12.6: Application - Planning Your RRSP

- Page ID

- 22143

How and when should you start planning your RRSP? When you are in your late teens or early twenties, you are probably not thinking much about your retirement income. You are at a stage in life when, besides paying for education or paying off student loans, you move out on your own and need to acquire many possessions ranging from appliances to furniture to transportation. Your income is probably at its lowest point in your career. You find yourself on a limited budget with high demands.

Ironically, though, this is the best time to start your RRSP. Throughout the last few chapters you have already witnessed the incredible power of compound interest. Through discussion, examples, and even some of the exercises, it should be clear that the earlier you invest your money, the less you have to pay out of your pocket to reach your retirement income goals.

But why should you go to the trouble and expense of contributing to an RRSP? For those counting on the government to provide retirement income, it was pointed out that the typical Canadian in retirement earns $529.09 per month from the Canada Pension Plan (CPP) and $514.74 from Old Age Security (OAS). Both of these amounts are pre-tax, which means your net income from these sources will be even less. This is not much to live off of.

Are companies not supposed to provide pension plans for their employees? While some companies do offer pension plans, these public and private-sector companies are few and far between. The Pension Investment Association of Canada (PIAC) manages approximately 130 pension funds representing approximately 80% of Canada's pension industry by asset size. In a 2007 study conducted by the PIAC, it found that approximately 20.5% of Canadian membership companies are either closing or considering closing their defined benefit pension funds. In Ontario, the percentage is much higher at 36.2%. These closures are in the private sector. Additionally approximately 20% of Canadian organizations are reducing future benefits.1

The bottom line is that you should not count on somebody else to create your retirement income for you. Also, do not bank on being lucky enough to work for a company that has a good pension plan. You need to take care of yourself.

This section introduces a simplified model of RRSP planning that reasonably approximates the financial commitment that will provide a satisfactory retirement income. Ultimately, you should always consult a financial adviser as you plan your RRSP.

Income Planning

Income planning requires you to project future earnings, determine income needs in retirement, and then develop a savings plan toward that goal. Look at these details:

- Projected Retirement Income. The first step is to determine your annual retirement income at the age of retirement. The general consensus is that a retiree needs approximately 70% of pre-retirement gross income to live comfortably and maintain the same lifestyle. It is difficult to know what that amount will be 30 or 40 years from now. However, today's typical retirement income is known. The average Canadian needs about $40,000 of gross income. You can adjust this number higher if necessary. You can then project today's amount forward to the age of retirement using an estimated rate of inflation based on historical data.

- Principal Required at Age of Retirement. The second step requires you to determine the principal needed to fund the annual income requirement at the age of retirement. You must estimate the number of years for which withdrawals are to be made from the RRSP balance. In essence, how long are you going to live? While no one knows the answer, the average Canadian male lives to age 78 while the average Canadian female lives to age 82. These are good starting points. It would not make sense to lower these numbers since you do not want to be caught short, but you could raise these numbers if necessary. A look at your parents, grandparents, and other ancestors combined with your own lifestyle choices might indicate the typical life span you may expect. While you are not guaranteed to live that long, at least you can base a reasonable financial decision upon it. You must also factor in inflation during the retirement years. Each year, your income must rise to keep up with the cost of living. Finally, you should use a conservative, low-risk interest rate in these calculations because you certainly cannot afford to lose your savings to another "Black Monday" (which refers to October 19, 1987, when stock markets around the world crashed).

- Annuity Savings Payments. The final step is to determine the payments necessary to reach the principal required for retirement. You should consider that your income generally rises over your lifetime, which means as you get older you could afford to contribute a larger amount to your RRSP. Thus, contributions start small when you are young and increase as you grow older. The interest rate you use must reflect the market and your risk tolerance. Since 1980, the Toronto Stock Exchange (TSX) has averaged approximately 6% annual growth, which is a good starting point for determining what interest rate to use in your calculations.

The Formula

RRSP planning does not involve any new formulas. Instead, you must combine previously studied single payment concepts from Chapter 9 and annuity concepts from both Chapter 11 and Chapter 12.

How It Works

Your end goal is to calculate the regular contributions to your RRSP necessary to achieve a balance in your RRSP from which you can regularly withdraw in retirement to form your income. The calculations presented ignore other sources of retirement income such as the CPP or OAS, as if you were solely responsible for your own financial well-being. You can then treat any other income as bonus income.

