4.2: Personal Income Tax (The Taxman Taketh)

- Page ID

- 22084

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)You have just filled out your income tax return, where you see that your total payable for the year is more than $5,000. You are glad you do not have to pay this lump sum all at once! Instead, almost all of it has actually been paid already: Your employer has made regular deductions from each paycheque to cover your federal and provincial taxes.

In Canada, businesses are taxed differently than individuals and there are many nuances and complexities to address. For these reasons, this textbook does not cover business taxes, which require a course in corporate taxes.

For individuals, taxes are relatively straightforward. This section of the book uses the 2013 tax year federal and provincial/territorial personal income tax brackets to calculate the amount of these taxes that are ultimately deducted from your gross earnings. You can find current-year tax brackets at www.taxtips.ca/marginaltaxrates.htm.

Federal and Provincial/Territorial Tax Brackets and Tax Rates

Personal income tax is a tax on gross earnings levied by both the federal and provincial/territorial governments. All of Canada uses a progressive tax system in which the tax rate increases as the amount of income increases; however, the increased tax rates apply only to income amounts above minimum thresholds. Thus, higher income earners pay higher marginal tax rates than lower income earners. The format is similar to a graduated commission structure.

The federal and provincial/territorial governments offer a basic personal amount, which is the amount of income for which the wage earner is granted a tax exemption. In other words, it is tax-free income. This is designed to help low-income earners in Canada. Tax brackets are adjusted annually federally and in most provinces and territories to reflect increases in the cost of living, as measured by the consumer price index (CPI).

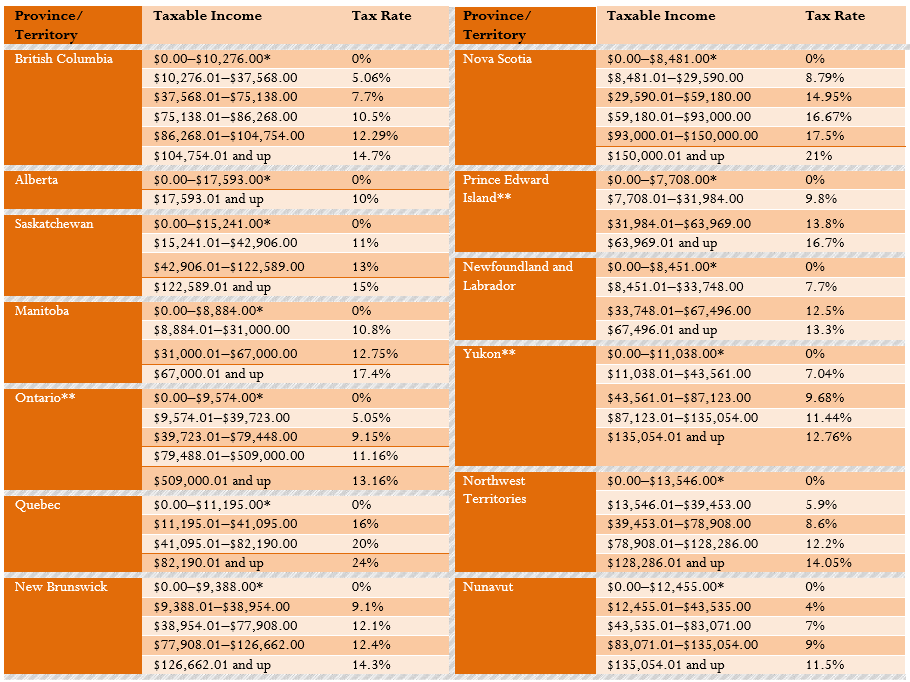

2013 Provincial Taxes

*There are additional income surtaxes in these provinces and Yukon.

**These surtaxes are not covered in this textbook. These amounts represent the basic personal amount.

2013 Federal Taxes

| Taxable Income | Tax Rate |

|---|---|

| $0.00–$11,038.00* | 0% |

| $11,038.01–$43,561.00 | 15% |

| $43,561.01–$87,123.00 | 22% |

| $87,123.01–$135,054.00 | 26% |

| $135,054.01 and up | 29% |

*This is the basic personal amount.

