8.4: Application - Promissory Notes

- Last updated

- Dec 15, 2024

- Save as PDF

( \newcommand{\kernel}{\mathrm{null}\,}\)

Have you ever lent a friend or family member some money on a promise they would pay you back on a specific date? Then you are already experienced with promissory notes!

Just before class a fellow student and close friend announces that the two of you should go for coffee afterwards. He seems a little tense, but he says there is no trouble, so you contain your curiosity until you are seated in a quiet corner of your local Starbucks. Then he asks if he can borrow $5,000 from you to pursue a new entrepreneurial venture, explaining that he already tried to get the money from a bank but too much red tape was involved and the interest rate was outrageous. You have the money saved up in your account. After your friend lays out all of the details, you feel satisfied that he has a good idea. Before lending your friend the money, though, it might be worthwhile to put this down in writing just in case matters turn sour, right? And by loaning your friend the money, you would be forgoing at least the interest on your savings and feel that it is fair to charge your friend the same interest rate so that you are not hurt financially. A promissory note seems a good path to take.

This section explains the characteristics of short-term promissory notes. You will learn how to calculate the maturity value of a promissory note along with its selling price if you want to cash it in before it matures.

What Are Promissory Notes?

Promissory notes are borrowing tools that allow both companies and people to get financing from a source other than a bank. The money is borrowed from other people or companies who are willing to provide the financing. The Bills of Exchange Act defines a promissory note as "an unconditional promise in writing made by one person to another person, signed by the maker, engaging to pay, on demand or at a fixed or determinable future time, a sum certain in money to, or to the order of, a specified person or to bearer.1 Promissory notes are commonly referred to just as notes.

A promissory note is not the same as an IOU (I owe you). An IOU simply acknowledges a debt but contains no promise of repayment, no timelines, and no consequences. A promissory note includes these elements.

In the opening scenario, it is probably best to create a promissory note that clearly details your agreement and terms. This allows both of you to have peace of mind in the transaction, and in the event something goes wrong both of you have a legally binding written record of your transaction.

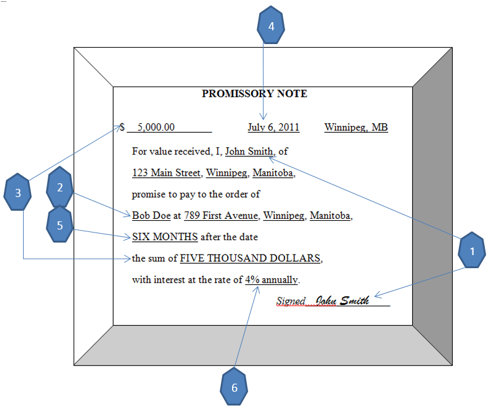

The illustration here provides an example of a promissory note. Observe the following characteristics:

- Borrower. This is the individual who is borrowing the money, sometimes known as the maker, promisor, or payor. It is best to provide details such as the name and address of the borrower to clearly establish an identity.

- Lender. This is the individual who is loaning the money (and should be repaid), sometimes known as the payee or issuer. As with the borrower, detailed name and address information clearly establish the identity of this person.

- Face Value. This is the borrowed principal. It appears numerically and in writing to prevent it from being altered. In simple interest calculations, this is the P.

- Issue Date (Start Date). This is the date on which the promissory note is issued and forms the starting date of the transaction.

- Term. This is the length of time for which the face value is borrowed from the lender. In simple interest calculations, this is the basis for the time period (t).

- Interest Rate. This is the percentage interest being charged along with the respective time frame for the interest (monthly, annually, etc.). In simple interest calculations, this is the rate (r).

Note in the illustration that the lender has decided to not have any additional consequence for failing to pay back the $5,000 after the six months. As written, any late payment continues to be charged 4% annual interest only.