Follow the steps:

Step 1: Calculate the annual retirement income you will need. Choose a value of annual income in today's dollars along with an annual rate of inflation to use. Then, by applying Formula 9.1 (Periodic Interest Rate), Formula 9.2 (Number of Compound Periods for Single Payments), and Formula 9.3 (Compound Interest for Single Payments) you can move that income to your required age of retirement.

Step 2: Calculate the present value of the retirement income. Most people receive their retirement income monthly, so you divide the result from step 1 by 12. Retirement income usually starts one month after retirement, thus forming an ordinary annuity. Using a reasonable annual rate of inflation, you also divide the inflation rate by 12 to approximate the growth rate to be used in calculating a constant growth annuity required during retirement. Estimate the number of years the retirement fund must sustain and select a low-risk conservative interest rate. Then apply Formula 9.1 (Periodic Interest Rate), Formula 11.1 (Number of Annuity Payments), and Formula 12.3 (Present Value of a Constant Growth Ordinary Annuity) to arrive at the principal required at the age of retirement.

Step 3: Calculate the annuity payment required to achieve your goal. If a single payment is already invested today, deduct its future value at the age of retirement (using Formula 9.1, Formula 9.2, and Formula 9.3) from the amount of money determined in step two. The principal at the age of retirement (from step 2) now becomes the future value for the ordinary constant growth annuity. Use an interest rate that reflects market rates and your risk level, along with an appropriate growth rate you select for the annuity payments you will make. This growth rate may or may not match the growth rate determined in step 2. Thus, arriving at the annuity payment amount requires Formula 9.1 (Periodic Interest Rate), Formula 11.1 (Number of Annuity Payments), and Formula 12.1 (Future Value of a Constant Growth Ordinary Annuity) rearranged for PMT.

Important Notes

This procedure approximates the required regular RRSP contribution. However, recognize that the procedure is somewhat simplified and certainly does not factor in all variables that may apply in an individual situation. It is always best to consult a certified financial planner to ensure that your RRSP plan works under current market conditions and under any applicable restrictions.

Also, the steps listed above also assume an ordinary annuity structure. In the event of an annuity due, substitute the appropriate annuity due formula as required.

Paths To Success

One of the hardest tasks in planning an RRSP is to guess interest rates and rates of inflation. If you are unsure of what numbers to use, some safe values are as follows:

- A rate of inflation or growth rate of 3% compounded annually, equaling 0.25% per month

- During retirement, an interest rate of 4% compounded annually

- While you contribute toward your RRSP, an interest rate of 6% compounded annually, based on the approximate historical average over the past 31 years (1980–2011) for the TSX.

Assume that two people—Person A and Person B—are saving for the same retirement amount under equal conditions except as noted. In each of the following cases, determine whose RRSP contributions are higher:

- Person A starts contributing at age 18 while Person B starts contributing at age 25.

- Person A earns 7% compounded annually while Person B earns 6% compounded annually.

- Person A contributes monthly while Person B contributes semi-monthly.

- Person A contributes through an ordinary annuity while Person B uses an annuity due.

- Person A earns 4.5% interest during retirement while Person B earns 4% interest during retirement.

- Person A has quarterly compounded earnings while Person B has monthly compounded earnings.

- Answer

-

- Person B, because he has a shorter period to accumulate the same amount as Person A.

- Person B, because a lower interest rate requires more principal, hence larger contributions.

- Person A, because the principal does not increase as often as Person B’s does.

- Person A, because there is one fewer compounds than for Person B.

- Person B earns less interest, so a larger principal is required at retirement than Person A requires.

- Person A, because the interest is not converted to principal as often as it is for Person B.

