15.2: Other Measures For Making Decisions

- Page ID

- 22160

The previous section explored the three main types of decisions and introduced various techniques for making smart investment decisions. This section revisits Decision #1 (making one choice from multiple options) and Decision #2 (pursuing one course of action) and introduces new characteristics:

- Decision #1: Examine situations where the timelines are not equal in length.

- Decision #2: Determine another profit-focused method of reaching the same decision.

Making Choices for Unequal Timelines

Consider the situation in which you need to buy only one of two $50,000 machines that solve the same problem. Machine #1 has savings of $20,000 per year, while machine #2 has savings of $14,000 per year. However, machine #1 has a life expectancy of four years, while machine #2 has a life expectancy of eight years. Calculating the net present value on these two machines at a 15% cost of capital reveals the \(NPV\) of machine #1 equals $7,100 while the \(NPV\) of machine #2 equals $12,823. Is this a fair comparison? Should machine #2 be selected based on its higher \(NPV\)? The answer is no. The \(NPV\) analysis does not factor in that if you chose machine #1 it must be replaced after four years and would once again have the opportunity to produce more savings over the subsequent four years, thereby offsetting the original difference in \(NPV\).

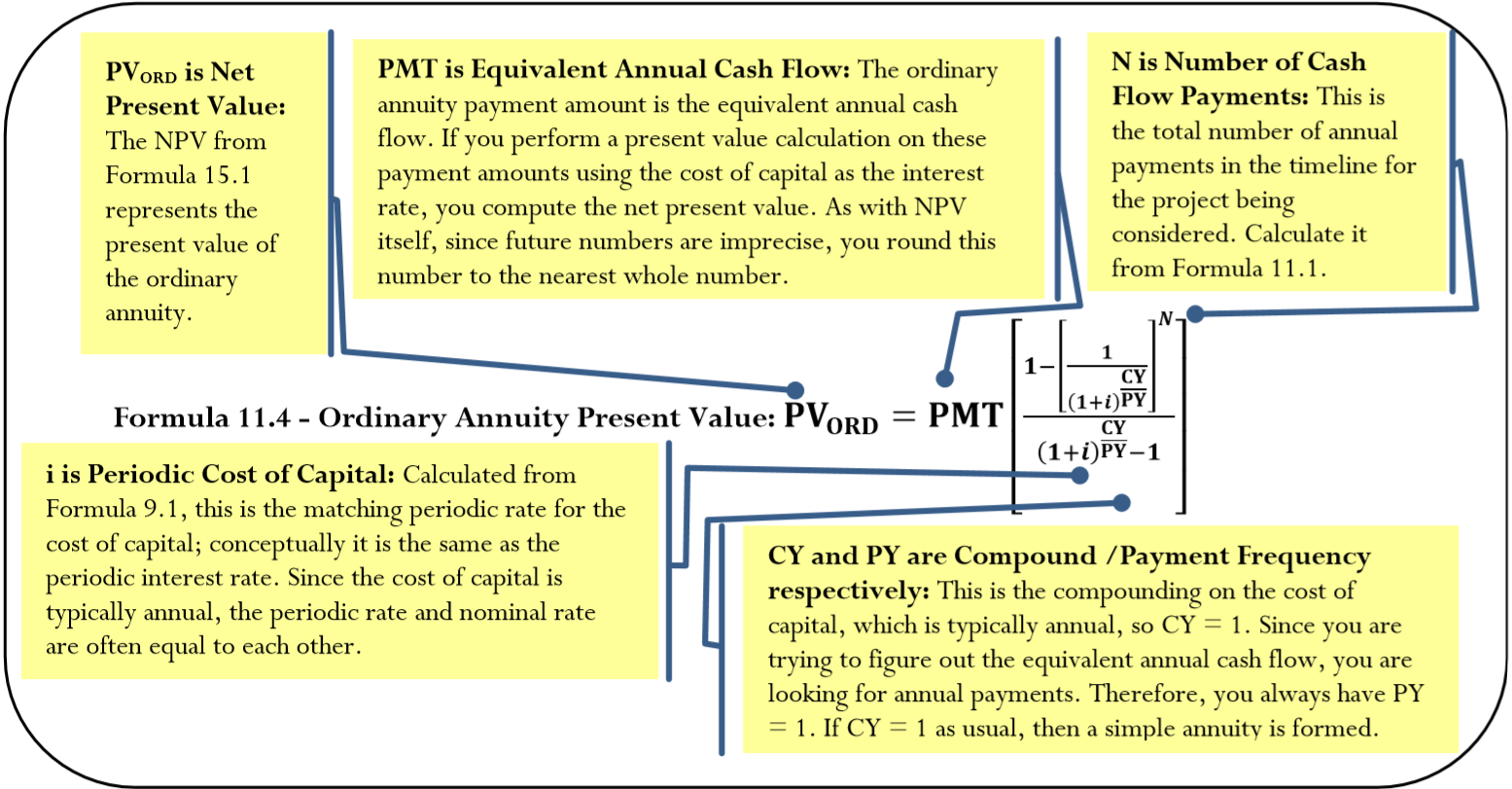

To fairly choose between the alternatives, you need a calculation that can equate two (or more) timelines of different lengths. This requires you to convert the net present value for each alternative into its equivalent annual cash flow. This is an annual annuity payment amount that, when present valued using the cost of capital, arrives at the same \(NPV\) as all of the original cash flows.

The Formula

To arrive at the equivalent annual cash flow, you need to apply two formulas:

- Formula 15.1 calculates the net present value for each alternative you are considering.

- To convert each calculated \(NPV\) into an annual cash flow payment, convert the net present value into an annuity possessing an annual cost of capital and annual end-of-interval payments—or an ordinary simple annuity! Formula 11.4 is reprinted below to illustrate how you can adapt this formula to suit the purposes of the equivalent annual cash flow.

How It Works

Follow these steps to calculate the equivalent annual cash flow:

Step 1: For each alternative project, draw a timeline and calculate the net present value using Formula 15.1 and the techniques discussed in Section 15.1.