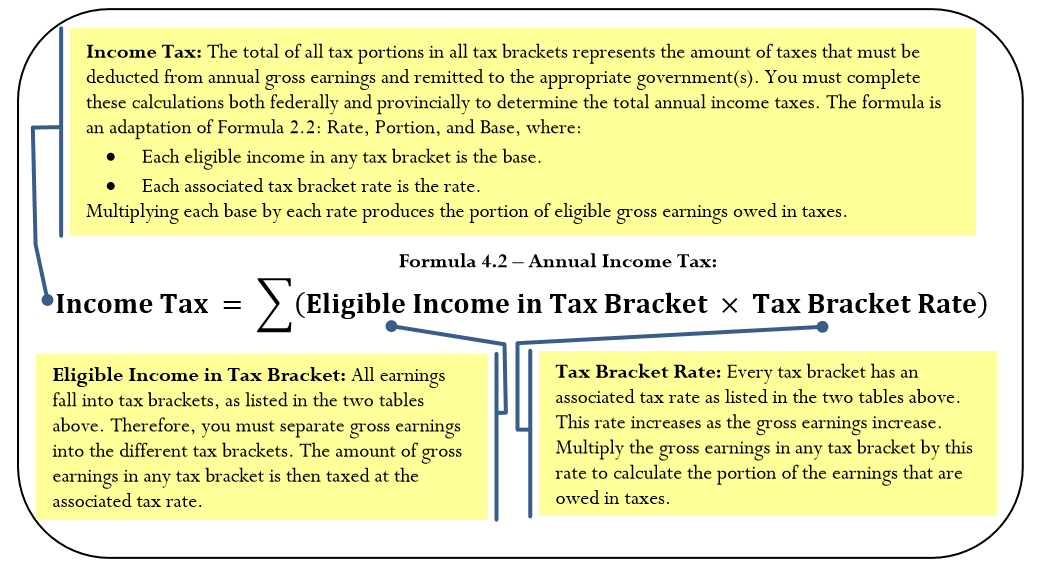

The Formula

To calculate the income taxes for any individual, you must total all taxes from all eligible gross earnings in every tax bracket. Formula 4.2 shows the calculation.

How It Works

To calculate the total annual income tax owing in any tax year, follow these steps:

Step 1: Determine the total amount of gross earnings that are taxable for the individual.

Step 2: Calculate the federal income taxes owing. Using the federal tax table, split the gross earnings into each of the listed tax brackets, then calculate the taxes owing in each tax bracket by multiplying the income in the bracket and the tax rate. Round any tax amounts to two decimals.

Step 3: Calculate the provincial/territorial income taxes owing. Repeat the same process as in step 2, but use the appropriate tax brackets from the provincial tax table instead. Round any tax amounts to two decimals.

Step 4: Calculate the total annual income taxes owing by applying Formula 4.2. This means adding all calculated tax amounts from both steps 2 and 3 together.

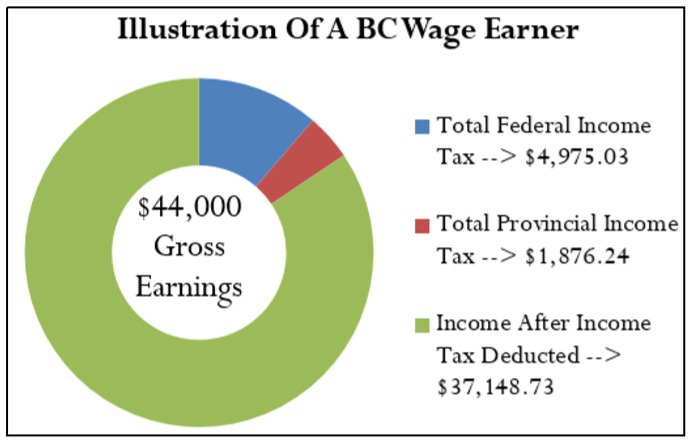

Assume you live in British Columbia and your taxable gross income is $44,000. Here is how you would calculate your annual total federal and provincial taxes:

Step 1: The gross earnings are $44,000.

Step 2: Federally, your income falls into the first three brackets. Your first $11,038 is taxed at 0%; therefore, there are no income taxes on this amount. The next $32,523 (from $11,038.01 to $43,561.00) is taxed at 15%, thus \(\$ 32,523 \times 15 \%=\$ 4,878.45\). The last $439 (from $43,561.01 to $44,000.00) is taxed at 22%, thus \(\$ 439 \times 22 \%=\$ 96.58\).

Step 3: Provincially, your income falls into the first three brackets for British Columbia. Your first $10,276 is taxed at 0%; therefore, there are no income taxes on this amount. The next $27,292 (from $10,276.01 to $37,568.00) is taxed at 5.06%, thus \(\$ 27,292 \times 5.06 \%=\$ 1,380.98\). The last $6,432 (from $37,568.01 to $44,000) is taxed at 7.7%, thus \(\$ 6,432 \times 7.7 \%=\$ 495.26\).

Step 4: Your total federal income tax is \(\$ 0.00+\$ 4,878.45+\$ 96.58=\$ 4,975.03\). Your total provincial income tax is \(\$ 0.00+\$ 1,380.98+\$ 495.26=\$ 1,876.24\). Applying Formula 4.1, \(\text { income tax}=\$ 4,975.03+\$ 1,876.24=\$ 6,851.27\), which is the amount that will be deducted from total gross earnings.

Things To Watch Out For

Have you ever heard someone say, "I earn more income and moved to a higher tax bracket, so now I am earning less money and my paycheque is lower"? The progressive tax system used in Canada makes this statement untrue.

Remember that tax rates apply only to the portion of the gross earnings in the tax bracket and are not retroactive to lower levels of income. For example, if your taxable gross income increased from $80,000 to $88,000, your highest tax bracket is now 26% instead of 22%. However, your federal income tax is not calculated at 26% for your entire income. Rather, the first $11,038 is tax free, the next $32,523 is taxed at 15%, the next $43,562 is taxed at 22%, and the final $877 is taxed at 26%.