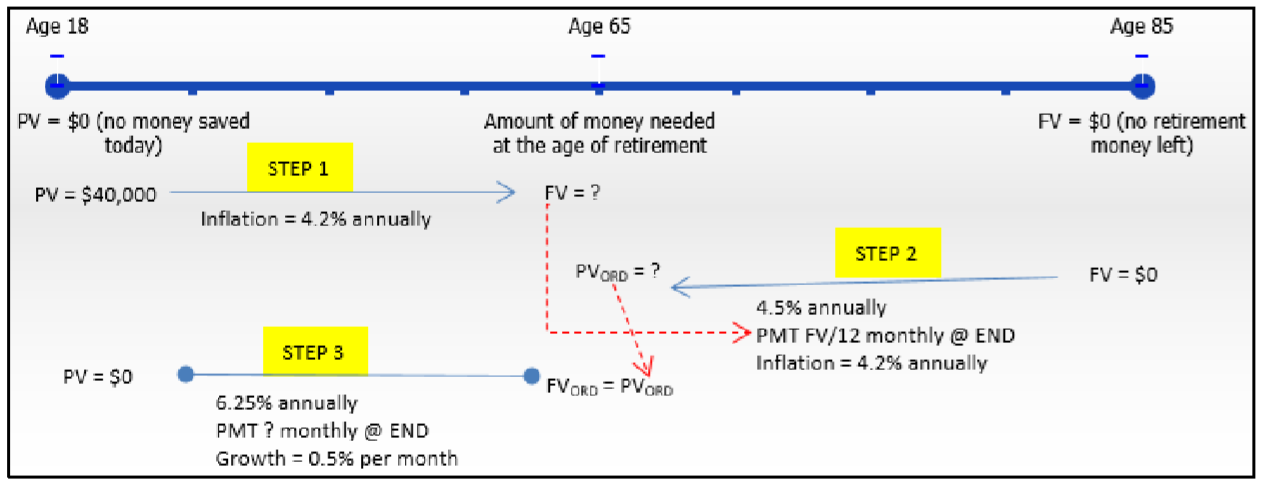

Jesse just turned 18 and plans on retiring when he turns 65. In today's funds, he wants to earn $40,000 annually in retirement. Based on the past 50 years, he estimates inflation at 4.2% compounded annually. He would like to receive 20 years of monthly payments from his retirement money, which is forecasted to earn 4.5% compounded annually. He believes his RRSP can earn 6.25% compounded annually during his contributions, he has no money saved to date, and he would like to increase each payment by 0.5%. One month from now, what is the amount of his first monthly RRSP contribution?

Solution

Jesse wants to make regularly increasing contributions to his RRSP at the end of the monthly payment interval with annual compounding. Therefore, this is a constant growth general ordinary annuity. Calculate his first payment (\(PMT\)).

What You Already Know

Jesse's RRSP plan appears in the timeline.

Step 1:

\(PV\) = $40,000, \(IY\) = 4.2%, \(CY\) = 1, Years = 47

Step 2:

\(FV\) = $0, \(IY\) = 4.5%, \(CY\) = 1, \(PY\) = 12, Years = 20, \(Δ\%\) = 4.2%/12 = 0.35% per payment

Step 3:

\(PV\) = $0, \(FV_{ORD}\) = Step 2 answer, \(IY\) = 6.25%, \(CY\) = 1, \(PY\) = 12, Years = 47, \(Δ\%\) = 0.5%

How You Will Get There

Step 1:

Move Jesse’s desired annual income from today to the age of retirement by applying Formula 9.1, Formula 9.2, and Formula 9.3.

Step 2:

Calculate the amount of money needed at the age of retirement by applying Formula 9.1, Formula 11.1, and Formula 12.3.

Step 3:

Calculate Jesse’s regular monthly payment by applying Formula 9.1, Formula 11.1, and Formula 12.1.

Perform

Step 1:

\(i=4.2 \% / 1=4.2 \% ; N=1 \times 47=47 \text { compounds; } FV=\$ 40,000(1+0.042)^{47}=\$ 276,594.02\)

Step 2:

\(i=4.5 \% / 1=4.5 \% ; N=12 \times 20=240 \text { payments }\)

Note that the monthly payment is $276,594.02 ÷ 12 = $23,049.50

\[PV_{ORD}=\dfrac{\$ 23,049.50}{1+0.0035}\left[\dfrac{1-\left[\dfrac{1+0.0035}{(1+0.045)^{\frac{1}{12}}}\right]^{240}}{\dfrac{(1+0.045)^{\frac{1}{12}}}{1+0.0035}-1}\right]=\$ 5,398,479.88 \nonumber \]

