6.4: Present Value of an Annuity and Installment Payment

- Page ID

- 37878

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)In this section, you will learn to:

- Find the present value of an annuity.

- Find the amount of installment payment on a loan.

PRESENT VALUE OF AN ANNUITY

In Section 6.2, we learned to find the future value of a lump sum, and in Section 6.3, we learned to find the future value of an annuity. With these two concepts in hand, we will now learn to amortize a loan, and to find the present value of an annuity.

The present value of an annuity is the amount of money we would need now in order to be able to make the payments in the annuity in the future. In other word, the present value is the value now of a future stream of payments.

We start by breaking this down step by step to understand the concept of the present value of an annuity. After that, the examples provide a more efficient way to do the calculations by working with concepts and calculations we have already explored in Sections 6.2 and 6.3.

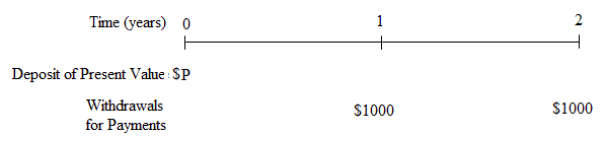

Suppose Carlos owns a small business and employs an assistant manager to help him run the business. Assume it is January 1 now. Carlos plans to pay his assistant manager a $1000 bonus at the end of this year and another $1000 bonus at the end of the following year. Carlos’ business had good profits this year so he wants to put the money for his assistant’s future bonuses into a savings account now. The money he puts in now will earn interest at the rate of 4% per year compounded annually while in the savings account.

How much money should Carlos put into the savings account now so that he will be able to withdraw $1000 one year from now and another $1000 two years from now?

At first, this sounds like a sinking fund. But it is different. In a sinking fund, we put money into the fund with periodic payments to save to accumulate to a specified lump sum that is the future value at the end of a specified time period.

In this case we want to put a lump sum into the savings account now, so that lump sum is our principal, \(\mathrm{P}\). Then we want to withdraw that amount as a series of period payments; in this case the withdrawals are an annuity with $1000 payments at the end of each of two years.

We need to determine the amount we need in the account now, the present value, to be able to make withdraw the periodic payments later.

We use the compound interest formula from Section 6.2 with \(r\) = 0.04 and \(n\) = 1 for annual compounding to determine the present value of each payment of $1000.

Consider the first payment of $1000 at the end of year 1. Let P1 be its present value

\[\$ 1000=P_{1}(1.04)^{1} \text { so } P_{1}=\$ 961.54 \nonumber \]

Now consider the second payment of $1000 at the end of year 2. Let P2 is its present value

\[\$ 1000=P_{2}(1.04)^{2} \text { so } P_{2}=\$ 924.56 \nonumber \]

To make the $1000 payments at the specified times in the future, the amount that Carlos needs to deposit now is the present value \(P=P_{1}+P_{2}=\$ 961.54+\$ 924.56=\$ 1886.10\)

The calculation above was useful to illustrate the meaning of the present value of an annuity.

But it is not an efficient way to calculate the present value. If we were to have a large number of annuity payments, the step by step calculation would be long and tedious.

Example \(\PageIndex{1}\) investigates and develops an efficient way to calculate the present value of an annuity, by relating the future (accumulated) value of an annuity and its present value.

Suppose you have won a lottery that pays $1,000 per month for the next 20 years. But, you prefer to have the entire amount now. If the interest rate is 8%, how much will you accept?

Solution

This classic present value problem needs our complete attention because the rationalization we use to solve this problem will be used again in the problems to follow.Consider, for argument purposes, that two people Mr. Cash, and Mr. Credit have won the same lottery of $1,000 per month for the next 20 years. Mr. Credit is happy with his $1,000 monthly payment, but Mr. Cash wants to have the entire amount now.

Our job is to determine how much Mr. Cash should get. We reason as follows:

If Mr. Cash accepts P dollars, then the P dollars deposited at 8% for 20 years should yield the same amount as the $1,000 monthly payments for 20 years. In other words, we are comparing the future values for both Mr. Cash and Mr. Credit, and we would like the future values to equal.

Since Mr. Cash is receiving a lump sum of \(x\) dollars, its future value is given by the lump sum formula we studied in Section 6.2, and it is

\[\mathrm{A}=\mathrm{P}(1+.08 / 12)^{240} \nonumber \]

Since Mr. Credit is receiving a sequence of payments, or an annuity, of $1,000 per month, its future value is given by the annuity formula we learned in Section 6.3. This value is

\[\mathrm{A}=\frac{\$ 1000\left[(1+.08 / 12)^{240}-1\right]}{.08 / 12} \nonumber \]

The only way Mr. Cash will agree to the amount he receives is if these two future values are equal. So we set them equal and solve for the unknown.

\[\begin{array}{l}

\mathrm{P}(1+.08 / 12)^{240}=\frac{\$ 1000\left[(1+.08 / 12)^{240}-1\right]}{.08 / 12} \\

\mathrm{P}(4.9268)=\$ 1000(589.02041) \\

\mathrm{P}(4.9268)=\$ 589020.41 \\

\mathrm{P}=\$ 119,554.36

\end{array} \nonumber \]

The present value of an ordinary annuity of $1,000 each month for 20 years at 8% is $119,554.36

The reader should also note that if Mr. Cash takes his lump sum of \(\mathrm{P}\) = $119,554.36 and invests it at 8% compounded monthly, he will have an accumulated value of \(\mathrm{A}\)=$589,020.41 in 20 years.

