14.4: Debt Retirement and Amortization

- Page ID

- 22155

Issuing, buying, and selling bonds results in financial obligations and accounting responsibilities. For instance, your firm is about to issue marketable bonds to finance a major venture in the near future. These bonds require a sinking fund provision to ensure investor confidence. However, the company first needs to foresee its financial obligations if it issues the bonds. How much interest will the company need to pay out to its bondholders annually? What annual sum will it deposit into the sinking fund to satisfy the provision? How does the liability side of the company’s balance sheet reflect the fund’s provisions? All these questions need to be answered so that you can make an informed decision.

Meanwhile, the finance department reports that your company invested in marketable bonds purchased at a discount. This means your company will benefit from the future bond interest payments and also realize the bond's redemption price upon maturity. Your firm's accounting records must show capital gains being realized over the years, in the form of the difference between the face value and the discounted amount at which the bonds were purchased.

As you can see, the decision to issue or invest in a bond has many financial and tax implications that a company or an individual investor must address. This section explores the financial obligations associated with retiring bond debt and accurate recording of the debt. Also examined is the accounting for premiums and discounts, both of which have tax implications for bondholders and issuers.

Debt Retirement

When an organization issues a bond, the three primary financial implications involve the bond's interest payments, the sinking fund payments, and the balance sheet liability tied to the bond.

- Annual Bond Interest Payments. As discussed earlier in this chapter, most bonds compound semi-annually with semi-annual interest payments, thus \(CY=PY\). Because companies manage their books by their fiscal year, they are more interested in the annual total payment commitment than in the amount of each payment, \(PMT_{BOND}\). Therefore, the annual total payment commitment is represented by \[\text{Annual Bond Interest Payment} = PMT _{ BOND } \times PY\nonumber \]Substituting Formula 14.2 in place of \(PMT_{BOND}\):\[\text { Annual Bond Interest Payment = Face Value } \times \dfrac{CPN}{CY} \times PY\nonumber \]Since \(CY=PY\), simplifying the above formula produces the most direct method of arriving at the annual payment amount: \[\text { Annual Bond Interest Payment = Face Value } \times CPN \nonumber \]