Step 3:

\(i=6.25 \% / 1=6.25 \% ; N=12 \times 47=564 \text { payments } \)

\[\$ 5,398,479.88=PMT(1+0.005)^{564-1}\left[\dfrac{\left[\dfrac{(1+0.0625)^{\frac{1}{12}}}{1+0.005}\right]^{564}-1}{\dfrac{(1+0.0625)^{\frac{1}{12}}}{1+0.005}-1}\right] \nonumber \]

\[\begin{aligned}\$ 5,398,479.88&=PMT(16.576497)[574.367284]\\ \$ 5,398,479.88&=PMT(9,520.997774)\\ \$ 567.01&=PMT\end{aligned} \nonumber \]

Calculator Instructions

| Step | Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|---|

| 1 | END | 47 | 4.2 | -40000 | 0 | Answer: 276,594.0176 | 1 | 1 |

On the basis that the rate of inflation is relatively accurate, Jesse’s first RRSP contribution one month from now is $567.01. Each subsequent payment increases by 0.5% resulting in a balance of $5,398,479.88 at retirement, from which he can make his first withdrawal of $23,049.50 increasing at 0.35% per month for 20 years.

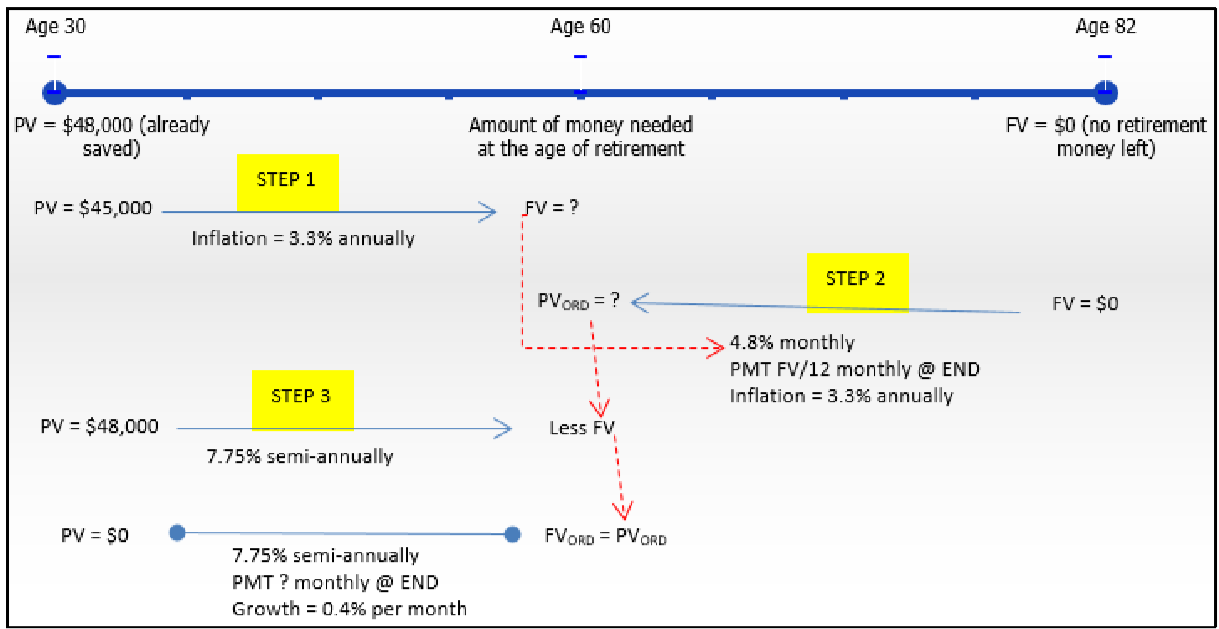

Marilyn just turned 30 and plans on retiring when she turns 60. In today's funds, she wants to earn $45,000 in retirement. Based on the past 30 years, she estimates inflation at 3.3% compounded annually. She would like to receive 22 years of month-end payments from her retirement fund, which is forecasted to earn 4.8% interest compounded monthly. Based on the results to date, she believes her RRSP can earn 7.75% compounded semiannually during her contributions. She has already saved $48,000, and she will increase each contribution by 0.4%. One month from now, what is the amount of her first monthly RRSP contribution?