INSTALLMENT PAYMENT ON A LOAN

If a person or business needs to buy or pay for something now (a car, a home, college tuition, equipment for a business) but does not have the money, they can borrow the money as a loan.

They receive the loan amount called the principal (or present value) now and are obligated to pay back the principal in the future over a stated amount of time (term of the loan), as regular periodic payments with interest.

Example \(\PageIndex{2}\) examines how to calculate the loan payment, using reasoning similar to Example \(\PageIndex{1}\).

Find the monthly payment for a car costing $15,000 if the loan is amortized over five years at an interest rate of 9%.

Solution

Again, consider the following scenario:Two people, Mr. Cash and Mr. Credit, go to buy the same car that costs $15,000. Mr. Cash pays cash and drives away, but Mr. Credit wants to make monthly payments for five years.

Our job is to determine the amount of the monthly payment. We reason as follows:

If Mr. Credit pays m dollars per month, then the m dollar payment deposited each month at 9% for 5 years should yield the same amount as the $15,000 lump sum deposited for 5 years.

Again, we are comparing the future values for both Mr. Cash and Mr. Credit, and we would like them to be the same.

Since Mr. Cash is paying a lump sum of $15,000, its future value is given by the lump sum formula, and it is

\[\$ 15,000(1+.09 / 12)^{60} \nonumber \]

Mr. Credit wishes to make a sequence of payments, or an annuity, of \(x\) dollars per month, and its future value is given by the annuity formula, and this value is

\[\frac{\mathrm{x}\left[(1+.09 / 12)^{60}-1\right]}{.09 / 12} \nonumber \]

We set the two future amounts equal and solve for the unknown.

\[\begin{array}{l}

\$ 15,000(1+.09 / 12)^{60}=\frac{m\left[(1+.09 / 12)^{60}-1\right]}{.09 / 12} \\

\$ 15,000(1.5657)=m(75.4241) \\

\$ 311.38=m

\end{array} \nonumber \]

Therefore, the monthly payment needed to repay the loan is $311.38 for five years.

SECTION 6.4 SUMMARY

We summarize the method used in examples \(\PageIndex{1}\) and \(\PageIndex{2}\) below.

The Equation to Find the Present Value of an Annuity,

Or the Installment Payment for a Loan

If a payment of \(m\) dollars is made in an account \(n\) times a year at an interest \(r\), then the present value \(\mathrm{P}\) of the annuity after \(t\) years is

\[\mathbf{P}(\mathbf{1}+\mathbf{r} / \mathbf{n})^{\mathbf{n} \mathbf{t}}=\frac{\mathbf{m}\left[(\mathbf{1}+\mathbf{r} / \mathbf{n})^{\mathbf{n} \mathbf{t}}-\mathbf{1}\right]}{\mathbf{r} / \mathbf{n}} \nonumber \]

When used for a loan, the amount \(\mathrm{P}\) is the loan amount, and \(m\) is the periodic payment needed to repay the loan over a term of \(t\) years with \(n\) payments per year.

If the present value or loan amount is needed, solve for \(P\)

If the periodic payment is needed, solve for \(m\).

Note that the formula assumes that the payment period is the same as the compounding period. If these are not the same, then this formula does not apply.

Finally, we note that many finite mathematics and finance books develop the formula for the present value of an annuity differently.

Instead of using the formula:

\[\mathrm{P}(1+\mathrm{r} / \mathrm{n})^{\mathrm{nt}}=\frac{\mathrm{m}\left[(1+\mathrm{r} / \mathrm{n})^{\mathrm{nt}}-1\right]}{\mathrm{r} / \mathrm{n}} \label{6.4.1} \]

and solving for the present value \(\mathrm{P}\) after substituting the numerical values for the other items in the formula, many textbooks first solve the formula for \(\mathrm{P}\) in order to develop a new formula for the present value. Then the numerical information can be substituted into the present value formula and evaluated, without needing to solve algebraically for \(\mathrm{P}\).

Alternate Method to find Present Value of an Annuity

Starting with formula \ref{6.4.1}: \(\mathrm{P}(1+\mathrm{r} / \mathrm{n})^{\mathrm{nt}}=\frac{\mathrm{m}\left[(1+\mathrm{r} / \mathrm{n})^{\mathrm{nt}}-1\right]}{\mathrm{r} / \mathrm{n}}\)

Divide both sides by \((1+r / n)^{n t}\) to isolate \(\mathrm{P}\), and simplify

\[P=\frac{m\left[(1+r / n)^{n t}-1\right]}{r / n} \cdot \frac{1}{(1+r / n)^{n t}} \nonumber \]

\[P=\frac{m\left[1-(1+r / n)^{-n t}\right]}{r / n} \label{6.4.2} \]

The authors of this book believe that it is easier to use formula \ref{6.4.1} at the top of this page and solve for \(\mathrm{P}\) or \(m\) as needed. In this approach there are fewer formulas to understand, and many students find it easier to learn. In the problems the rest of this chapter, when a problem requires the calculation of the present value of an annuity, formula \ref{6.4.1} will be used.

However, some people prefer formula \ref{6.4.2}, and it is mathematically correct to use that method. Note that if you choose to use formula \ref{6.4.2}, you need to be careful with the negative exponents in the formula. And if you needed to find the periodic payment, you would still need to do the algebra to solve for the value of m.

It would be a good idea to check with your instructor to see if he or she has a preference. In fact, you can usually tell your instructor’s preference by noting how he or she explains and demonstrates these types of problems in class.