predetermined time period. Whereas short-term GICs in Section 8.3 involved terms less than one year, most long-term GICs range from one to five years. Though terms longer than this are available, they are not very common.

Also recall that Section 8.3 discussed the factors that determine interest rates for short-term GICs. The same factors apply to long-term GICs: To receive the highest interest rate on a GIC, you should still invest a large principal in a non-redeemable GIC for the longest term possible.

The key difference between short- and long-term GICs lies in the compounding of interest. Long-term GICs do not wait until the end of the term for interest on them to appear and be paid out. Rather, in line with the definition of compound interest, a long-term GIC periodically converts the accrued interest into principal throughout the transaction. Although GICs come in many varieties (remember, financial institutions try to market these products attractively to investors), three structures are commonly available:

- Interest Payout GICs. An interest payout GIC uses interest rates that by all appearances you might assume to be compounded periodically since they are listed side-by-side with compound interest rates. In practice, though (and by reading the fine print), you will find that the periodically calculated interest is never added to the principal of the GIC, and in essence the concepts of simple interest are used. Instead, the interest is paid out to the investor (perhaps into a chequing account) and does not actually compound unless the investor takes the interest payment received and invests it in another compounding investment. Interest payout GIC interest rates can take either a fixed or variable format. For example, in an online browsing of long-term GICs you may find a posted rate on a three-year GIC at 2% semi-annually. The fine print and footnotes may show that the interest is paid out on a simple interest basis at the end of each six months.

- Compound Interest GICs. A compound interest GIC uses compound interest rates for which interest is periodically calculated and converted to the principal of the GIC for further compounding. Interest rates can be either fixed or variable.

- Escalator Interest GICs. An escalator interest GIC uses compound interest rates that usually remain constant during each of a series of time intervals, always rising stepwise throughout the term of the investment with any accrued interest being converted to principal.

When you invest in a GIC, you are in essence lending the bank your money in return for earning an interest rate. Financial institutions commonly use the money raised from GICs to fund mortgages. As a result, the posted interest rates on GICs hover at 1% to 2% lower than the interest rates on mortgages. Thus, the bank earns the interest from its mortgagors, paying only a portion of it to its GIC investors. The rest of this section discusses each of the three types of GICs separately.

Interest Payout GIC

The interest payout GIC is mathematically the least interesting of the three types of GICs since the interest, while periodically calculated based on compound interest rates, does not get converted to principal. Instead, the interest payment is paid out to an account specified by the investor. Therefore, usually the only variable of concern on an interest payout GIC is the amount of the interest payment.

As a source of confusion, in the marketplace many financial institutions refer to interest payout GICs as simple interest GICs, because the interest never converts to principal. Examining bank websites such as CIBC (www.cibc.com/ca/gic/index.html), TD Canada Trust (www.tdcanadatrust.com/GICs/index.jsp), or HSBC (www.hsbc.ca/1/2/en/personal/investing-retiring/gics) reveals a variety of long-term GICs referred to as using simple interest. Why do these GICs then appear in this chapter and not previously in Chapter 8? The answer is threefold:

- Periodic Interest Payments. In interest payout GICs, interest is periodically paid out throughout the term of the GIC. This differs from the GICs discussed in Chapter 8 in that simple interest required interest to be calculated and added to the principal only at the end of the transaction's time period.

- Rates Used in Calculating the Interest Amount. In interest payout GICs, the posted rates appear intermixed with the posted compound interest rates. For example, a rate of 2% semi-annually may be posted (the word compounded is usually omitted to reduce confusion with compound interest GICs), which means that 1% interest is paid out every six months.

- Length of Time. The terms involved with interest payout GICs are longer than one year, meeting the definition of "long-term" GICs.