Step 2: For each alternative project, calculate the periodic interest rate using Formula 9.1 and the number of annuity payments using Formula 11.1. Then solve Formula 11.4 for \(PMT\).

Step 3: Compare the equivalent annual cash flow of each alternative and make the best decision.

Important Notes

Factoring in the unequal life expectancies of projects is important for situations in which you can choose only one out of many mutually exclusive projects. This is the basis for Decision #1. With respect to the other decisions:

- There is only one timeline to consider in Decision #2 (pursuing one course of action), so the issue of unequal life expectancies does not apply.

- In Decision #3 (making multiple choices under constraints), the net present value ratio provides an adequate means of equating different timelines. You do not need the equivalent annual cash flow.

For each of the following decisions where alternative projects solve the same problem and only one can be chosen (a Decision #1 situation), indicate whether the decision should be made through the comparison of \(NPV\) or equivalent annual cash flows.

- Project #1 with a seven-year life; Project #2 with a seven-year life

- Project #1 with a five-year life; Project #2 with a seven-year life

- Answer

-

- \(NPV\); each alternative has the same time frame.

- Equivalent annual cash flow; each alternative has a different time frame

Recall the earlier situation in which you can buy only one of two equal $50,000 machines. Machine #1 has savings of $20,000 per year, while machine #2 has savings of $14,000 per year. However, machine #1 has a life expectancy of four years, while machine #2 has a life expectancy of eight years. The cost of capital is 15%. Determine which machine should be purchased and the annual benefit of your choice.

Solution

Notice that you are in a Decision #1 situation and need to choose from these two alternatives. Also notice that the cost of capital is known but the timelines are different. You need to use the equivalent annual cash flow to make the decision.

What You Already Know

Step 1:

The timelines for machine #1 and machine #2 appear below, respectively.

Machine #1: \(PV\) = −$50,000, \(IY\) = 15%, \(CY\) = 1, \(PMT\) = $20,000, \(PY\) = 1, \(FV\) = $0, Years = 4

Machine #2: \(PV\) = −$50,000, \(IY\) = 15%, \(CY\) = 1, \(PMT\) = $14,000, \(PY\) = 1, \(FV\) = $0, Years = 8

How You Will Get There

Step 1 (continued):

Each timeline represents an ordinary simple annuity. Calculate the net present value by applying Formulas 9.1, 11.1, 11.4, and Formula 15.1 to each alternative.