Promissory notes are issued outside the normal banking system, so it is up to the lender to determine the interest rate. This results in two types of promissory notes:

- Noninterest-Bearing Notes. In these cases, the lender has decided not to charge any interest, hence making the interest rate 0%. Alternatively, the lender and borrower may decide to include an amount of interest in the face value specified on the note. For example, the lender may borrow $5,000, but the note is written for $5,100 with no interest. In the case of a noninterest-bearing note, of course, no calculation of interest on the promissory note is needed to determine the amount that is due, as the face value equals the maturity value.

- Interest-Bearing Notes. In these cases, the lender has decided to charge interest on the face value. This requires you to calculate the simple interest on the face value. Therefore, the maturity value is the face value plus a simple interest amount. The method for this calculation is discussed next.

Maturity Value for Interest-Bearing Notes

Based on all of the elements included in the promissory note, the maturity date or end date of the promissory note must be determined before the borrower and lender can calculate simple interest. This is the date upon which the promissory note needs to be repaid. However, by Canadian law this is not the due date. The legal due date of a note is instead three days after the term specified, allowing the borrower time to repay the note without penalty in the event that the due date falls on a statutory holiday or weekend, when it might not be possible to make the payment. Interest is still charged during those three days, though. The three days’ grace period can be waived by the borrower by stating “no grace” on the promissory note.

The following rules are used to determine the due date:

- Specific Date or Number of Days. If the note states a specific maturity date or details the exact number of days, then the due date is three days later than the maturity date.

- Time Period in Months. If the note states a number of months, then it is due on the same date in the month in which it matures plus three days. In the illustration, the note was issued on July 6, 2011. Six months later is January 6, 2012, plus three days gives a legal due date of January 9, 2012. A special situation arises, though, if the note is issued near or at the end of a month. For example, if the note is issued instead on August 31, 2011, six months later is February 31, 2012. Since this date does not exist, the rule is to use the last day of the month in which it matures. Therefore, the note has a maturity date of February 29, 2012, and that plus three days gives a legal due date of March 3, 2012.

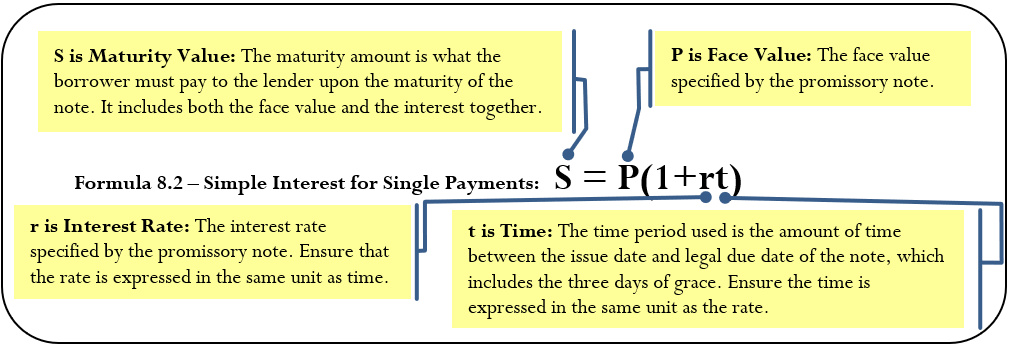

The Formula

Once you know the legal due date, calculate the time involved in the transaction using the methods discussed in Section 8.1. You calculate the maturity value using Formula 8.2 from Section 8.2, which is reproduced below and adapted for promissory notes.

How It Works

You use the same four steps to calculate the maturity value of a single payment as when calculating the maturity value of a promissory note. The only nuance requiring close attention lies in determining the time period.

Working with the previous promissory note illustration, calculate the amount that John Smith owes to Bob Doe along with the amount of interest.

Step 1: Note that this promissory note is interest-bearing because of the interest rate information provided on the note. The face value or P=$5,000. The interest rate or r=4% annually. To calculate the time, it is noted above that the legal due date of this promissory note is six months plus three days later, which is January 9, 2012. Using an appropriate date method from Section 8.1, the days between the dates equal 187 days.

Step 2: Expressing the time annually to match the annual rate, t=187/365.

Step 3: Substituting into Formula 8.2, S=$5,000(1+0.04(187/365))=$5,102.47. Therefore, John needs to repay $5,102.47 to Bob on January 9, 2012.