The Formula

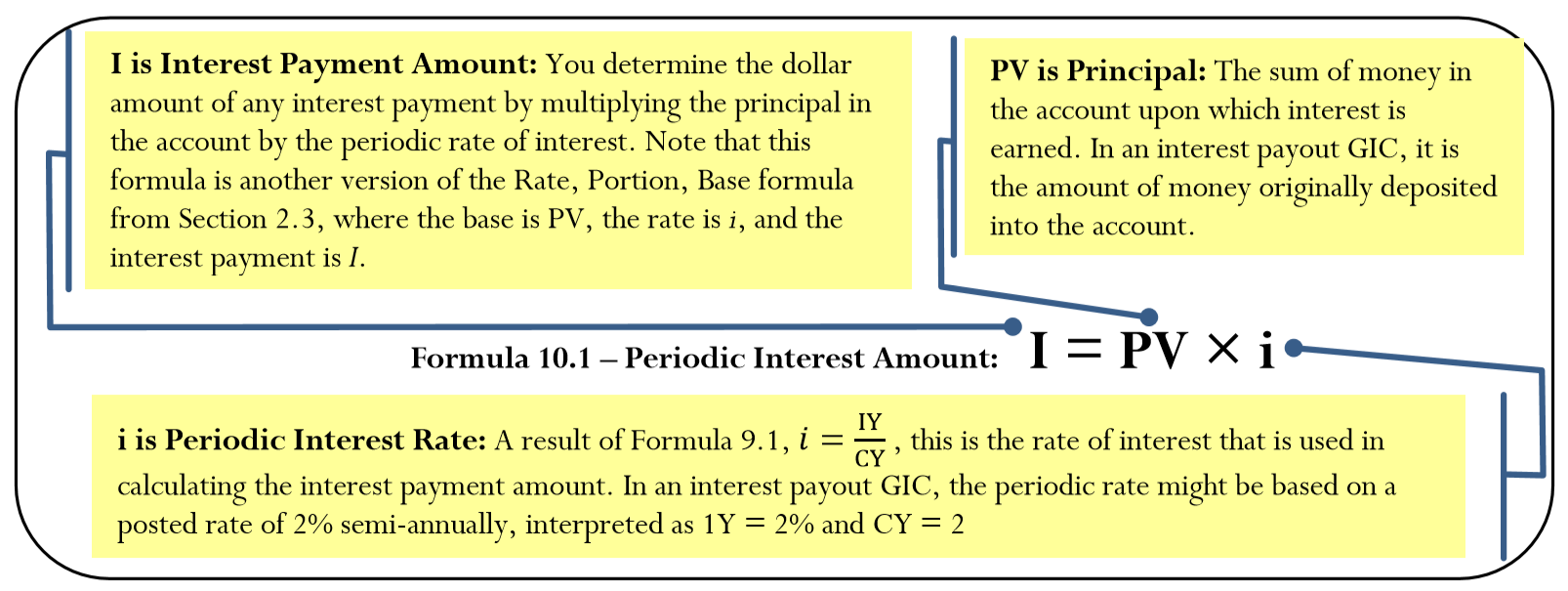

Calculating the interest payment requires a simplification of Formula 9.3 involving compound interest for single payments. As with compound interest GICs, you use the periodic interest rate calculated through Formula 9.1. However, in an interest payout GIC you never add the interest to the principal, so you do not need the 1+ term in the formula. There is also no future value to calculate, just an interest amount. This changes Formula 9.3 from \(FV = PV × (1 + i)N\) to \(I = PV × iN\). Simplifying further, you calculate the interest one compound period at a time, where \(N = 1\). This eliminates the need for the \(N\) exponent and establishes Formula 10.1.

How It Works

Follow these steps to calculate the interest payment for an interest payout GIC:

Step 1: Identify the amount of principal invested. This is the \(PV\). Also determine the nominal interest rate (\(IY\)) and interest payout frequency (\(CY\)).

Step 2: Using Formula 9.1, calculate the periodic interest rate (\(i\)).

Step 3: Apply Formula 10.1 to calculate the interest amount.

Assume $5,000 is invested for a term of three years at 5% quarterly in an interest payout GIC. Calculate the amount of the quarterly interest payment.

Step 1: The principal invested is $5,000, or \(PV\) = $5,000. The nominal interest rate is \(IY\) = 5%. The frequency is \(CY\) = 4 for quarterly.