Step 2:

For each alternative, calculate the equivalent annual cash flow using Formula 11.4 (rearranging for \(PMT\)).

Step 3:

Make the decision.

Step 4:

Determine on an annual basis how much better your decision is by taking the equivalent annual cash flow of your chosen alternative and subtracting the equivalent annual cash flow of the other alternative.

Perform

Machine #1:

Step 1:

\(i=15 \% / 1=15 \% ; N=1 \times 4=4 \) payments

\[PV_{ORD}=\$ 20,000\left[\dfrac{1-\left[\dfrac{1}{(1+0.15)^{\frac{1}{1}}}\right]^{4}}{(1+0.15)^{\frac{1}{1}-1}}\right]=\$ 57,099.56725 \nonumber \]

\[\begin{aligned}NPV&=\$ 57,099.56725-\$ 50,000\\&=\$ 7,099.56725 \\ &==>\$ 7,100 \end{aligned} \nonumber \]

Step 2:

\[\begin{aligned} PMT&=\dfrac{\$ 7,100}{\left[\dfrac{1-\left[\dfrac{1}{(1+0.15)^{\frac{1}{1}}}\right]^{4}}{(1+0.15)^{\frac{1}{1}}-1}\right]}\\ &=\$2,486.883996\\ &==>\$2,487 \end{aligned} \nonumber \]

Machine #2:

Step 1:

\(i=15 \% / 1=15 \% ; N=1 \times 8=8 \nonumber \) payments

\[PV_{ORD}=\$ 14,000\left[\dfrac{1-\left[\dfrac{1}{(1+0.15)^{\frac{1}{1}}}\right]^{8}}{(1+0.15)^{\frac{1}{1}-1}}\right]=\$ 62,822.50111 \nonumber \]

\[\begin{aligned}NPV&=\$ 62,822.50111-\$ 50,000\\&=\$ 12,822.50111 \\ &==>\$ 12,823\end{aligned} \nonumber \]

Step 2:

\[\begin{aligned} PMT&=\dfrac{\$ 12,823}{\left[\dfrac{1-\left[\dfrac{1}{(1+0.15)^{\frac{1}{1}}}\right]^{8}}{(1+0.15)^{\frac{1}{1}}-1}\right]}\\ &=\$2,857.606699\\ &==>\$2,858 \end{aligned} \nonumber \]

Step 3:

The best choice is machine #2 because it has a higher equivalent annual cash flow of $2,858.

Step 4:

Annual benefit = Machine #2 − Machine #1 = $2,858 − $2,487 = $371

Calculator Instructions

| Cash Flows | ||||

|---|---|---|---|---|

| Machine #1 | Machine #2 | |||

| Cash Flow | Amount (\(CXX\)) | Frequency (\(FXX\)) | Amount (\(CXX\)) | Frequency (\(FXX\)) |

| \(CF0\) | -50000 | N/A | -50000 | N/A |

| C01 & F01 | 20000 | 4 | 14000 | 8 |

| \(NPV\) | ||

|---|---|---|

| Machine #1 | Machine #2 | |

| \(I\) | 15 | 15 |

| \(NPV\) | Answer: 7,099.567254 | Answer: 12,822.50111 |

| Machine | Mode | \(N\) | \(I/Y\) | \(PV\) | \(PMT\) | \(FV\) | \(P/Y\) | \(C/Y\) |

|---|---|---|---|---|---|---|---|---|

| 1 | END | 4 | 15 | -7100 | Answer: 2,486.883996 | 0 | 1 | 1 |

| 2 | \(\surd\) | 8 | \(\surd\) | -12823 | Answer: 2,857.606699 | 0 | \(\surd\) | \(\surd\) |

The smart decision is to purchase machine #2 because it produces the highest equivalent annual cash flow of $2,858, which represents savings of $371 more per year than machine #1.

Internal Rate of Return

Another method of reaching a decision when choosing whether to pursue a single course of action (Decision #2) involves percentages. While the \(NPV\) calculations in Section 15.1 provide an exact monetary magnitude of the project, the common mindset in business focuses on profitability as a percentage and not a dollar amount. Thus, decisions are based on the internal rate of return for a project, or IRR for short. The IRR is the annual percentage rate of return on the investment being made such that the net present value of all cash flows in a particular project equals zero.