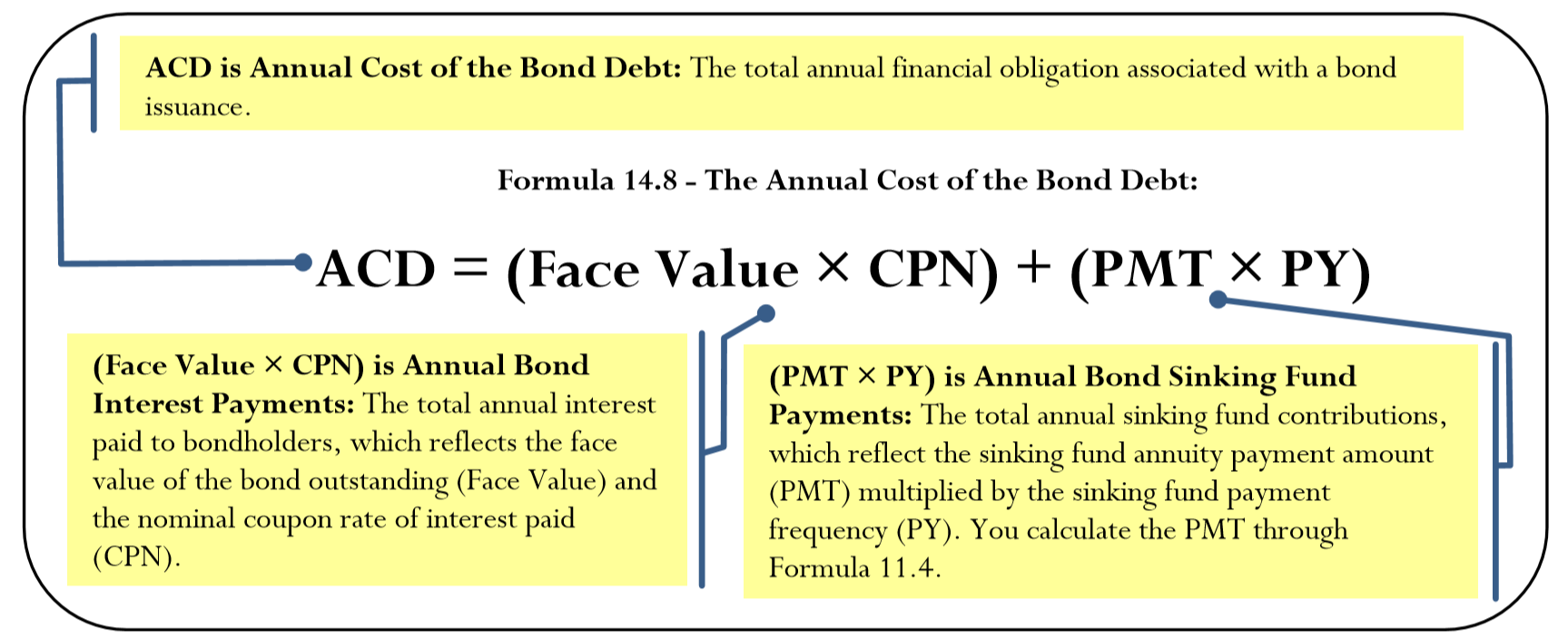

- Annual Bond Sinking Fund Payments. Sinking fund payments are most commonly set up to match the timing of the bond's interest payments. Hence, these payments are semi-annual. Again, the focus is on the annual sinking fund obligation, which you calculate by multiplying the sinking fund payment by the payment frequency, or \(PMT \times PY\). The total of the annual bond interest payments and the annual sinking fund payments is referred to as the annual cost of the bond debt or the periodic cost of the bond debt.

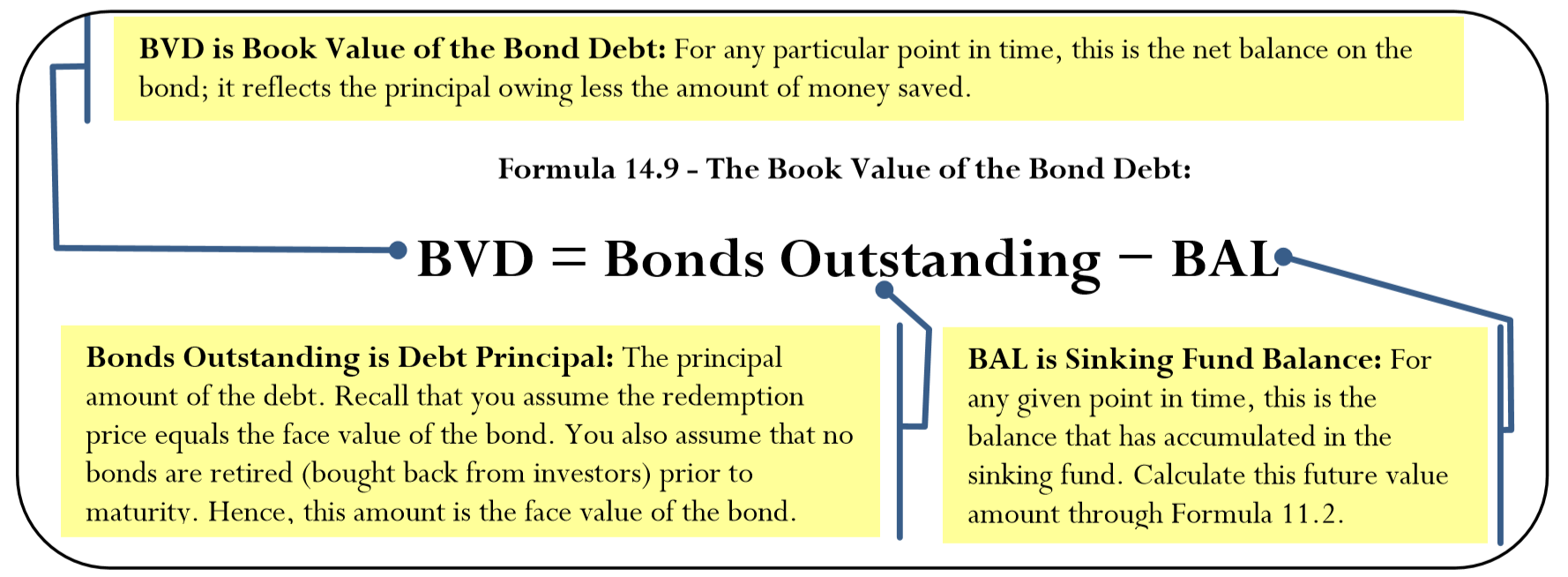

- Balance Sheet Liability. The bond represents a debt for the issuing organization. Through the sinking fund, the company saves up money to extinguish that debt. The amount of debt that is outstanding is the difference between the money owing and the money saved at any given point in time. Thus, the book value of the bond debt represents the difference between the principal amount owing on the bond and the accumulated balance in the sinking fund at any point in time. For example, if the company issued $10 million in bonds and has accumulated $1 million in its sinking fund, the book value of the debt is $9 million. This would be the balance owing if the company used the sinking fund to retire a portion of the bond debt at face value.