Step 2: Applying Formula 9.1 results in \(i\) = 5%/4 = 1.25%.

Step 3: Applying Formula 10.1, I = $5,000 × 0.0125 = $62.50.

The investor receives an interest payment of $62.50 every quarter throughout the term of the investment. A term of three years then means that there are \(N = 4 × 3 = 12\) payments totaling $62.50 × 12 = $750 of interest. At the end of the three years, the GIC matures and the investor is paid out the principal of $5,000.

Important Notes

If the interest rate is variable, you must apply Formula 10.1 to each of the variable interest rates in turn to calculate the interest payment amount in the corresponding time segment. For example, if a $1,000 GIC earns 2% quarterly for the first year and 2.4% monthly for the second year, then in the first year \(I=\$ 1,000 \times \dfrac{2 \%}{4}=\$ 5\), and in the second year \(I=\$ 1,000 \times \dfrac{2.4 \%}{12}=\$ 2\).

In an interest payout GIC, is the maturity value of the investment higher than, lower than, or the same as the principal invested in the GIC?

- Answer

-

The maturity value and the principal are the same since the interest is never converted to principal

Jackson placed $10,000 into a four-year interest payout GIC earning 5.5% semi-annual interest. Calculate the amount of each interest payment and the total interest earned throughout the term.

Solution

Calculate the periodic interest payment amount (\(I\)). Then calculate the total interest paid for the term based on \(N\).

What You Already Know

Step 1:

\(PV\) = $10,000, \(IY\) = 5.5%, \(CY\) = 2

How You Will Get There

Step 2:

Apply Formula 9.2.

Step 3:

Apply Formula 10.1.

Step 4:

To calculate the total interest, determine \(N\) using Formula 9.2 and multiply the payment by \(N\).

Perform

Step 2:

\[i=\dfrac{5.5 \%}{2}=2.75 \% \nonumber \]

Step 3:

\[I = \$10,000 × 0.0275 = \$275 \nonumber \]

Step 4:

\(N\) = 2 × 4 = 8; total interest = $275 × 8 = $2,200

Every six months, Jackson receives an interest payment of $275. Over the course of four years, these interest payments total $2,200.

Compound Interest GIC

Throughout the term of a compound interest GIC, interest is periodically converted to principal. A starting amount, called the principal, remains in the account for the entire term and compounds interest. Therefore, you treat a compound interest GIC exactly like a future value compound interest calculation on a single payment amount.

How It Works

Compound interest GICs do not require any new formulas or techniques. Most commonly, the variables of concern are either the maturity value of the investment or the compound interest rate.

- Maturity Value. If the compound interest rate is fixed, then you find the maturity value by applying Formula 9.3 once, where \(FV = PV(1 + i)N\). These 4 steps were introduced in section 9.2. If the compound interest rate is variable, then to find the maturity value you must apply Formula 9.3 once for each segment of the timeline. These 7 steps were also introduced in section 9.2. Note that in step 5, no principal adjustment needs to be made since only the interest rate variable changes.

- Compound Interest Rate. In the event that the unknown variable is the interest rate, recall the 6 steps were introduced in section 9.5.

Assume an investment of $5,000 is made into a three-year compound interest GIC earning 5% compounded quarterly. Solve for the maturity value.

Step 1: The timeline below illustrates this investment. This is a fixed rate compound interest GIC with a term of three years and \(PV\) = $5,000. The nominal interest rate is \(IY\) = 5%. The compounding frequency is \(CY\) = 4.

Step 2: The periodic interest rate is \(i\) = 5%/4 = 1.25%.

Step 3: The number of compound periods is \(N\) = 4 × 3 = 12.

Step 4: Applying Formula 9.3, \(FV = \$5,000(1 + 0.0125)^{12} = \$5,803.77\). Hence, at maturity the GIC contains $5,803.77, consisting of $5,000 of principal and $803.77 of compound interest.

Supposing that each investment is held until maturity, which earns more interest, an interest payout GIC or a compound interest GIC?

