4.5: Compounding Interest Makes Cents

- Page ID

- 148774

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)INTRODUCTION

Recall the following information about CDs from Preparation 4.5. Take a minute to read through it again below and, if necessary, discuss any difficulties in your group.

A Certificate of Deposit (CD) is a type of investment used by many people because it is very safe and predictable. CDs can be purchased through banks and other financial institutions. The U.S. Security and Exchange Commission gives the following information about CDs.

The ABCs of CDs

A CD is a special type of deposit account with a bank or thrift institution that typically offers a higher rate of interest than a regular savings account. Unlike other investments, CDs feature federal deposit insurance up to $250,000.

When you purchase a CD, you invest a fixed sum of money for a fixed period of time—six months, one year, five years, or more—and, in exchange, the issuing bank pays you interest, typically at regular intervals. When you cash in or redeem your CD, you receive the money you originally invested, plus any accrued interest. If you redeem your CD before it matures, you may have to pay an “early withdrawal” penalty or forfeit a portion of the interest you earned …

At one time, most CDs paid a fixed interest rate until they reached maturity. But, like many other products in today’s markets, CDs have become more complicated. Investors may now choose among variable-rate CDs, long-term CDs, and CDs with other special features.

SPECIFIC OBJECTIVES

By the end of this collaboration, you should understand that

- compounding is repeated multiplication by a compounding factor.

- compounding is best expressed in terms of exponential growth, using exponential notation.

- exponential growth models the compounding of interest on an initial investment.

By the end of this collaboration, you should be able to

- calculate the earnings on a principal investment with annual compound interest.

- write a formula for annual compound interest.

- compare and contrast linear and exponential models.

PROBLEM SITUATION: THE FIVE-YEAR CD

Suppose you invest $1,000 principal (the original deposit in an investment) into a certificate of deposit (CD) with a five-year term (the agreed upon period of time that money is in an investment) that pays a 5% annual interest rate. The compounding period is one year. Recall that in compound interest, interest is added to the starting principal and accrues after set periods of time through the duration of the whole term.

(1) How much money will you have in your account at the end of the five-year term? (Be ready to explain your calculations.) Use the table below to find a pattern and develop a formula to model the total amount accrued in a CD with annual compounding after t years, if the principal = $1,000 and the APR = 5%. Round figures in the Amount Accrued column to two decimal places.

|

Term |

Calculation |

Amount Accrued |

|

1 year |

$1,000 + $1,0000.05 = $1,000(1 + 0.05) = $1,000*1.05 |

$1,050.00 |

|

2 years |

($1,000*1.05)(1.05) = $1,000(1.05)2 |

|

|

3 years |

||

|

4 years |

||

|

5 years |

||

|

… |

||

|

t years |

(2) Is your formula from Question 1 linear? Explain your reasoning.

(3) Using the formula and patterns you developed when answering Question 1, work in your group to fill out the following table. Round figures in the Amount Accrued column to two decimal places.

|

Term |

Calculation |

Amount Accrued |

|

10 years |

||

|

20 years |

||

|

30 years |

||

|

40 years |

||

|

50 years |

(4) (a) Use the values from the table above to create a graph of the model you developed. Note: If completing this problem online, follow the instructions given online to create your graph.

