12.5: Application - How To Purchase A Vehicle

- Page ID

- 22142

What is the cheapest way to acquire a vehicle? With 20 million cars on the road for 12 million Canadian households, that is an average of 1.7 cars per household in Canada. In fact, on average Canadians purchase about 10 to 12 cars in their lifetime. With average prices in the $25,000 to $30,000 range per vehicle, and factoring in rising inflation over your lifetime, you will spend approximately $550,000 on acquiring vehicles! Yet despite this huge amount of money being spent, shockingly few consumers take the time to analyze their financing options critically. Would you spend $550,000 without doing some research? I thought not.

This section guides you through the practical task of finding the cheapest of the alternatives for obtaining a vehicle. It lays out the four primary means of vehicle ownership and develops a procedure through which you can make a smart purchase decision.

What Are the Choices?

A few matters need to be cleared up from the outset. This section sticks to examining vehicle leases aimed at eventual ownership. Studies of vehicle leases have revealed that leasing a vehicle without intent to own is much more costly than ownership, even after factoring in maintenance and repairs. Give it some thought: Leasing a vehicle with no intent ever to own it means that you will be making monthly car payments for the rest of your driving life. That is called the "forever-in-debt” club. That does not sound like much fun, does it?

Smart vehicle ownership means exploring the various financial paths to vehicle ownership and ultimately choosing the lowest cost option that results both in 100% ownership of the vehicle for as long as you decide to retain the vehicle and in eventual termination of your car payments. That definitely sounds much more financially appealing.

One of the ways to purchase the vehicle is to pay cash for it. While this is technically possible, very few Canadians have $30,000 lying around that they can just write a cheque against. Therefore, this option is not pursued as a normal alternative. If you cannot pay cash, then you must finance the purchase by borrowing the money from an organization.