To interpret the IRR, examine the \(NPV\) decision criteria and the relationship to the IRR:

- If the net present value is greater than or equal to $0, pursue the project.

- If the \(NPV\) is more than zero, the definition of IRR requires you to find a rate of return such that your present value becomes zero. Mathematically this means that a higher discount rate must be used to calculate your present value. In other words, the IRR is greater than the cost of capital.

- If the \(NPV\) equals zero, by definition the cost of capital and the IRR are the same value.

- If the net present value is less than $0, do not pursue the project. The IRR requires you to find a rate of return where the present value becomes zero. Mathematically this means that a lower discount rate must be used to calculate your present value. In other words, the IRR is less than the cost of capital.

This table summarizes how to decide whether to pursue a single course of action using the IRR method instead of the \(NPV\) method.

| If... | So... | Then... | Decision |

|---|---|---|---|

| \(NPV>0\) | IRR > Cost of Capital | It is profitable since it makes enough money to cover the costs | Pursue the project |

| \(NPV=0\) | IRR > Cost of Capital | It breaks even and just pays the bills | This is the minimum financial condition to pursue the project |

| \(NPV<0\) | IRR > Cost of Capital | It is unprofitable and does not make enough money to cover the costs | Do not pursue the project |

The Formula

Solving for the internal rate of return requires you to calculate the annually compounded interest rate for the project. For annuities, substituting and rearranging Formula 15.1 produces:

\[NPV=\text { (Present Value of All Future Cash Flows) - (Initial Investment) } \nonumber \]

\[\$0=PMT\left[\dfrac{1-\left[\dfrac{1}{\left(1+i\right )^{\frac{CY}{PY}}} \right ]^N}{(1+i)^{\frac{CY}{PY}}-1}\right ] -(\text { Initial Investment }) \nonumber \]

\[\text { Initial Investment }=PMT\left[\begin{array}{c}{1-\left[\dfrac{1}{(1+i)^{\frac{CY}{PY}}}\right]^{N}} \\ (1+i)^{\frac{CY}{PY}}-1\end{array}\right] \nonumber \]

The only algebraic method to solve this general formula for the periodic interest rate is through trial and error, which is time consuming and inefficient. The same algebraic problem exists if your cash flows consist of multiple lump-sum amounts at different points in time. Assume you have inflows of $15,000 and $10,000 at the end of years one and two, respectively. Taking Formula 15.1 you have:

\[NPV=\text { (Present Value of All Future Cash Flows) - (Initial Investment) } \nonumber \]

\[\$ 0=\left(\$ 15,000 /(1+i)^{1}+\$ 10,000 /(1+i)^{2}\right)-(\text { Initial Investment }) \nonumber \]

\[\text { Initial Investment }=\$ 15,000 /(1+i)^{1}+\$ 10,000 /(1+i)^{2} \nonumber \]

It is algebraically difficult to solve this formula for the periodic interest rate.