The Formula

To calculate the annual cost of the bond debt, you combine both the annual bond interest payments and annual bond sinking fund payments into a single formula.

Formula 14.9 lets you calculate the book value of the bond debt.

How It Works

Follow these steps to calculate the annual cost of the bond debt:

Step 1: Identify the face value of the bond and the coupon rate.

Step 2: If the sinking fund payment (\(PMT\)) and payment frequency (\(PY\)) are known, skip to step 4. Otherwise, draw a timeline for the sinking fund and identify known variables.

Step 3: Calculate the sinking fund payment using Formula 11.4.

Step 4: Calculate the annual cost of the bond debt using Formula 14.8.

Follow these steps to calculate the book value of the bond debt:

Step 1: Identify the face value of the bond.

Step 2: If the balance in the sinking fund (\(BAL\)) is known, skip to step 5. Otherwise, draw a timeline for the sinking fund and identify known variables.

Step 3: Calculate the sinking fund payment using Formula 11.4.

Step 4: Calculate the future value of the sinking fund at the point of interest using Formula 11.2. This is the sinking fund balance, or \(BAL\).

Step 5: Calculate the book value of the bond debt using Formula 14.9.

Suppose a company decides not to wait until maturity and retires some of its bond debt early on an interest payment date. What happens to the \(BVD\) if the debt is retired when:

- the market rate equals the coupon rate?

- the market rate is higher than the coupon rate?

- the market rate is lower than the coupon rate?

(Hint: Think about what happens to the market price of the bond.)

- Answer

-

- The \(BVD\) is unchanged. If the two rates are the same, then the bonds sell at par value. Money is transferred dollar for dollar from the sinking fund to directly reduce the bond debt.

- The \(BVD\) decreases. If the market rate is higher, the bonds sell at a discount. The company acquires more bonds at the lower bond price, reducing the number of outstanding bonds.

- The \(BVD\) increases. If the market rate is lower, the bonds sell at a premium. The company acquires fewer bonds at the higher bond price, leaving a larger number of outstanding bonds than by redeeming at par.

The Bank of Montreal issued a $10,000,000 face value bond carrying a 5.1% coupon with 30 years until maturity. The bond has a matching sinking fund provision for which monies are invested at 4.5%. Calculate the annual cost of the bond debt. Assume all compounding and payments are semi-annual.

Solution

You need to calculate the annual cost of the bond debt (\(ACD\)).

What You Already Know

Step 1:

Face Value = $10,000,000, \(CPN\) = 5.1%

Step 2:

The timeline for the sinking fund appears below.

\(FV_{ORD}\) = $10,000,000, \(IY\) = 4.5%, \(CY\) = 2, \(PY\) = 2, Years = 30, \(PV\) = $0

How You Will Get There

Step 3:

Solve for the ordinary sinking fund annuity payment (\(PMT\)) using Formulas 9.1, 11.1, and 11.2 (rearranging for \(PMT\)).

Step 4:

Calculate the annual cost of the bond debt using Formula 14.8.

Perform

Step 3:

\(i=4.5 \% / 2=2.25 \% ; N=2 \times 30=60\) payments

\[\$ 10,000,000=PMT\left[\dfrac{\left[(1+0.0225)^{\frac{2}{2}}\right]^{60}-1}{(1+0.0225)^{\frac{2}{2}}-1}\right] \nonumber \]

\[PMT=\dfrac{\$ 10,000,000}{\left[\dfrac{\left[(1+0.0225)^{\frac{2}{2}}\right]^{60}-1}{(1+0.0225)^{\frac{2}{2}}-1}\right]}=\$ 80,353.27 \nonumber \]

Step 4:

\[\begin{aligned} ACD &=(\$ 10,000,000 \times 0.051)+(\$ 80,353.27 \times 2) \\ &=\$ 510,000+\$ 160,706.54\\&=\$ 670,706.54 \end{aligned} \nonumber \]

Calculator Instructions

| Mode | N | I/Y | PV |

|---|---|---|---|

| END | 60 | 4.5 | 0 |

| PMT | FV | P/Y | C/Y |

|---|---|---|---|

| Answer: -80,353.27482 | 10000000 | 2 | 2 |

Each year, the Bank of Montreal pays $510,000 in interest to its bondholders. Additionally, it deposits $160,706.54 to its sinking fund. Thus, the annual cost of the bond debt is $670,706.54 every year for the next 30 years.

