14.S: Summary

- Page ID

- 22156

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Key Concepts

14.1: Determining the Value of a Bond (What Does It Sell for?)

- Bond definition, characteristics, and key terminology

- Calculating a marketable bond price when the selling date is the interest payment date

- Calculating premiums and discounts

- Calculating a marketable bond price when the selling date is a noninterest payment date

14.2: Calculating a Bond’s Yield (Know When to Hold ’em, Know When to Fold ’em)

- Calculating the yield on the bond to maturity

- Calculating the yield realized by an investor if a bond is purchased and sold before maturity

14.3: Sinking Fund Schedules (You Need to Show Responsibility)

- Sinking funds and their purposes

- How to construct complete ordinary sinking fund schedules

- How to construct partial ordinary sinking fund schedules

- Adapting any ordinary sinking fund into an annuity fund due schedule

14.4: Debt Retirement and Amortization (Balancing the Books)

- The financial implications of retiring bond debt

- How to amortize a bond premium or accrue a bond discount

The Language of Business Mathematics

- annual cost of the bond debt

- The annual total of the bond interest payments and the bond sinking fund payments.

- bond

- A debt that is secured by a specific corporate asset and that establishes the issuer’s responsibility toward a creditor for paying interest at regular intervals and repaying the principal at a fixed later date.

- bond accrued interest

- The amount of interest that the bond has earned but has not yet paid out since the previous interest payment date.

- bond cash price

- Also known as the purchase price or flat price, this is the amount of money an investor must directly pay out to acquire the bond. It represents the total of the market price and the accrued interest.

- bond coupon rate

- Also known as the bond rate or nominal rate, this is the nominal interest rate paid on the face value of the bond.

- bond discount

- The amount by which a bond's selling price falls short of its face value.

- bond face value

- Also called the par value or denomination of the bond, this is the principal amount of the debt that the investor lent to the bond-issuing corporation.

- bond issue date

- The date that a bond is issued and available for purchase by creditors

- bond market price

- Also known as the quoted price, this is the actual value of the bond excluding any accrued interest.

- bond market rate

- This is the prevailing nominal rate of interest in the open bond market.

- bond maturity date

- Also known as the redemption date or due date, this is the day upon which the redemption price will be paid to the bondholder (along with the final interest payment), thereby extinguishing the debt.

- bond premium

- The amount by which a bond's selling price exceeds its face value.

- bond redemption price

- Also called the redemption value or maturity value, this is the amount the bond issuer will pay to the bondholder upon maturity of the bond.

- bond selling date

- This is the date that a bond is actively traded and sold to another investor through the bond markets.

- book value of the bond debt

- The difference between the principal amount owing on the bond and the accumulated balance in the sinking fund at any point in time.

- capital gain

- The amount by which the current value of an asset exceeds the original purchase price.

- capital loss

- The amount by which the current value of an asset falls short of the original purchase price.

- debenture

- A debt that is not secured by a specific corporate asset and that establishes the issuer’s responsibility toward a creditor for paying interest at regular intervals and repaying the principal at a fixed later date.

- sinking fund

- A special account into which an investor, whether an individual or a business, makes annuity payments such that sufficient funds will be on hand by a specified date to meet a future savings goal or debt obligation.

- sinking fund schedule

- A table that shows the sinking fund contribution, interest earned, and the accumulated balance for every payment in the annuity.

- yield to maturity

- A bond's overall rate of return when purchased at a market price and held until maturity. It includes both the semi-annual interest that the bondholders earn on their investment along with the gain or loss resulting from the difference between the market price and the redemption price.

The Formulas You Need to Know

Symbols Used

\(ACD\) = Annual cost of the bond debt

\(AI\) = Accrued interest

\(BAL\) = Principal balance

\(BVD\) = Book value of the bond debt

Cash Price = Price paid for a bond including the market price and accrued interest

\(CPN\) = Nominal bond coupon rate of interest

\(CY\) = Compounding per year or compounding frequency

Date Price = Price of the bond on the interest payment date preceding the sale date

Discount = Bond discount amount

Face Value = Bond face value

\(i\) = Periodic interest rate

\(INT_{SFDUE}\) = Interest portion of any single annuity due sinking fund payment

\(N\) = Number of annuity payments

\(PMT\) = Annuity payment amount

\(PMT_{BOND}\) = The bond's annuity payment as determined by the coupon rate

Premium = Bond premium amount

\(PRI\) = Market price

\(t\) = Time ratio (using the actual number of days)

Formulas Introduced

Formula 14.1 The Cash Price for Any Bond: \(\text { Cash Price }=PRI+AI\)

Formula 14.2 Bond Coupon Annuity Payment Amount: \(PMT_{BOND}=\text { Face Value } \times \dfrac{CPN}{CY}\)

Formula 14.3 Bond Price on an Interest Payment Date: \(\text { Date Price }=\dfrac{FV}{(1+i)^{N}}+PMT_{BOND}\left[\dfrac{1-\left[\dfrac{1}{1+i}\right]^{N}}{i}\right]\)

Formula 14.4 Bond Premium or Discount: \(\text { Premium or Discount }=\text { PRI - Face Value }\)

Formula 14.5 Bond Cash Price on a Noninterest Payment Date: \(\text { Cash Price }=(\text { Date Price })(1+i)^{t} \)

Formula 14.6 Accrued Interest on a Noninterest Payment Date: \(Al=PMT_{BOND} \times t\)

Formula 14.7 Interest Portion of a Sinking Fund Single Payment Due: \(\text { INT_{SFDUE } }=(BAL+PMT) \times\left((1+i)^{\frac{CY}{PX}}-1\right)\)

Formula 14.8 The Annual Cost of the Bond Debt: \(ACD=(\text { Face Value } \times CPN)+(PMT \times PY)\)

Formula 14.9 The Book Value of the Bond Debt: \(BVD=\text { Bonds Outstanding }-BAL\)

Technology

Calculator

The DATE function was used in this chapter. See the end of Chapter 8 for a full discussion of this function.