Paths To Success

It is sometimes beneficial to pre-calculate the total income taxes in any tax bracket under the assumption that the individual’s income comprises the entire tax bracket. This technique is particularly useful when repetitive calculations are required, such as determining the federal income taxes for each employee in an entire company. For example, the second federal tax bracket extends from $11,038.01 to $43,561, representing $32,523 of employee income. Since this bracket is taxed at 15%, someone who earns a higher income always owes the full amount of tax in this category, which is \(\$ 32,523 \times 15 \%=\$ 4,878.45\). The next tax bracket covers $43,561.01 to $87,123, representing $43,562 of income. Someone earning a higher income always owes the full amount of tax in this category, which is \(\$ 43,562 \times 22 \%=\$ 9,583.64\).

Assume taxable gross earnings of $88,000. With your pre-calculated income taxes in each bracket, you know the income taxes in the first three tax brackets are $0, $4,878.45, and $9,583.64, or $14,462.09 in total. You only need to calculate the tax on the portion of income in the final tax bracket of \(\$ 877 \times 26 \%=\$ 228.02\). The grand total is \(\$ 14,462.09+\$ 228.02=\$ 14,690.11\).

A Canadian wage earner has taxable gross income of $97,250. Calculate the federal and provincial annual income taxes individually and then sum the amounts to calculate the total annual income taxes if the wage earner lives in

- Ontario

- New Brunswick

- Alberta

Solution

For each of the provinces, you need to calculate the individual's total federal income tax and total provincial income tax. Then sum these amounts to arrive at the annual income tax.

What You Already Know

Step 1:

The employee's gross taxable earnings are $97,250. From the tax tables, you also know the federal and provincial income tax brackets and corresponding tax rates.

How You Will Get There

Step 2:

Calculate the federal income tax. This amount is the same in all three provinces and needs to be calculated only once. Looking at the federal tax table, you see that this wage earner falls into the first four tax brackets, which requires the sum of the income tax calculations for each bracket.

Step 3:

Calculate the provincial income tax. Using the provincial tax table, the income spans all four of Ontario's tax brackets. In New Brunswick, the individual falls into the first four tax brackets. In Alberta, the individual spans both of Alberta's tax brackets. In all three provinces, the total provincial income is the sum of the income tax calculations for each bracket.

Step 4:

Calculate total annual income taxes using Formula 4.2.

Perform

Step 2:

\[\begin{aligned}

&(\$ 11,038-\$ 0) \times 0=\$ 0.00\\

&(\$ 43,561-\$ 11,038) \times 0.15=\$ 4,878.45\\

&(\$ 87,123-543,561) \times 0.22=\$ 9,583.64\\

&(\$ 97,250-\$ 87,123) \times 0.26=\$ 2,633.02\\

&\text { Total federal income tax}=\$ 0.00+54,878.45+59,583.64+\$ 2,633.02=\$ 17,095.11

\end{aligned} \nonumber \]

Step 3:

Ontario

\[\begin{aligned}

&(59,574-50) \times 0=\$ 0.00\\

&(539,723-59,574) \times 0.0505=\$ 1,522.52\\

&(579,448-\$ 39,723) \times 0.0915=\$ 3,634.84\\

&(597,250-579,448) \times 0.1116=\$ 1,986.70\\&\text{Total Ontario income tax}=\$ 0.00+\$ 1,522.52$ $+\$ 3,634.84+\$ 1,986.70=\$ 7,144.06 \end{aligned} \nonumber \]

New Brunswick

\[\begin{align*} (59,388-50) \times 0 &= \$ 0.00\\ (\$ 38,954-\$ 9,388) \times 0.091 &= \$ 2,690.51\\ (\$ 77,908-\$ 38,954) \times 0.121 &= \$ 4,713.43\\ (\$ 97,250-\$ 77,908) \times 0.124 &= \$ 2,398.41\\ \text{Total New Brunswick income tax} &= \$ 0.00+\$ 2,690.51+54,713.43+52,398.41=\$ 9,802.35 \end{align*}\nonumber \]

Alberta

\[\begin{align*} (\$ 17,593-\$ 0) \times 0 &= \$ 0.00\\ (597,250-517,593) \times 0.10 &= \$ 7,965.70\\ \text{Total New Alberta income tax} &= \$0.00 + \$7,965.70 = \$7,965.70 \end{align*}\nonumber \]

Step 4:

\(\text { Total income tax if living in Ontario }=\$ 17,095.11+\$ 7,144.06=\$ 24,239.17\)

\(\text { Total income tax if living in New Brunswick }=\$ 17,095.11+\$ 9,802.35=\$ 26,897.46\)

\(\text { Total income tax if living in Alberta }=\$ 17,095.11+\$ 7,965.70=\$ 25,060.81\)

For an individual earning $97,250 in taxable gross income, the person will pay $24,239.17 in total income tax if living in Ontario, $26,897.46 total income tax if living in New Brunswick, and $25,060.81 if living in Alberta.