Step 4: The amount of interest on the note is I=$5,102.47−$5,000=$102.47.

Corey borrowed $7,500 from Miller Enterprises on March 31, 2011. An interest-bearing promissory note was created, indicating that the money was to be repaid eight months later at an interest rate of 6% annually. Calculate the maturity value of the promissory note on the legal due date.

Solution

Calculate the maturity value of the promissory note (S) upon the legal due date using the stated interest rate.

What You Already Know

Step 1:

The face value, interest rate, term, and issue date are known:

P=$7,500,r=6% per year t=8 months, Issue date = March 31, 2011

How You Will Get There

Step 1 (continued):

Calculate the legal due date by determining the end of the term and adding three days. Transform this date into the number of days.

Step 2:

While the rate is annual, the time is in days. Convert the time to an annual number.

Step 3:

Apply Formula 8.2.

Perform

Step 1 (continued):

Eight months after the issue date of March 31, 2011, is November 31, 2011. Since November has only 30 days, use the last day of November as the maturity date. Adding three days’ grace, the legal due date is December 3, 2011. Therefore, the timeframe is March 31, 2011, to December 3, 2011. By counting the days in between (1 + 30 + 31 + 30 + 31 + 31 + 30 + 31 + 30 + 2) or using a calculator, you find that there are 247 days between these dates.

Step 2:

247 days out of 365 days in a year is t=247365

Step 3:

S=$7,500(1+0.06(247365))=$7,804.52

Calculator Instructions

For the days between dates in step 1, use the DATE function:

| DT1 | DT2 | DBD | Mode |

|---|---|---|---|

| 03.3111 | 12.0311 | Answer: 247 | ACT |

Corey owes Miller Enterprises $7,804.52 upon the legal due date for the promissory note.

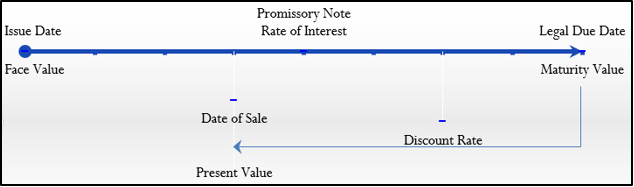

Selling a Promissory Note Before It Matures

Two months ago you established a promissory note to lend your friend the $5,000 to help him start his entrepreneurial venture. Now you have unexpectedly lost your job and find yourself in need of the money you loaned out. However, the note does not require your friend to repay the debt for another four months. Is there any way you can access your money?

During the life of a promissory note, its holder (the lender) may be unable to wait until the end of the term to get paid back and so sell the note to another investor. It is generally up to both parties to negotiate a fair interest rate for the sale of the note. This interest rate might be based on prevailing interest rates in the market at the time of the sale or just a mutually agreed-upon rate. This negotiated interest rate is sometimes called a discount rate, since the process to sell the note requires the removal of interest from the maturity value of the promissory note.

How It Works

When selling a promissory note before its maturity date, always follow a three-step procedure:

Step 1: Identify the promissory note information and selling information. For the promissory note, this includes the face value of the promissory note, the agreed-upon interest rate, and the legal due date. For selling the note, the discount rate and the time of the sale must be known. If necessary, draw a timeline to illustrate the transaction as illustrated in the figure below.

Step 2: Calculate the maturity value of the promissory note itself using the face value, promissory note rate of interest, and the time period involved with the legal due date.

Step 3: Calculate the present value of the note at the date of sale using the maturity value of the note, the new discount rate, and the time between the date of the sale and the legal due date.