Using Example \(\PageIndex{1}\), calculate the book value of the bond debt after 10 years.

Solution

You must calculate the book value of the bond debt (\(BVD\)) after 10 years.

What You Already Know

Step 1:

Face Value = $10,000,000

Steps 2 and 3:

The sinking fund balance is unknown. From the previous example, the sinking fund payment is \(PMT\) = $80,353.27. The timeline for calculating the sinking fund after 10 years appears below.

\(FV_{ORD}\) = $10,000,000, \(IY\) = 4.5%, \(CY\) = 2, Years = 10, \(PMT\) = $80,353.27, \(PY\) = 2, \(PV\) = $0

How You Will Get There

Step 4:

Solve for future value of the ordinary sinking fund, or \(FV_{ORD}\), after 10 years using Formulas 9.1, 11.1, and 11.2.

Step 5:

Calculate the book value of the bond debt using Formula 14.9.

Perform

Step 4:

\(i=4.5 \% / 2=2.25 \% ; N=2 \times 10=20 \) payments made over 10 years

\[FV_{ORD }=\$ 80,353.27\left[\dfrac{\left[(1+0.0225)^{\frac{2}{2}}\right]^{20}-1}{(1+0.0225)^{\frac{2}{2}}-1}\right]=\$ 2,001,722.10 \nonumber \]

Step 5:

\[BVD=\$ 10,000,000-\$ 2,001,722.10=\$ 7,998,277.90 \nonumber \]

Calculator Instructions

| Mode | N | I/Y | PV | PMT |

|---|---|---|---|---|

| END | 20 | 4.5 | 0 | -80353.27 |

| FV | P/Y | C/Y |

|---|---|---|

| Answer: 2,001,722.095 | 2 | 2 |

After 10 years, the Bank of Montreal will accumulate $2,001,722.10 in its sinking fund. With a $10,000,000 debt, the book value of the bond debt remaining equals $7,998,277.90.

Amortization of Bond Premiums and Accrual of Bond Discounts

When a bond sells for a price different from its face value, the bond premium or bond discount has accounting implications. Take a look at each scenario.