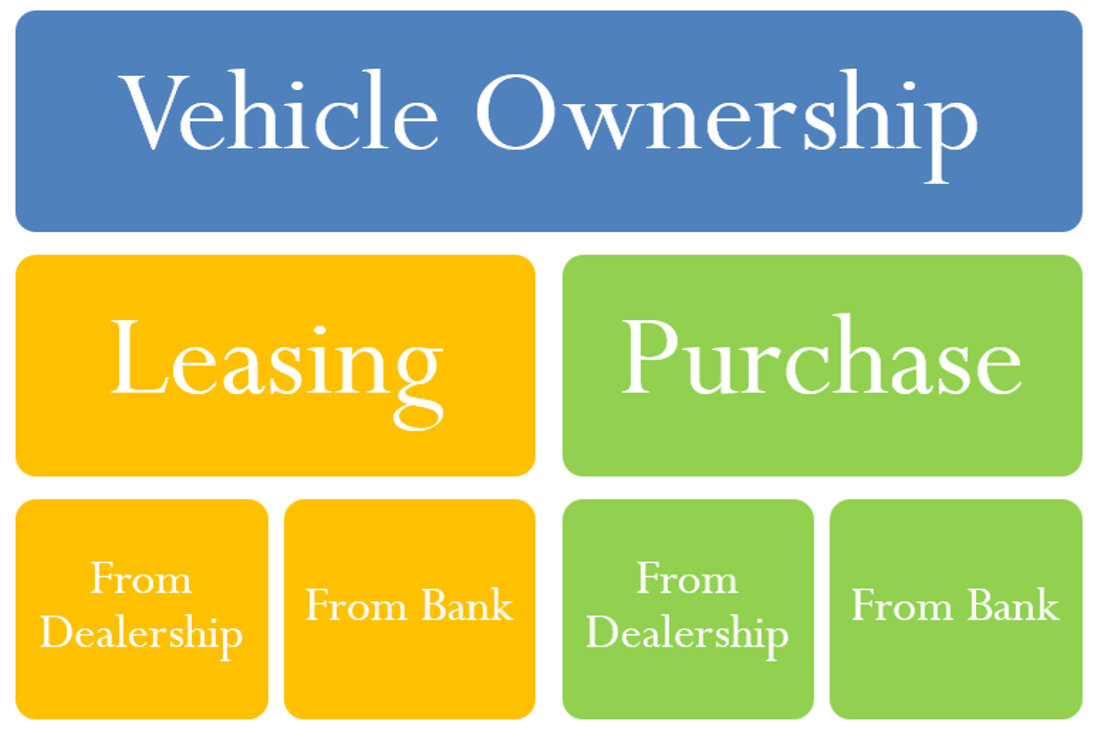

The figure below illustrates the four paths available for a typical vehicle acquisition.

The two basic options are to lease the vehicle or purchase it. You can borrow the money from either the dealership or a financial institution of your choice (from here on just called a bank for simplicity), such as RBC or a credit union. Note that if you lease the vehicle, you intend to pay the residual value upon the termination of the lease term.

Through the Internet and publications such as newspapers and flyers, you can usually obtain a lot of information about each of these four options without having to visit the dealership or a financial institution. Sometimes you may have to look in the fine print. The goal is to explore your monthly payment under equal conditions for each of the four options and then select the lowest payment.

The Formula

Borrowing funds for a car requires either a loan or a lease. Both options represent annuities and have previously been discussed in this textbook. Therefore, to figure out your lowest cost alternative to vehicle ownership you do not need any new formulas, just a new process.

How It Works

The secret to choosing well is that most vehicles actually have two prices at the dealership. One is the financing price and the other is a cash price, which results from a cash rebate that lowers the price. To be eligible to receive this cash rebate, the dealership must receive payment in full for the vehicle on the date of purchase. If you elect to have a bank be your source of funds, then the bank will provide a cheque to the dealership for the vehicle on your behalf, and therefore you will have paid cash! Thus, you need to borrow less money from the bank to acquire the vehicle since the cash price is lower. If you elect for the dealership to be your source of funds, then the dealership is not paid in full right away, and you are not eligible for the cash rebate. Thus, you pay the financing price, which is higher.

Of course, the dealerships want you to borrow from them since you pay the higher price and they receive an additional revenue stream from the interest they charge you. Dealerships put very tempting offers in front of consumers. Because most consumers do not understand the time value of money, they fail to compare these offers with other alternatives. Do you pay more for the car but at a lower interest rate from the dealership, or do you pay less for the car but at a higher interest rate from the bank? Only a time value of money calculation can determine that. The consumer’s best decision is based on which alternative has the lowest payment under equal conditions.

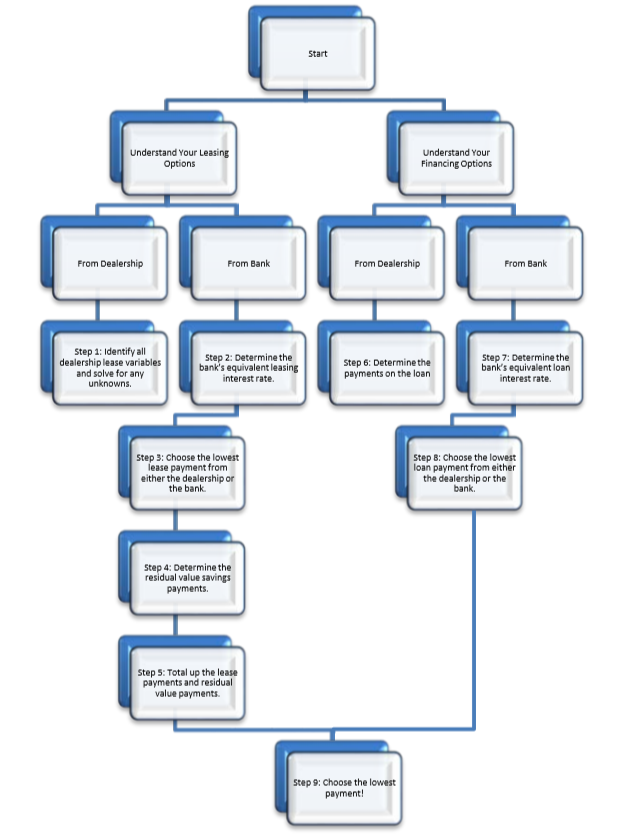

The steps for figuring out the lowest cost automotive option are illustrated in the figure below.