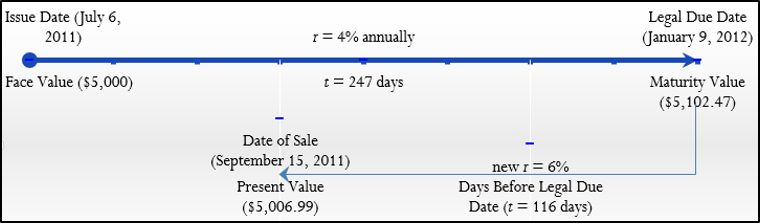

Assume in the example that you negotiated an interest rate of 6% with the buyer of the promissory note, and that the date of sale was September 15, 2011. The timeline illustrates the two steps:

Step 1: For the promissory note, the face value is $5,000, interest rate is 4% annually, and the time is from July 6, 2011, to January 9, 2012, previously calculated as 187 days. For selling the note, the discount rate is 6%. The selling date is September 15, 2011, which works out to 116 days before the legal due date.

Step 2: Applying Formula 8.2, calculate the maturity value of the promissory note on the legal due date. From previous calculations, the promissory note is worth $5,102.47 on January 9, 2012, when the borrower repays the note. This is the value that an investor purchasing the note receives in the future.

Step 3: Now sell the note using the discount rate and time before the legal due date. Applying Formula 8.2, rearrange and solve for P=$5,102.47/(1+(0.06×)=$5,006.99.

The $5,006.99 is how much the buyer of the promissory note pays based on the negotiated interest rate. This is sometimes called the proceeds, which is the amount of money received from a sale. The buyer now holds the promissory note and receives the full payment of $5,102.47 on January 9, 2012, from the borrower. This earns the buyer a 6% rate of interest on the investment.

Important Notes

If the original promissory note is noninterest-bearing, remember you can skip the second step above, since the face value of the note equals the maturity value upon the legal due date.

Things To Watch Out For

When working with the sale of a promissory note to another investor, the most common mistake is to mix up the interest rates. Remember that you use the original, stated interest rate of the promissory note in calculating the maturity value on the legal due date. When calculating the selling price, you must use the new negotiated rate to discount the maturity value.

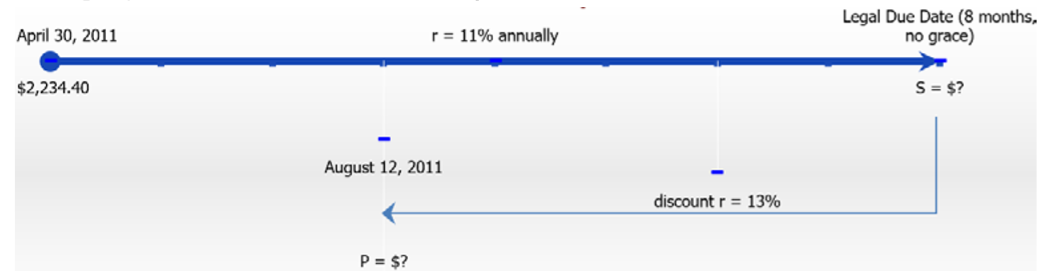

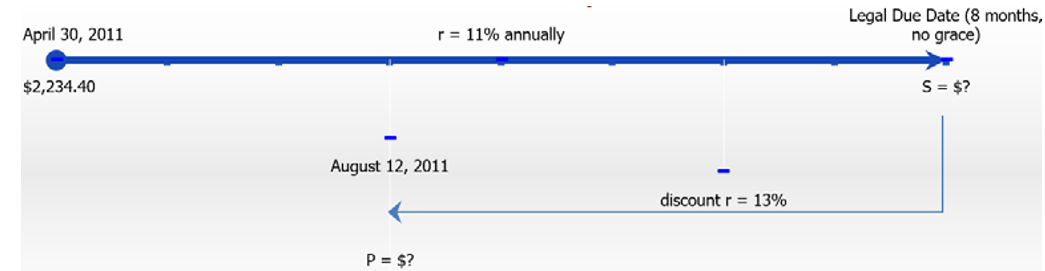

On April 30, 2011, Bernie purchased some furniture from Fran’s Fine Furniture on a 10-month no payment plan. A promissory note was created establishing an interest rate of 11% and it included the clause “no grace.” The furniture purchase was for $2,234.40. On August 12, 2011, Fran’s Fine Furniture sold the promissory note to an investor at an agreed-upon interest rate of 13%. What were the proceeds of the sale?