Bond Premium

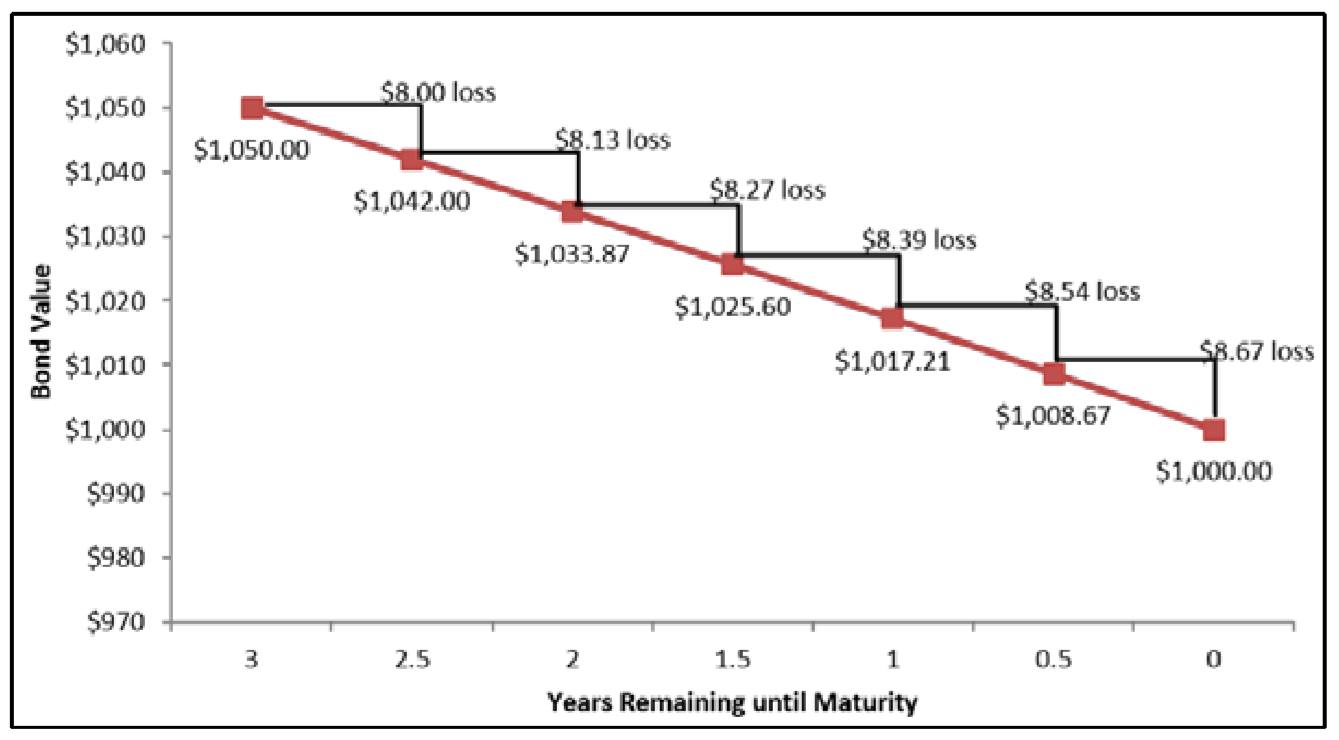

Figure \(\PageIndex{3}\)

In these situations, the investor pays more for the bond, say $1,050 for a $1,000 bond. If the investor holds onto the bond until maturity, only the redemption price of $1,000 is returned. The bond premium of $50 represents a capital loss for the investor. A capital loss is the amount by which the current value of an asset falls short of the original purchase price. Commonly accepted practices allow the investor to amortize the $50 capital loss over the period of time that the bond is held and not just in the period during which the capital loss actually occurs (at maturity). The figure illustrates the amortization of a capital loss assuming three years remain until maturity on a $1,000 bond carrying a 5% coupon purchased when the market rate was 3.23775%. Note that the total capital loss of $50 is spread throughout the entire three-year time frame.

Bond Discount

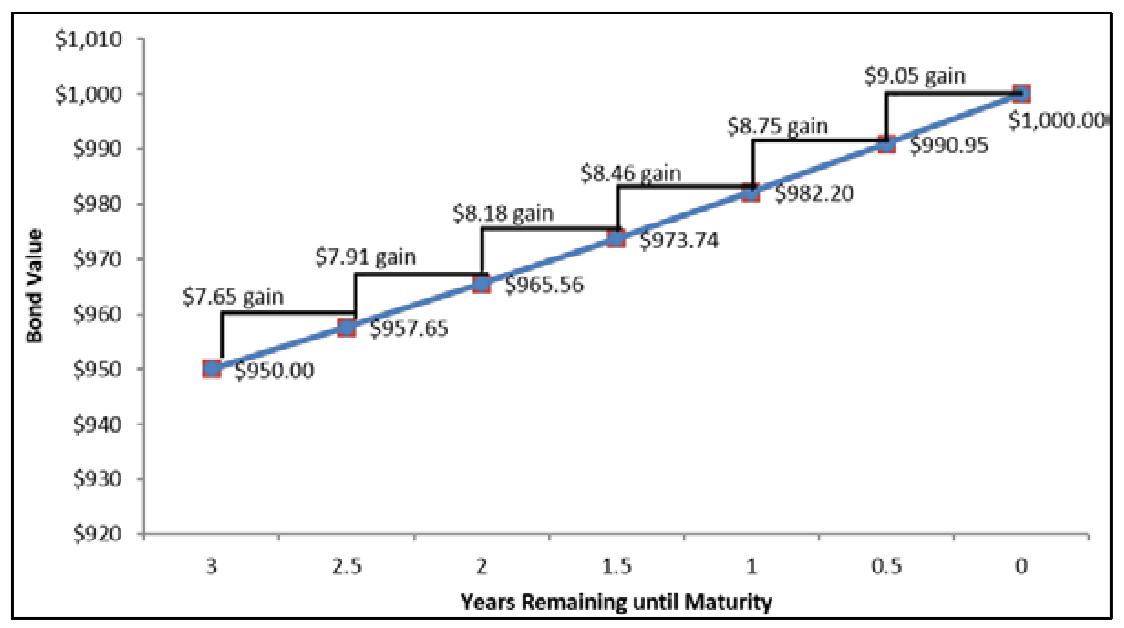

Figure \(\PageIndex{4}\)