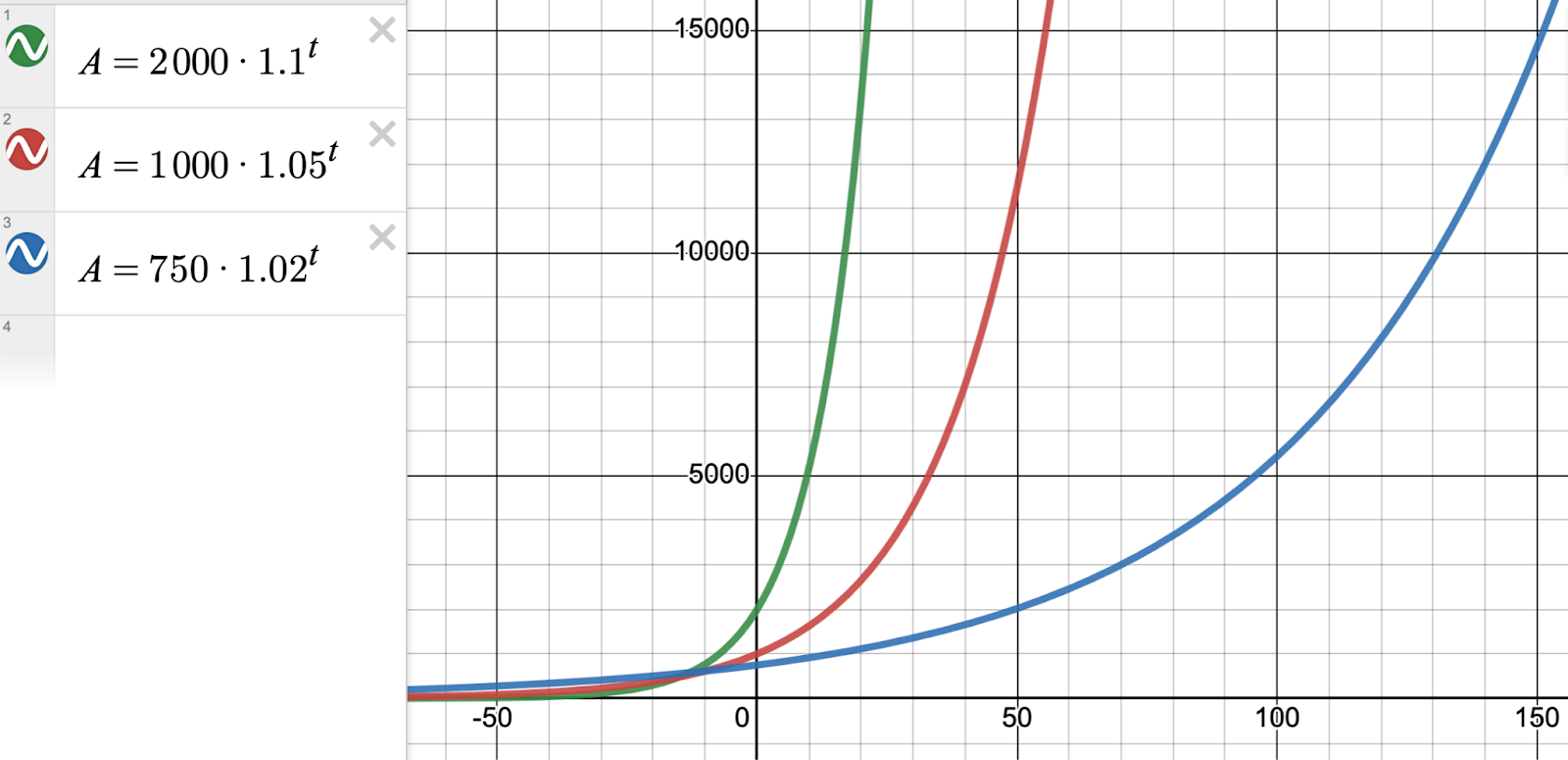

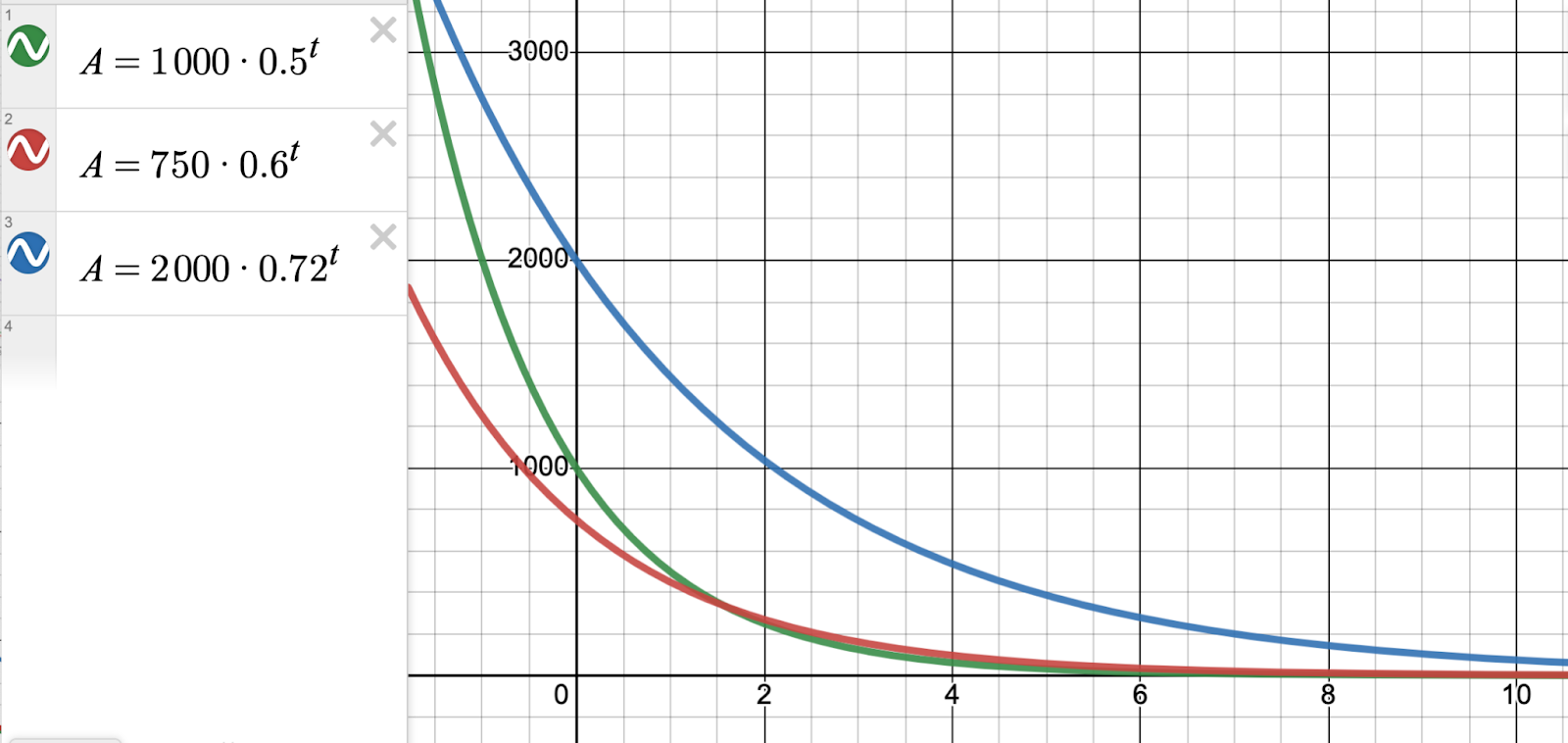

Behavior of Exponential Growth/Decay

Note from the graph in Question 4a, that the growth is very small at first, but then it changes dramatically. Here are some other graphs that illustrate both exponential growth and exponential decay:

Exponential growth (increasing rate of change)

Exponential decay (decreasing rate of change)

(b) Use the information in the table below to plot a graph of the model. Note: If completing this problem online, follow the instructions given online to create your graph.

- You have $1,000 in savings and add $20 each year.

- Equation: A = 1,000 + 20n where A = amount ($) and n = number of years

|

Term |

Calculation |

Amount Accrued |

|

1 year |

1,000 + 20 |

$1,020 |

|

2 years |

(1,000 + 20) + 20 = $1,000 + 2*20 |

$1,040 |

|

3 years |

(1,000 + 20 + 20) + 20 = $1,000 + 3*20 |

$1,060 |

|

4 years |

(1,000 + 20 + 20 + 20) + 20 = $1,000 + 4*20 |

$1,080 |

|

5 years |

(1,000 + 20 + 20 + 20 + 20) + 20 = $1,000 + 5*20 |

$1,100 |

(5) Write a general formula that could be used to find the accrued amount (A) for a CD with annual compounding. Let P = the principal, r = the annual interest rate as a decimal, and t = number of years of investment.

MAKING CONNECTIONS

Record the important mathematical ideas from the discussion.