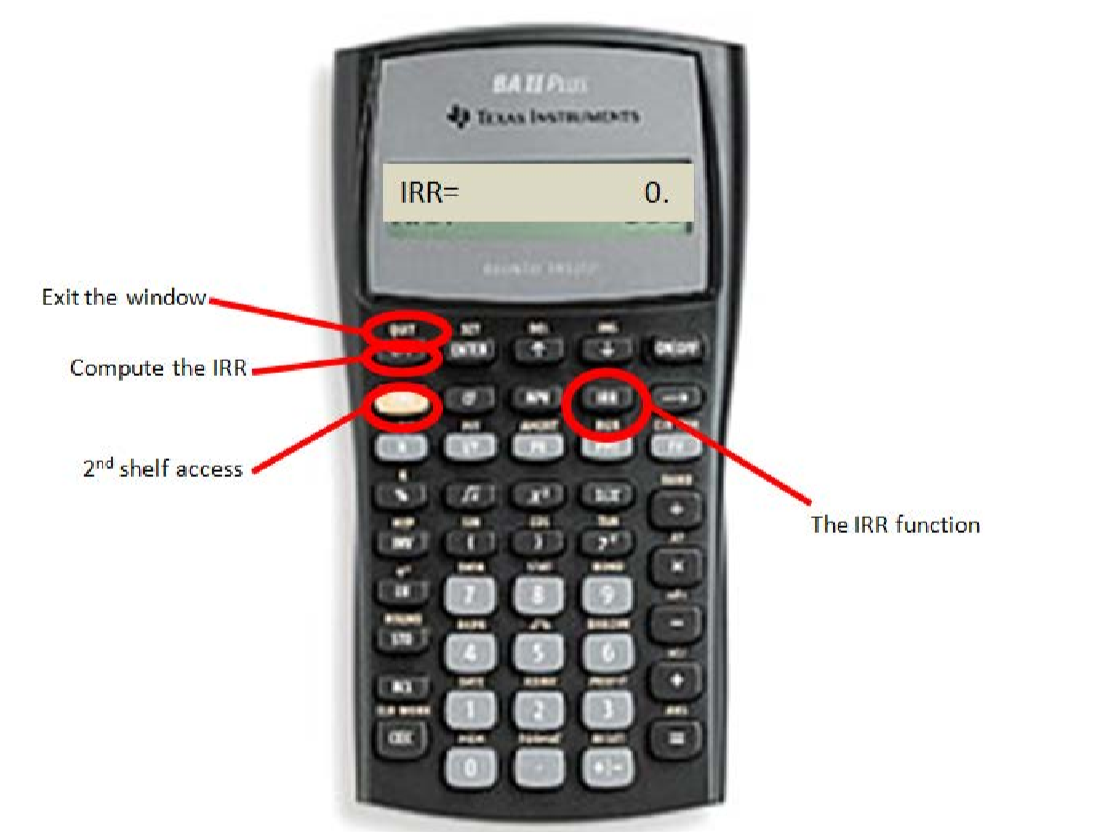

Therefore, using the same process as in Section 11.6, you should let the BAII Plus calculator perform the trial and error and arrive at the solution. Note that Excel can also perform this calculation, and the formula is pre-programmed into the chapter template.

How It Works

Follow these steps to solve for the internal rate of return:

Step 1: Draw a timeline to illustrate the cash flows involved in the project.

Step 2: If using manual trial and error, set up the appropriate algebraic formula to arrive at an \(NPV\) of $0 and start the sequence of iterations to generate the solution. Alternatively, use technology such as the BAII Plus calculator by entering the cash flows and solving for the IRR.

Step 3: Compare the IRR to the cost of capital and make a decision.

Important Notes

Using the IRR Function on the BAII Plus Calculator. Use the IRR function in conjunction with the CF (cash flow) function. Once you have entered all cash flows, activate the IRR function by pressing the IRR key followed by the CPT button to perform the calculation. The output is a percentage in percent format. To exit the window, press 2nd Quit. Recall that because of the trial-and-error method required, the calculator may briefly hesitate before displaying the solution.

Things To Watch Out For

When making decisions, you use the internal rate of return only to figure out if one particular path should be followed or not (which is Decision #2). The internal rate of return should not be used when making one choice from multiple options (Decision #1) or when making multiple choices under constraints (Decision #3). This rule is in place for two reasons:

- The Cost of Capital Is Ignored. The IRR does not factor in the cost of capital in its computations. Recall that the fundamental concept of time value of money requires all money to be on the same date using an appropriate rate of interest—the cost of capital—before any decision can be made. Therefore, if you have not factored in the cost of capital, then your analysis is incomplete and choosing between different alternatives based solely on the IRR is flawed.

- The Magnitude of the Decision Is Ignored. It can easily happen that an alternative has a high IRR but a low \(NPV\). For example, using a cost of capital of 10% consider two alternatives. Alternative A invests $1 and one year later returns $1.50. The IRR is 50%, while the \(NPV\) is $0.36. Alternative B invests $1,000 and one year later returns $1,250. The IRR is 25%, while the \(NPV\) is $136.36. If choosing between these two options based on the IRR, you select Alternative A, resulting in a net present value that is $136 lower than for Alternative B.

In each of the following situations, determine whether the project should be pursued or not.