In these situations, the investor pays less for the bond, say $950 for a $1,000 bond. If the investor holds onto the bond until maturity, the investor receives the full redemption price of $1,000. The bond discount of $50 represents a capital gain for the investor. A capital gain is the amount by which the current value of an asset exceeds the original purchase price. Commonly accepted practice allows the investor to accrue the $50 capital gain over the period of time that the bond is held and not just in the period during which the capital gain actually occurs (at maturity). For example, assuming three years remain until maturity on a $1,000 bond carrying a 5% coupon purchased when the market rate was 6.8729%,the figure illustrates the accrual of a capital gain of $50. Note that the total gain is spread throughout the three-year time frame.

In either situation, the gain or loss has tax implications for the investor. These amounts appear on tax forms and either raise the amount of taxes paid by the investor (for gains) or lower the amount of taxes (for losses). As well, for companies these amounts appear on financial statements.

The Formula

To allow the investor to understand these capital gains or losses, you must develop either an amortization table for premiums or an accrual table for discounts. The table here illustrates the standard format of either table. You should note the following in the table:

| Payment Interval Number (at end) | Bond Interest Payment Amount (\(PMT_{BOND}\)) | Interest at Yield Rate (PMT) | Amortized Premium or Discount Accrued | Bond Value (Cash Price) |

|---|---|---|---|---|

| 0 | N/A | N/A | N/A | Purchase Price |

| 1 | Formula 14.2 | Formula 10.1 |

Premium:\(PMT_{BOND}-PMT\) Discount:\(PMT-PMT_{BOND}\) |

Premium: Previous Value − Premium Discount: Previous Value + Discount |

| ... | ||||

| Last Payment | ||||

| Total | Total Interest Received | Net Income Realized |

Premium: Capital Loss Discount: Capital Gain |

N/A |

- A suitable header of discount or premium is used for the fourth column

- In the last two columns, the method of calculation depends on whether the table is for a premium or discount.

How It Works

Follow these steps to develop a premium amortization table or discount accrual table:

Step 1: Draw a timeline for the bond. Identify all of the time value of money variables for the bond (\(N, IY, FV, PMT_{BOND}, PY, CY\)). Use Formulas 14.2 and 14.3 as needed to solve for any unknowns.

Step 2: Set up a table, using the appropriate headers depending on the bond discount or premium. The number of payment intervals is the \(N\) identified in step 1.

Step 3: Fill in the purchase price of the bond under the “Bond Value” column for payment 0.

Step 4: Fill in the bond annuity payment, or \(PMT_{BOND}\), for every payment in the “Bond Interest Payment Amount” column.

Step 5: Based on the market yield at which the bond was purchased, calculate the interest portion of the current bond payment based on the prior “Bond Value” using Formula 10.1. Round the number to two decimals for the table but retain all decimals for future calculations.

Step 6: Calculate the amortized premium or discount accrued using one the two techniques shown below. Either way, round the result to two decimals for the table but retain all decimals for future calculations.

- For a bond premium, calculate the amortized premium of the current bond payment by taking the second column and subtracting the third column, or \(PMT_{BOND} − PMT\).

- For a bond discount, calculate the discount accrued by taking the third column and subtracting the second column, or \(PMT − PMT_{BOND}\).

Step 7: Calculate the new bond value for the current payment using one of the two techniques shown below. Either way, round the result to two decimals for the table but retain all decimals for future calculations.

- For a bond premium, calculate the new bond value by taking the previous unrounded “Bond Value” on the line above and subtracting the unrounded amortized amount from step 6.

- For a bond discount, add the two numbers to calculate the new bond value.

Step 8: Repeat steps 5 through 7 for each payment interval until you reach bond maturity.

Step 9: Since all numbers are rounded to two decimals throughout the table, check the table for the "missing penny” using the same method as for amortization tables.

- The previous bond values plus or minus the amortized or discount amount must equal the new bond value.