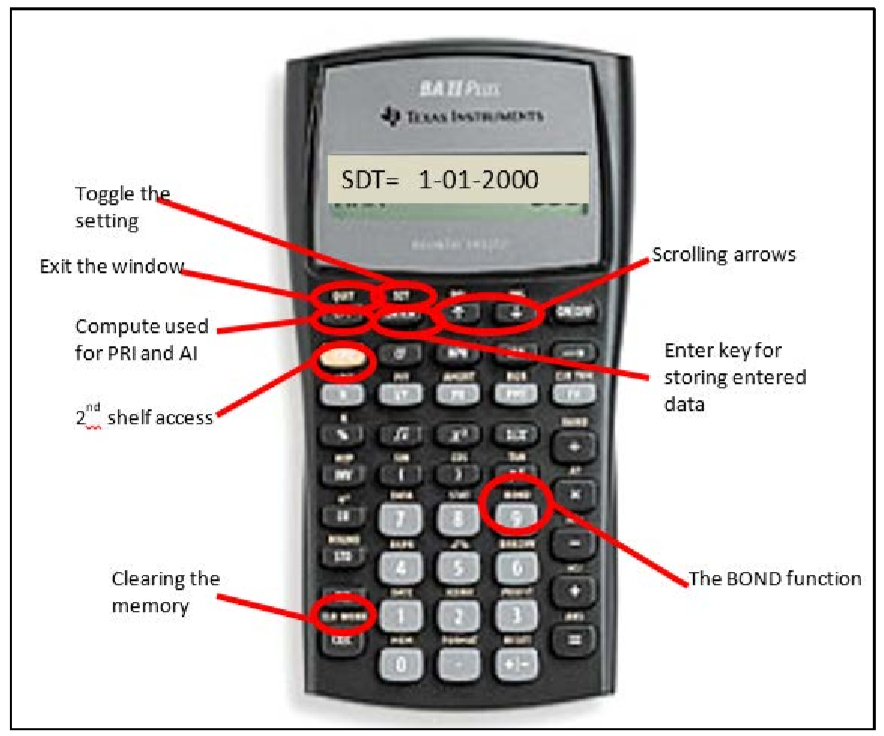

The Bond Function

- The BOND function is located on the second shelf above the number 9 key and accessed by pressing 2nd BOND.

- Scroll through using the ↓ and ↑ arrows.

- There are nine lines in the function. The first seven lines are considered the data entry lines, while the last two are the output lines.

- Upon opening the window, you should use the 2nd CLR Work function to erase previously entered data. The input lines are as follows:

- SDT is the selling date. Enter it in the standard date format of MM.DDYY and press the ENTER key to store the information.

- CPN is the nominal coupon rate. It is formatted as a percentage but without the percent sign, so you key in 5.5% as 5.5. You must press the ENTER key to store the information.

- RDT is the redemption date or maturity date. Enter it in the standard date format and press ENTER to store the information.

- RV is the redemption value or redemption price expressed as a percentage of the face value. Since the redemption price equals the face value, use the default setting of 100.

- ACT/360 is a toggle that you change by pressing 2nd SET. ACT counts the actual number of days in the transaction, while 360 treats every month as having 30 days. In Canada, ACT is the standard.

- 2/Y or 1/Y is a toggle that you change by pressing 2nd SET. 2/Y indicates a semi-annual compound for both the market rate and coupon rate, while 1/Y indicates an annual compound.

- YLD is the nominal market rate for bonds at the time of sale. It follows the same format as the CPN. Press the ENTER key to store the information. The output lines are as follows:

- PRI is the market price of the bond. Press the CPT button to calculate for this solution. The output is a percentage of the redemption price (which is the same as the face value).

- AI is the accrued interest of the bond. It is automatically calculated when you press the CPT button in the PRI line. The output is a percentage of the redemption price.

Sinking Funds Using AMORT

- The AMORT function was used in this chapter. See the end of Chapter 13 for a full discussion of this function. Specific sinking fund comments and adaptations are listed below.

- Ordinary sinking funds: The principal grows instead of declining.

- With respect to the cash flow sign convention, the PV (if not zero) and PMT are negative, since money is being invested into the account. The FV is a positive number since it can be withdrawn in the future.

- The BAL and INT outputs are accurate and true to definition. The PRN output is also accurate, but its definition is changed to represent the total of the annuity payments made and the interest earned.

- Sinking funds due: You must adapt the payment number.

- P1 and P2: Always add one to the payment number(s) desired.

- BAL: It has one payment too many. To correct for this, decrease the balance by removing one payment (or with BAL on your display, press − RCL PMT =).

- INT and PRN: Both of these numbers are correct.

- Ordinary sinking funds: The principal grows instead of declining.