Solution

Calculate the proceeds of the sale. This represents a present value calculation (P) based on the maturity value of the original promissory using the discount rate.

What You Already Know

Step 1:

The following information about the promissory note and sale are known:

Original Promissory Note: Issue Date = April 30, 2011, P=$2,234.40, Term = 10 months, no grace, r=11% per year

Sale of Promissory Note: Sale Date = August 12, 2011, Discount r=13% per year

How You Will Get There

Step 1 (continued):

Calculate the legal due date, accounting for the no grace clause, and transform it into the number of days expressed annually to match the interest rate. Also calculate the number of days between the legal due date and the sale date, expressing it annually to match the interest rate.

Step 2:

To arrive at the maturity value, apply Formula 8.2.

Step 3:

To arrive at the present value using the new interest rate, apply Formula 8.2, rearranging for P.

Perform

Step 1 (continued):

Ten months from April 30, 2011, is February 30, 2012, which is adjusted to the last day of the month, or February 29, 2012. No grace period is added. By counting the days in between (1 + 31 + 30 + 31 + 31 + 30 + 31 + 30 + 31 + 31 + 29) or using a calculator, you find that there are 305 days between the dates. Thus t=305365 expressed annually.

Step 1 (continued):

Using a selling date of August 12, 2011, and the legal due date of February 29, 2012, count the days in between (19 + 30 + 31 + 30 + 31 + 31 + 29) or use a calculator to determine there are 201 days between the dates. Thus, t=201365 expressed annually.

Step 2:

S=$2,234.40(1+0.11(305365))=$2,439.78

Step 3:

P=$2,439.781+0.13(201355)=$2,276.79

Calculator Instructions

Use the DATE function to calculate number of days between:

| DT1 | DT2 | DBD | Mode | |

|---|---|---|---|---|

| Original Promissory Note | 04.3011 | 02.2912 | Answer: 305 | ACT |

| Sale of Promissory Note | 08.1211 | √ | Answer: 201 | ACT |

When Fran’s Fine Furniture sold the note to the investor, the proceeds of the sale were $2,276.

A noninterest-bearing promissory note was issued on January 31 with a face value of $10,000 and a term of eight months. On May 28 the note was sold to an investor at an agreed-upon interest rate of 5% per year. What was the sale price of the promissory note? Assume February is in a non–leap year.

Solution

Calculate the proceeds of the sale. This represents a present value calculation (P) based on the maturity value of the original promissory using the discount rate.

What You Already Know

Step 1:

The following about the promissory note and sale are known:

Original Promissory Note: Issue Date =January 31 Term = 8 months, P=$10,000, r=0%

Sale of Promissory Note: Sale Date = May 28 Discount r=5% per year

How You Will Get There

Step 1 (continued):

Calculate the legal due date by adding three days. Also calculate the number of days between the legal due date and the sale date, expressing it annually to match the interest rate.

Step 2:

The promissory note is noninterest-bearing, so the maturity value equals the face value.

Step 3: To arrive at the present value using the new interest rate, apply Formula 8.2, rearranging for P.

Perform

Step 1 (continued):

Add eight months to January 31, arriving at September 31. Adjust this to the last day of the month, September 30. Adding three days’ grace gives you a legal due date of October 3.

Step 1 (continued):

Using a selling date of May 28 and the legal due date of October 3, count the days in between (4 + 30 + 31 + 31 + 30 + 2) or use a calculator to determine that there are 128 days between the dates. Thus, t=128365 expressed annually.

Step 2:

P=S=$10,000

Step 3:

P=$10,0001+0.05(128365)=$9,827.68

Calculator Instructions

Assume a non-leap year of 2011 and use the DATE function to calculate number of days

| DT1 | DT2 | DBD | Mode |

|---|---|---|---|

| 04.2811 | 10.0311 | Answer: 128 | ACT |

The promissory note was sold for $9,827.68 on May 28.

References

- Bills of Exchange Act, R.S.C., 1985, c. B-4, Part IV Promissory Notes, §176. Available at http://laws-lois.justice.gc.ca/eng/a...B-4/index.html.