- The amortized or discount amount plus the interest portion must equal the bond payment amount. Note that on the final line of the table the balance should equal the face value. If necessary, adjust the penny to exactly match the face value.

Step 10: Sum the bond interest payments received. This is the total interest payments received by the investor.

Step 11: Sum the bond interest earned at the yield rate.

Step 12: Sum the amortized premium or discount accrued to arrive at the total capital loss or capital gain, respectively. You calculate a nominal net income by taking the total bond interest and either subtracting the total capital loss or adding the total capital gain.

Important Notes

This section introduces how to spread the capital gain or capital loss on a bond across different time periods. Therefore, it sticks to premium amortization tables and discount accrual tables where the bond is purchased on its interest payment date. If the bond is purchased on some other date, this adds complications that are better left for more in-depth texts.

When posted market rates were 4%, Baseline Industries acquired a $10,000 bond carrying a 6% coupon rate with three years remaining until maturity. Develop a complete bond premium amortization table. Assume that all payments and interest are semi-annual.

Solution

You need to construct a complete bond premium amortization table.

What You Already Know

Step 1:

The timeline of the bond purchase appears below.

Coupon Interest Payment: \(CPN\) = 6%, \(CY\) = 2, Face Value = $10,000

Bond: \(FV\) = $10,000, \(IY\) = 4%, \(CY\) = 2, \(PMT_{BOND}\) = Formula 14.2, \(PY\) = 2, Years Remaining = 3

How You Will Get There

Step 1 (continued):

Apply Formula 14.2 to determine the periodic bond interest payment. Then apply Formulas 9.1, 11.1, and 14.3 to determine the price of the bond on its interest payment date.

Step 2:

Set up the bond premium amortization table.

Steps 3 and 4:

Fill in the purchase price and the bond payment amount column.

Steps 5 to 8:

Use Formula 10.1 and for each line calculate the last two columns.

Step 9:

Check for the "missing penny."

Steps 10 to 12:

Total up the bond payments, interest payments, and amortized amounts.

Perform

Step 1:

\[PMT_{BOND}=\$ 10,000 \times \dfrac{0.06}{2}=\$ 300 \nonumber \]

\(i=4 \% / 2=2 \% ; N=2 \times 3=6\) payments

\[\text { Date Price }=\dfrac{\$ 10,000}{(1+0.02)^{6}}+\$ 300\left[\dfrac{1-\left[\dfrac{1}{1+0.02}\right]^{6}}{0.02}\right]=\$ 10,560.14 \nonumber \]

Step 2 to 8 (with some calculations) are detailed in the table below:

| Payment Interval Number (at end) | Bond Interest Payment Amount (\(PMT_{BOND}\)) | Interest at Yield Rate (PMT) | Amortized Premium | Bond Value (Cash Price) |

|---|---|---|---|---|

| 0 | $10,560.14 | |||

| 1 | $300 | (1) $211.20 | (2) $88.80 | (3) $10,471.34 |

| 2 | $300 | $209.43 | $90.57 | $10,380.77 |

| 3 | $300 | $207.61 | $92.38 | $10,288.39 |

| 4 | $300 | $205.77 | $94.23 | $10,194.15 |

| 5 | $300 | $203.88 | $96.12 | $10,098.04 |

| 6 | $300 | $201.96 | $98.04 | $10,000.00 |

| Total |

(1) $10,560.14 × 0.02 = $211.2028

(2) $300 − $211.2028 = $88.7972

(3) $10,560.14 − $88.7972 = $10,471.3428

Steps 9 to 12:

Adjust for the "missing pennies" (noted in red) and total the bond payment amount, interest at yield rate, and amortized premiums.

| Payment Interval Number (at end) | Bond Interest Payment Amount (\(PMT_{BOND}\)) | Interest at Yield Rate (PMT) | Amortized Premium | Bond Value (Cash Price) |

|---|---|---|---|---|

| 0 | $10,560.14 | |||

| 1 | $300 | (1) $211.20 | (2) $88.80 | (3) $10,471.34 |

| 2 | $300 | $209.43 | $90.57 | $10,380.77 |

| 3 | $300 | $207.61 | $92.38 | $10,288.39 |

| 4 | $300 | $205.77 | $94.23 | $10,194.15 |

| 5 | $300 | $203.88 | $96.12 | $10,098.04 |

| 6 | $300 | $201.96 | $98.04 | $10,000.00 |

| Total | $1,800 | $1,239.86 | $560.14 |

Calculator Instructions

| Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| END | 6 | 4 | Answer: -10,560.14309 | 300 | 10000 | 2 | 2 |

By purchasing the bond at a premium price of $10,560.14 and holding it until maturity, when it has a redemption price of $10,000, Baseline Industries takes a $560.14 capital loss. It receives $1,800 in bond payments, loses $560.14, and realizes nominal net income of $1,239.86.