To understand the process illustrated, it is much easier to obtain information on vehicles from dealership advertisements or websites. Most commonly, the price of the vehicle is the same regardless of which dealership you might visit. Therefore, acquiring the vehicle from a dealership commonly represents a singular path with known information. On the other hand, approximately 75 banks and 485 credit unions are available to consumers in Canada. This represents up to 560 different choices, from which it would be extremely time consuming to gather all required information. The process establishes a threshold against which the banks are compared. You need contact only those financial institutions that pass the initial screening.

Step 1: Understand your leasing terms from the dealership. You must identify your leasing variables, including the lease interest rate, lease term, leasing payment structure, any down payment required, the purchase price, and the residual value. If any of these variables is unknown, identify its value by applying the appropriate annuity due formula.

Step 2: Determine the equivalent leasing interest rate from your bank. Banks advertise interest rates, not payments. Thus, you calculate the interest rate a bank must charge to be equivalent to the dealership using the identical leasing structure using the same lease term, lease payments, compounding, and residual value. The present value used in this calculation is the dealer's purchase price from step 1 less the cash rebate. Solve for the bank's equivalent nominal interest rate (\(IY\)).

Step 3: Make your leasing decision. After conducting some research, if you find a bank with a lower interest rate than the calculated \(IY\) from step 2, then choose the bank lease (you should contact the bank to confirm the rate). Recalculate the leasing payments at the bank's interest rate. If you cannot find a lower interest rate from a bank, then select the dealership lease payments from step 1.

Step 4: A lease requires you to save up for the residual value. In choosing a leasing option, you also must save enough funds to pay off the residual value at the lease end. Set up an annuity due savings account using the same term and payment frequency. Use an appropriate interest rate from your savings institution. Calculate the annuity payment required to meet your residual value savings goal.

Step 5: Total the lease payment. Your lease payment from step 3 plus the residual value annuity payment from step 4 is the total out-of-pocket commitment required per payment interval to own the vehicle through leasing.

That completes the analysis of the leasing alternative. The remainder of the steps now involve examining your financing options.

Step 6: Figure out the loan payment from the dealership. Using the same term and payment frequency as the lease, calculate the payments to purchase the vehicle. Remember that a vehicle loan is an ordinary annuity. Use the financing price of the vehicle and the financing interest rate (not the lease rate) offered by the dealership.

Step 7: Figure out the equivalent loan interest rate from your bank. Using the same process as in step 2, aim to determine the equivalent interest rate from a bank loan that matches the payments with the dealership. With an identical structure and using the cash price, calculate the bank's equivalent nominal interest rate (\(IY\)).

Step 8: Make the loan decision. If a bank offers an interest rate lower than the calculated \(IY\) from step 7, then select the bank loan (and you should probably contact the bank to confirm the rate). Recalculate the loan payments at the bank's interest rate. If you are unable to find a bank with a lower interest rate, then select the dealership loan payments from step 6.

Step 9: The final decision. In step 5, you calculated the total lease payment. From step 8, you have the lowest loan payment. The obvious choice is the lowest payment.

Important Notes

- At any given point in time, numerous vehicle rebates that adjust the purchase price of the vehicle are available (subject to various conditions). If such rebates apply to your purchase situation, modify the vehicle's purchase price accordingly in your calculations.

- While leases are generally non-negotiable, the purchase price of a vehicle may be negotiable depending on the dealership and automotive manufacturer's policies. If haggling is allowed, estimate the amount by which you could reduce the purchase price and use the reduced amount for the calculations in steps 6 and 7.