- Cost of capital = 15%; IRR = 17%

- Cost of capital = 12%; IRR = 9%

- Cost of capital = 14%; IRR = 14%

- Answer

-

- Pursue it; IRR > cost of capital

- Do not pursue it; IRR < cost of capital

- Minimum condition to pursue it; IRR = cost of capital (breaks even

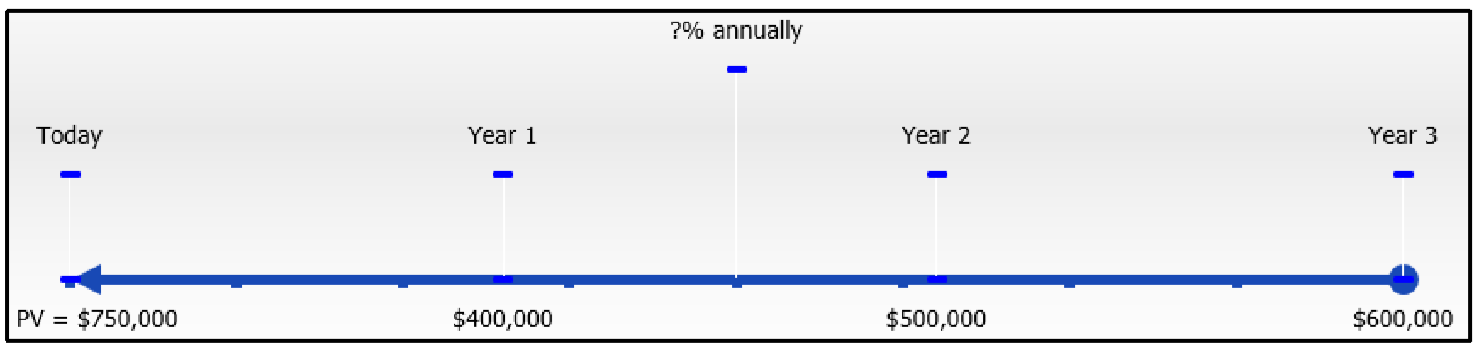

Tim Hortons has purchased the lease on a three-year onsite concession space in the cafeteria at a local college for $750,000. The franchise is expected to earn $400,000, $500,000, and $600,000 in profits per year for the first three years, respectively.

- What is the investment's internal rate of return?

- If the cost of capital is 20%, did Tim Hortons make a smart financial decision?

Solution

You need to calculate the internal rate of return (IRR) for this project. Once calculated, you can compare it to the provided cost of capital to evaluate the decision.

What You Already Know

Step 1:

The timeline for this project appears below.

\(PV\) = $750,000, \(CY\) = 1

\(C01\) = $400,000, Years = 1

\(C02\) = $500,000, Years = 2

\(C03\) = $600,000, Years = 3

How You Will Get There

Step 2:

This project involves multiple lump-sum cash flows, so apply Formulas 9.2 and 9.3 (rearranged for \(PV\)). Substitute into the rearranged Formula 15.1. Algebraically, this must be solved through trial and error for i (note that \(i = IY\) since the compounding frequency is 1). Alternatively, use the cash flow and internal rate of return function on your calculator.

Step 3:

Compare the IRR to the cost of capital to make the decision.

Perform

Step 2:

Cash Flow 1: \(N=1 \times 1=1 \text { compound; } PV=\$ 400,000 \div(1+i)^{1} \)

Cash Flow 2: \(N=1 \times 2=2 \text { compounds; } PV=\$ 500,000 \div(1+i)^{2} \)

Cash Flow 3: \(N=1 \times 3=3 \text { compounds; } PV=\$ 600,000 \div(1+i)^{3} \)

\(\$ 750,000=\$ 400,000 \div(1+i)^{1}+\$ 500,000 \div(1+i)^{2}+\$ 600,000 \div(1+i)^{3} \)

Through trial and error or by using the calculator (see instructions below), the calculated solution is: \(IY\) = 40.9235%

Step 3:

40.9235% > 20% ==> smart decision

Calculator Instructions

| Cash Flow | Amount (\(CXX\)) | Frequency (\(FXX\)) |

|---|---|---|

| CF0 | -750000 | N/A |

| C01 & F01 | 400000 | 1 |

| C02 & F02 | 500000 | 1 |

| C03 & F03 | 600000 | 1 |

IRR

Answer: 40.923472

Since the internal rate of return on this project is 40.9235%, which far exceeds the cost of capital of 20%, Tim Hortons made a very smart financial decision in pursuing this project.