- Answer

-

The compound interest GIC earns more interest since the interest is converted to principal and therefore earns even more interest. The interest payout GIC does not compound.

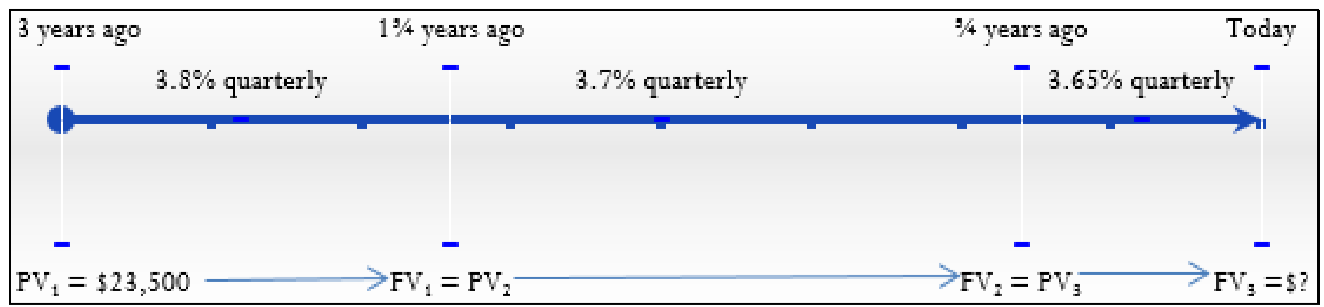

Andrej invested $23,500 into a three-year variable compound interest GIC. The quarterly compounded interest rate was 3.8% for the first 15 months, 3.7% for the next 12 months, and 3.65% after that. What is the maturity value of Andrej’s GIC?

Solution

Calculate the maturity value (\(FV\)) of Andrej’s variable rate compound interest GIC.

What You Already Know

Step 1:

The principal, terms, and interest rates are known, as shown in the timeline.

\(PV\) = $23,500

First time segment: \(IY\) = 3.8%, \(CY\) = quarterly = 4 Term = 1¼ years

Second time segment: \(IY\) = 3.7%, \(CY\) = quarterly = 4 Term = 1 year

Third time segment: \(IY\) = 3.65%, \(CY\) = quarterly = 4 Term = ¾ year

How You Will Get There

Step 2:

For each time segment, calculate the periodic interest rate by applying Formula 9.2.

Step 3:

For each time segment, calculate the number of compound periods by applying Formula 9.2.

Step 4:

Calculate the future value (\(FV_1\)) of the first time segment using Formula 9.3.

Step 5:

Let \(FV_1 = PV_2\).

Step 6:

Calculate the future value (\(FV_2\)) of the second time segment using Formula 9.3. Repeat Step 5: Let \(FV_2 = PV_3\). Repeat Step 6: Calculate the future value (\(FV_3\)) of the third time segment using Formula 9.3.

Step 7:

\(FV_3\) is the final future value amount.

Perform

Step 2:

First Time Segment:

\[i=\dfrac{3.8 \%}{4}=0.95 \% \nonumber \]

Second Time Segment:

\[i=\dfrac{3.7 \%}{4}=0.925 \% \nonumber \]

Third Time Segment:

\[i=\frac{3.65 \%}{4}=0.9125 \% \nonumber \]

Step 3:

First Time Segment:

\[N=4 \times 1\tfrac{1}{4}=5 \nonumber \]

Second Time Segment:

\[N=4 \times 1=4 \nonumber \]

Third Time Segment:

\[N=4 \times \tfrac {3}{4}=3 \nonumber \]

Step 4:

\[FV_1=\$ 23,500 \times(1+0.0095)^{5}=\$ 24,637.66119 \nonumber \]

Step 5 - Step 6:

\[FV_2=\$ 24,637.66119 \times(1+0.00925)^{4}=\$ 25,561.98119 \nonumber \]

Repeat Step 5 - Step 6:

\[FV_3=\$ 25,561.98119 \times(1+0.009125)^{3}=\$ 26,268.15 \nonumber \]

Calculator Instructions

| Segment | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 1 | 5 | 3.8 | -23500 | 0 | Answer: -24,637.66119 | 4 | 4 |

| 2 | 4 | 3.7 | 24,637.66119 | \(\surd\) | Answer: -25,561.98119 | \(\surd\) | \(\surd\) |

| 3 | 3 | 3.65 | 25,561.98119 | \(\surd\) | Answer: -26,268.14515 | \(\surd\) | \(\surd\) |

At the end of the three-year compound interest GIC, Andrej has $26,268.15, consisting of the $23,500 principal plus $2,768.15 in interest.