- If you have a trade-in for your vehicle acquisition, the value of the trade-in is treated in the same manner as a down payment toward the vehicle. It reduces the purchase price, so you modify your calculations accordingly.

- The fundamental concept of time value of money says that to decide between the different leasing and financing timelines, all money must be moved to the same focal date. Note that in the process explained above you are making the final decision by comparing the payment amounts on the annuity due against the payment amounts on the ordinary annuity. A clear discrepancy in the timing of the payments is evident. In technically correct financial theory, to obey the fundamental concept of time value of money these payment amounts should then be present valued to the start of the transaction (the focal date) and the lower present value should be chosen. However, the reality is that most consumers base their purchase decision on the payment amount and what they can afford rather than on the total amount. Therefore, it is more logical to base the car acquisition decision strictly on the physical out-of-pocket annuity payment amounts.

Haber Suzuki advertises a Suzuki SX4 Hatchback for sale. The following information is known:

- Leasing information: Seven-year term, 0.9% compounded annually lease rate, $90.75 biweekly payments, $8,250 residual value, no down payment required.

- Purchase information: Cash rebate of $3,500 available, purchase financing at 2.99% compounded annually.

- Bank options: The lowest vehicle lease rate from a bank is 4.4% compounded annually, while the lowest loan rate is 8.25% compounded annually.

- Savings accounts: The best rate available is 2% compounded annually. What is the lowest cost method to purchase this vehicle?

Solution

Examine the four paths to vehicle ownership and choose the path with the lowest biweekly payment.

What You Already Know

There are five timelines, one for each of the options (two leases, one savings account, two purchases):

Dealership Lease: \(IY\) = 0.9%, \(CY\) = 1, \(PMT\) = $90.75, \(PY\) = 26, \(FV\) = $8,250, Years = 7

Bank Lease: \(PV_{DUE}\) = Purchase Price − $3,500, \(CY\) = 1, \(PMT\) = $90.75, \(PY\) = 26, \(FV\) = $8,250, Years = 7

Residual Savings Plan: \(PV\) = $0, \(IY\) = 2%, \(CY\) = 1, \(PY\) = 26, \(FV\) = $8,250, Years = 7

Dealership Loan: \(PV_{ORD}\) = Purchase Price, \(IY\) = 2.99%, \(CY\) = 1, \(PY\) = 26, \(FV\) = $0, Years = 7

Bank Loan: \(PV_{ORD}\) = Purchase Price − $3,500, \(CY\) = 1, \(PMT\) = Dealer loan payment, \(PY\) = 26, \(FV\) = $0, Years =

How You Will Get There

Step 1:

In the dealership lease, the purchase price of the vehicle for the lease is missing. Find the present value of the residual value by applying Formulas 9.1, 9.2, and 9.3 (rearranged for \(PV\)). Then apply Formulas 11.1 and 11.5 to find the present value of the lease payments. Add the \(PV\) and \(PV_{DUE}\) to arrive at the purchase price.

Step 2:

In the bank lease, calculate the equivalent bank leasing interest rate. Adjust the purchase price to reflect the cash price and use your calculator to solve Formula 11.5 for \(IY\).

Step 3:

If the bank rate is higher, choose the payment from step 1. If the bank rate is lower, then recalculate the lease payment using Formulas 9.1, 9.2, and 9.3 (rearranged for PV) to adjust the \(PV_{DUE}\) and apply Formula 11.5 (rearranged for \(PMT\)).

Step 4:

In the residual savings plan, save to pay off the residual value using the savings account interest rate. Apply Formulas 9.1 and 11.3 (rearranged for \(PMT\)).

Step 5:

Add the payments from steps 3 and 4. This is the total lease payment.

Step 6:

In the dealership loan, calculate the loan payments from the dealership by applying Formulas 9.1 and 11.4 (rearranged for \(PMT\)).

Step 7:

In the bank loan, calculate the equivalent bank loan interest rate. Adjust the purchase price and use your calculator to solve Formula 11.4 for \(IY\).