Solution

She will make regularly increasing contributions to her RRSP at the end of the monthly payment interval with semi-annual compounding. Therefore, this is a constant growth general ordinary annuity. Calculate her first payment (\(PMT\)).

What You Already Know

Marilyn’s RRSP plan appears in the timeline.

Step 1:

\(PV\) = $45,000, \(IY\) = 3.3%, \(CY\) = 1, Years = 30

Step 2:

\(FV\) = $0, \(IY\) = 4.8%, \(CY\) = 12, \(PY\) = 12, Years = 22, \(Δ\%\) = 3.3%/12 = 0.275% per payment

Step 3:

\(PV\) = $48,000, \(FV_{ORD}\) = Step 2 answer, \(IY\) = 7.75%, \(CY\) = 2, \(PY\) = 12, Years = 30, \(Δ\%\) = 0.4%

How You Will Get There

Step 1:

Move her desired annual income from today to the age of retirement by applying Formula 9.1, Formula 9.2, and Formula 9.3.

Step 2:

Calculate the amount of money needed at the age of retirement by applying Formula 9.1, Formula 11.1, and Formula 12.3.

Step 3:

Deduct her current savings from her required future contributions by calculating the future value of her present savings and deducting it from the step 2 answer by applying Formula 9.1, Formula 9.2, and Formula 9.3. Calculate her regular monthly payment by applying Formula 9.1, Formula 11.1, and Formula 12.1.

Perform

Step 1:

\(i=3.3 \% / 1=3.3 \% ; N=1 \times 30=30 \text { compounds; } FV=\$ 45,000(1+0.033)^{30}=\$ 119,185.15\)

Step 2:

\(i=4.8 \% / 12=0.4 \% ; N=12 \times 22=264 \text { payments } \)

Note that the monthly payment is $119,185.15/12 = $9,932.10

\[PV_{ORD}=\dfrac{\$ 9,932.10}{1+0.00275}\left[\dfrac{1-\left[\dfrac{1+0.00275}{(1+0.004)^{\frac{12}{12}}}\right]^{264}}{\dfrac{(1+0.004)^{\frac{12}{12}}}{1+0.00275}-1}\right]=\$ 2,226,998.08 \nonumber \]

Step 3:

Current Savings:

\(i=7.75 \% / 2=3.875 \% ; N=2 \times 30=60 \text { compounds } ; FV=\$ 48,000(1+0.03875)^{60}=\$ 469,789.65 \)

\(\text { new } FV_{ORD}=\$ 2,226,998.08-\$ 469,789.65=\$ 1,757,208.43 \)

RRSP Payments:

\(i=7.75 \% / 2=3.875 \% ; N=12 \times 30=360 \text { payments } \)

\[\$ 1,757,208.43=PMT(1+0.004)^{360-1}\left[\dfrac{\left[\dfrac{(1+0.03875)^{\frac{2}{12}}}{1+0.004}\right]^{360}-1}{\dfrac{(1+0.03875)^{\frac{2}{12}}}{1+0.004}-1}\right] \nonumber \]

\[\begin{aligned}\$ 1,757,208.43&=PMT(4.191822)[564.766990] \\ \$ 1,757,208.43&=PMT(2,367.403054) \\ \$ 742.25&=PMT\end{aligned} \nonumber \]

Calculator Instructions

| Step | Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|---|

| 1 | END | 30 | 3.3 | -45000 | 0 | Answer: 119,185.1533 | 1 | 1 |

| 3(Savings) | \(\surd\) | 60 | 7.75 | -48000 | \(\surd\) | Answer: 469,789.6504 | 2 | 2 |

On the basis that the rate of inflation is relatively accurate, Marilyn’s first RRSP contribution one month from now is $742.25. Each subsequent payment increases by 0.4% resulting in a balance of $2,226,998.08 (including her current savings) at retirement, from which she makes her first withdrawal of $9,932.10 increasing at 0.275% per month for 22 years.

References

- Pension Investment Association of Canada, Pension Plan Funding Challenges: 2007 PIAC Survey, December 2007, www.piacweb.org/files/Pension%20Plan%20Funding%20Challenges%202007%20PIAC%20Survey%20Dec%2007.pdf (accessed September 26, 2010).