Using Example \(\PageIndex{2}\), what equivalent fixed quarterly compounded interest rate did Andrej earn on his GIC?

Solution

Calculate the fixed quarterly compounded interest rate (\(IY\)) that is equivalent to the three variable interest rates.

What You Already Know

Step 1:

From Example \(\PageIndex{2}\), the principal, maturity value, compounding frequency, and term are known, as illustrated in the timeline. \(CY\) = 4, Term = 3 years

How You Will Get There

Step 2:

Calculate \(N\) using Formula 9.2.

Step 3:

Substitute into Formula 9.3 and rearrange for \(i\).

Step 4:

Substitute into Formula 9.1 and rearrange for \(IY\).

Perform

Step 2:

\[N=4 \times 3=12 \nonumber \]

Step 3:

\[\begin{aligned} \$ 26,268.15 &=\$ 23,500(1+i)^{12} \\ 1.117793 &=(1+i)^{12} \\ 1.117793^{ \frac{1}{12}} &=1+i \\ 1.009322 &=1+i \\ 0.009322 &=i \end{aligned} \nonumber \]

Step 4:

\[0.009322=\dfrac{I Y}{4} \nonumber \]

\[IY=0.037292=3.7292 \% \text { compounded quarterly } \nonumber \]

Calculator Instructions

| N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|

| 12 | Answer: 3.729168 | -23500 | 0 | 26268.15 | 4 | 4 |

A fixed rate of 3.7292% compounded quarterly is equivalent to the three variable interest rates that Andrej realized.

Escalator Interest GIC

An escalator interest GIC is a compound interest rate GIC with four distinguishing characteristics:

- The interest rate is variable throughout the term.

- The nominal interest rate always increases with each change so that higher returns on longer terms will encourage the investor to keep the sum of money invested in this GIC.

- The interest rates are known in advance and fixed for the duration of each time segment of the investment.

- Each time segment is most commonly one year in length.

Various financial institutions call escalator interest GICs by many names to differentiate their products from others on the market. Some of the names include Rate Riser, Stepper, Multi-Rater, Stepmaker, and RateAdvantage. Regardless of the actual name used, if the GIC fits the above characteristics it is an escalator interest GIC.

How It Works

The escalator interest GIC is a special form of the compound interest GIC, so the exact same formulas and procedures used for compound interest GICs remain applicable. The most common applications with escalator GICs involve finding one of the following:

- The maturity value of the GIC.

- The equivalent fixed rate of interest on the GIC so that the investor can either compare it to that of other options or just better understand the interest being earned. Recall from Chapter 9 the 6 steps you need to calculate equivalent fixed rates.