Recalculate Example \(\PageIndex{3}\) by changing the market rate to 8%. Construct a bond discount accrual table.

Solution

You need to construct a complete bond discount accrual table.

What You Already Know

Step 1:

The timeline for the bond purchase appears below.

Coupon Interest Payment: \(CPN\) = 6%, \(CY\) = 2, Face Value = $10,000

Bond: \(FV\) = $10,000, \(IY\) = 8%, \(CY\) = 2, \(PMT_{BOND}\) = Formula 14.2, \(PY\) = 2, Years Remaining = 3

How You Will Get There

Step 1 (continued):

Apply Formula 14.2 to determine the periodic bond interest payment. Then apply Formulas 9.1, 11.1, and 14.3 to determine the price of the bond on its interest payment date.

Step 2:

Set up the bond discount accrual table.

Steps 3 and 4:

Fill in the purchase price and the bond payment amount column.

Steps 5 to 8:

Use Formula 10.1 and for each line calculate the last two columns

Step 9:

Check for the "missing penny."

Steps 10 to 12:

Total up the bond payments, interest payments, and accrued amounts.

Perform

Step 1:

\[PMT_{BOND}=\$ 10,000 \times \dfrac{0.06}{2}=\$ 300 \nonumber \]

\(i=8 \% / 2=4 \% ; N=2 \times 3=6 \) payments

\[\text { Date Price }=\dfrac{\$ 10,000}{(1+0.04)^{6}}+\$ 300\left[\dfrac{1-\left[\dfrac{1}{1+0.04}\right]^{6}}{0.04}\right]=\$ 9,475.79 \nonumber \]

Step 2 to 8 (with some calculations) are detailed in the table below:

| Payment Interval Number (at end) | Bond Interest Payment Amount (\(PMT_{BOND}\)) | Interest at Yield Rate (PMT) | Amortized Premium | Bond Value (Cash Price) |

|---|---|---|---|---|

| 0 | $9,475.79 | |||

| 1 | $300 | (1) $379.03 | (2) $79.03 | (3) $9,554.82 |

| 2 | $300 | $382.19 | $82.19 | $9,637.01 |

| 3 | $300 | $385.48 | $85.48 | $9,722.50 |

| 4 | $300 | $388.90 | $88.90 | $9,811.39 |

| 5 | $300 | $392.46 | $92.46 | $9,903.85 |

| 6 | $300 | $396.15 | $96.15 | $10,000.00 |

| Total |

(1) $9,475.79 × 0.04 = $379.0316

(2) $379.0316 − $300 = $79.0316

(3) $9,475.79 + $79.0316 = $9,554.8216

Steps 9 to 12:

Adjust for the "missing pennies" (noted in red) and total the bond payment amount, interest at yield rate, and discounts accrued.

| Payment Interval Number (at end) | Bond Interest Payment Amount (\(PMT_{BOND}\)) | Interest at Yield Rate (PMT) | Amortized Premium | Bond Value (Cash Price) |

|---|---|---|---|---|

| 0 | $9,475.79 | |||

| 1 | $300 | (1) $379.03 | (2) $79.03 | (3) $9,554.82 |

| 2 | $300 | $382.19 | $82.19 | $9,637.01 |

| 3 | $300 | $385.48 | $85.48 | $9,722.50 |

| 4 | $300 | $388.90 | $88.90 | $9,811.39 |

| 5 | $300 | $392.46 | $92.46 | $9,903.85 |

| 6 | $300 | $396.15 | $96.15 | $10,000.00 |

| Total | $1,800 | $2,324.21 | $524.21 |

Calculator Instructions

| Mode | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| END | 6 | 8 | Answer: -9,475.786314 | 300 | 10000 | 2 | 2 |

By purchasing the bond at a discounted price of $9,475.79 and holding it until maturity, when it has a redemption price of $10,000, Baseline Industries earns a $524.21 capital gain. It receives $1,800 in bond payments, gains $524.21, and realizes nominal net income of $2,324.21.