Step 8:

If the bank rate is higher, choose the payment from step 6. If the bank rate is lower, recalculate the loan payment, first using Formulas 9.1 and 9.3 (rearranged for \(PV\)) to adjust the \(PV_{ORD}\) and then using Formula 11.4 (rearranged for \(PMT\)).

Step 9:

Choose the lowest payment from step 5 or step 8.

Perform

Step 1:

Residual Value:

\(i=0.9 \% / 1=0.9 \% ; N=1 \times 7=7 \text { compounds }\);

\(\$ 8,250=PV(1+0.009)^{7}\);

\[PV=\$8,250 \div(1+0.009)^{7}=\$7,748.466949 \nonumber \]

Lease Payments:

\(N=26 \times 7=182 \text { payments } \)

\[PV_{DUE}=\$ 90.75\left[\dfrac{1-\left[\dfrac{1}{(1+0.009)^{\frac{1}{26}}}\right]^{182}}{(1+0.009)^{\frac{1}{26}}-1}\right] \times(1+0.009)^{\frac{1}{26}}=\$ 16,011.97657 \nonumber \]

\[\text { Total } PV=\$ 7,748.466949+\$ 16,011.97657=\$ 23,760.44=\text { purchase price of the vehicle } \nonumber \]

Step 2:

\(\text { Cash price of vehicle }=\$ 23,760.44-\$ 3,500.00=\$ 20,260.44\)

Solve Formula 11.5 (adjusting for residual value):

\[\$ 20,260.44-\dfrac{\$ 8,250}{\left((1+i)^{\frac{1}{26}}\right)^{182}}=\$ 90.75\left[\dfrac{1-\left[\dfrac{1}{(1+i)^{\frac{1}{26}}}\right]^{182}}{(1+i)^{\frac{1}{26}}-1}\right] \times(1+i)^{\frac{1}{26}} \nonumber \]

From calculator, \(IY\) = 4.5331% compounded annually.

Step 3:

The bank lease rate of 4.4% is lower than the equivalent lease rate of 4.5331%. Choose the lease from the bank and recalculate the payment.

\(i=4.4 \% / 1=4.4 \% ; N=1 \times 7=7 \text { compounds }\)

\[\begin{aligned}\$ 8,250&=PV(1+0.044)^{7} \\ PV&=\$ 8,250 \div(1+0.044)^{7}\\ &=\$ 6,103.099605\end{aligned} \nonumber \]

\[\text { new } PV_{DUE}=\$ 20,260.44-\$ 6,103.099605=\$ 14,157.34039 \nonumber \]

\(N = 182\) payments (same as step 1)

\[\$ 14,157.34039=PMT\left[\dfrac{1-\left[\dfrac{1}{(1+0.044)^{\frac{1}{26}}}\right]^{182}}{(1+0.044)^{\frac{1}{26}}-1}\right] \times(1+0.044)^{\frac{1}{26}} \nonumber \]

\[\$ 14,157.34039=PMT\left[\dfrac{0.260230}{0.001657}\right] \times 1.001657 \nonumber \]

\[PMT=\dfrac{\$ 14,157.34039}{157.261348}=\$ 90.02 \nonumber \]

Step 4:

\(i=2 \% / 1=2 \% ; N=182 \text { payments }\) (same as step 1)

\[\$ 8,250=PMT\left[\dfrac{\left[(1+0.02)^{\frac{1}{26}}\right]^{182}-1}{(1+0.02)^{\frac{1}{26}}-1}\right] \times(1+0.02)^{\frac{1}{26}} \nonumber \]

\[\$ 8,250=PMT\left[\dfrac{0.148685}{0.000761}\right] \times 1.000761 \nonumber \]

\[PMT=\dfrac{\$ 8,250}{195.292254}=\$ 42.24 \nonumber \]

Step 5:

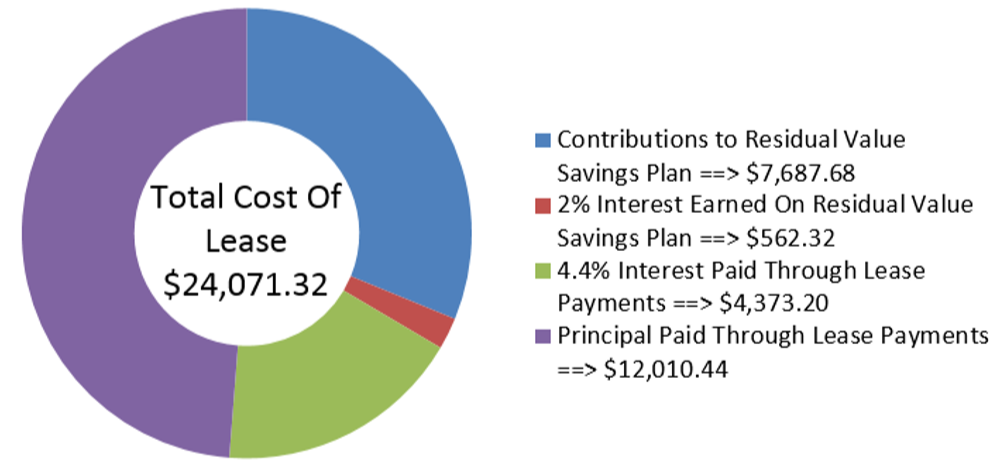

The total lease payment is $90.02 + $42.24 = $132.26 biweekly.

Step 6:

\(\text { Purchase price }=\$ 23,760.44 \) (from step 1) ; \(i=2.99 \% / 1=2.99 \% ; N=182 \text { payments } \) (same as in step 1)

\[\$ 23,760.44=PMT\left[\dfrac{1-\left[\dfrac{1}{(1+0.0299)^{\frac{1}{26}}}\right]^{182}}{(1+0.0299)^{\frac{1}{26}}-1}\right] \nonumber \]

\[\$ 23,760.44=PMT\left[\dfrac{0.186355}{0.001133}\right] \nonumber \]

Step 7:

Cash price of vehicle =$20,260.44 (from step 2).

\[\$ 20,260.44=\$ 144.56\left[\dfrac{1-\left[\dfrac{1}{(1+i)^{\frac{1}{26}}}\right]^{182}}{(1+i)^{\frac{1}{26}}-1}\right] \nonumber \]

From calculator, \(IY\) = 8.0841% compounded annually.

Step 8:

Since the bank loan rate of 8.25% is higher than the equivalent loan rate of 8.0841%, remain with the dealership loan and make payments of $144.56.

Step 9:

The lowest payment is from step 5, which is $132.26.

Calculator Instructions

| Step | Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|---|

| 1 | BGN | 182 | 0.9 | Answer: 23,760.44352 | -90.75 | -8250 | 26 | 1 |

| 2 | \(\surd\) | \(\surd\) | Answer: 4.533113 | 20260.44 | \(\surd\) | \(\surd\) | \(\surd\) | \(\surd\) |

| 3 | \(\surd\) | \(\surd\) | 4.4 | \(\surd\) | Answer: -90.024284 | \(\surd\) | \(\surd\) | \(\surd\) |

| 4 | \(\surd\) | \(\surd\) | 2 | 0 | Answer: -42.244378 | 8250 | \(\surd\) | \(\surd\) |

| 6 | END | \(\surd\) | 2.99 | 23760.44 | Answer: -144.558127 | 0 | \(\surd\) | \(\surd\) |

| 7 | \(\surd\) | \(\surd\) | Answer: 8.084126 | 20260.44 | -144.56 | \(\surd\) | \(\surd\) | \(\surd\) |

The best option to acquire this vehicle is to lease it from the bank. This requires biweekly lease payments of $90.02 and residual savings payments of $42.24 for a total of $132.26 per period for seven years. At the end of the lease, the accumulated savings is used to pay the $8,250 residual value.