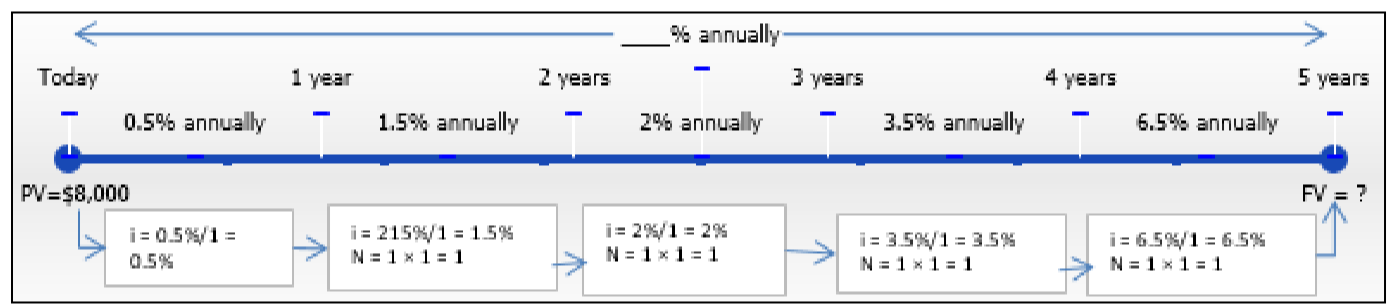

Antoine is thinking of investing $8,000 into a five-year CIBC Escalating Rate GIC with annually compounded rates of 0.5%, 1.5%, 2%, 3.5%, and 6.5% in each subsequent year. Determine the maturity value of Antoine's investment along with the equivalent fixed annually compounded rate.

Solution

First, calculate the maturity value of Antoine's investment (\(FV\)) at the end of the five-year term. Then calculate the equivalent fixed nominal interest rate (\(IY\)).

What You Already Know

Step 1:

The present value, term, and escalating nominal interest rates are known, as shown in the timeline.

How You Will Get There

Step 2:

For each time segment, calculate the \(i\) and \(N\) in the timeline using Formula 9.1 and Formula 9.2. Note that since all rates are compounded annually (\(CY\) = 1), Formula 9.1 results in \(i = IY\) for all time segments. As well, in Formula 9.2 the \(N\) always equals 1 since both \(CY\) = 1 and Years = 1 for every time segment.

Step 3: Solve for \(FV\) using Formula 9.3. Since only the interest rate changes, expand the formula:

\[FV=PV \times\left(1+i_{1}\right)^{N_{1}} \times\left(1+i_{2}\right)^{N_{2}} \times \ldots \times\left(1+i_{5}\right)^{N_{5}} \nonumber \]

Step 4: To reflect the entire five-year term compounded annually, calculate a new value of \(N\) using Formula 9.2.

Step 5: Substitute into Formula 9.3 and rearrange for \(i\).

Step 6: With \(CY\) = 1, then \(IY = i\).

Perform

Step 2:

The above figure shows the successive calculated values of \(i\) and \(N\).

Step 3:

\[FV_{1}=\$ 8,000(1+0.005)^{1}(1+0.015)^{1}(1+0.02)^{1}(1+0.035)^{1}(1+0.065)^{1}=\$ 9,175.13 \nonumber \]

Step 4:

\[N = 1 × 5 = 5 \nonumber \]

Step 5:

\[\begin{aligned} \$ 9,175.13&=\$ 8,000(1+i)^{5} \\ 1.146891&=(1+i)^{5} \\ 1.146891^{\frac{1}{5}}&=1+i \\ 1.027790&=1+i \\ 0.027790&=i \end{aligned} \nonumber \]

Step 6:

\[IY=i=0.027790 \text { or } 2.779 \% \text { compounded annually} \nonumber \]

Calculator Instructions

| Segment | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 1 | 1 | 0.5 | -8000 | 0 | Answer: 8,040 | 2 | 2 |

| 2 | \(\surd\) | 1.5 | -8040 | \(\surd\) | Answer: 8,160.60 | \(\surd\) | \(\surd\) |

| 3 | \(\surd\) | 2 | -8,160.60 | \(\surd\) | Answer:8,323.812 | \(\surd\) | \(\surd\) |

| 4 | \(\surd\) | 3.5 | -8,323.812 | \(\surd\) | Answer: 8,615.14542 | \(\surd\) | \(\surd\) |

| 5 | \(\surd\) | 6.5 | -8,615.14542 | \(\surd\) | Answer: 9,175.129872 | \(\surd\) | \(\surd\) |

| All | 5 | Answer: 2.779014 | -8000 | \(\surd\) | 9175.13 | \(\surd\) | \(\surd\) |

If Antoine invests in the CIBC Escalating Rate GIC, the maturity value after five years is $9,175.13. He realizes 2.779% compounded annually on his investment.