9.3: Determining the Present Value

- Page ID

- 22119

Should you pay your bills early? If so, what amount should be paid? From a strictly financial perspective, if you are going to pay a bill earlier than its due date, the amount needs to be reduced somehow. If not, then why pay it early?

To illustrate, assume that you just received a $3,000 bonus from your employer. Stopping at your mailbox, you pick up a large stack of envelopes that include a financial statement for your $3,000 purchase of furniture from The Brick on its three-year, no-interest, no-payments plan. Should you use your bonus to extinguish this debt? The choices are that you can either pay $3,000 today or $3,000 three years from now.

- If you pay the bill today, The Brick can then take your money and invest it themselves for the next three years. At 2.75% compounded semi-annually, The Brick earns $256.17. At the end of your agreement, The Brick then has both your $3,000 payment and the additional interest of $256.17! You might as well have just paid The Brick $3,256.17 for your furniture!

- If you invest your bonus instead and pay your bill when it is due, The Brick receives its $3,000 and you have the $256.17 of interest left over in your bank account. Clearly, this is the financially smart choice.

For The Brick to be financially equitable in its dealings with you, it must reduce any early payment by an amount such that with interest the value of your payment accumulates to the debt amount upon the maturity of the agreement. This means that The Brick should be willing to accept a payment of $2,763.99 today as payment in full for your $3,000 bill. If The Brick then invests that payment at 2.75% compounded semi-annually, it grows to $3,000 when your payment becomes due in three years.

Whether you are paying bills personally or professionally, it is important to understand present value. The amount of interest to be removed from a future value needs to reflect both how far in advance the payment occurs and an equitable interest rate. In this section, you calculate the present value of a future lump-sum amount under both conditions of constant variables and changing variables.

Present Value Calculations with No Variable Changes

As in your calculations of future value, the simplest scenario for present value is for all the variables to remain unchanged throughout the entire transaction. This still involves compound interest for a single payment or lump-sum amount and thus does not require a new formula.

The Formula

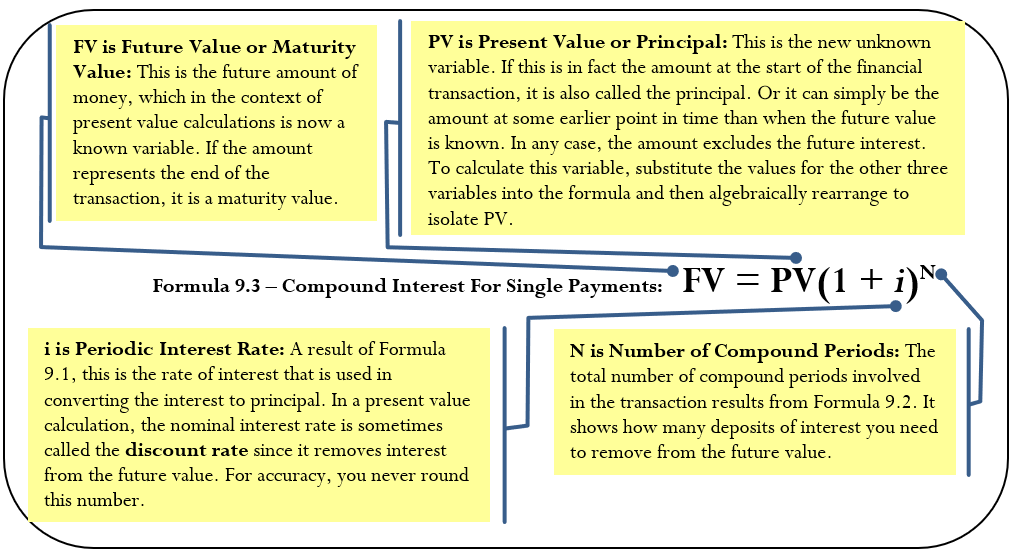

Solving for present value requires you to use Formula 9.3 once again. The only difference is that the unknown variable has changed from \(FV\) to \(PV\).

How It Works

Follow these steps to calculate the present value of a single payment:

Step 1: Read and understand the problem. If necessary, draw a timeline identifying the future value, the nominal interest rate, the compounding, and the term.

Step 2: Determine the compounding frequency (\(CY\)) if it is not already known, and calculate the periodic interest rate (\(i\)) by applying Formula 9.1.

Step 3: Calculate the number of compound periods (\(N\)) by applying Formula 9.2.

Step 4: Substitute into Formula 9.3, rearranging algebraically to solve for the present value.

Revisiting that furniture you bought on The Brick’s three-year, no-interest and no-payments plan, if the amount owing three years from now is $3,000 and prevailing market interest rates are 2.75% compounded semi-annually, what should The Brick be willing to accept as full payment today?

Step 1: The value of the payment today (\(PV\)) is required. The future value (\(FV\)) is $3,000. The nominal interest rate is \(IY = 2.75\%\), and the compounding frequency of semi-annually is \(CY= 2\). The term is to pay it three years early.

Step 2: The periodic interest rate is \(i=2.75 \% / 2=1.375 \%\).

Step 3: The number of compounds is \(N=3 \times 2=6\).

Step 4: Applying Formula 9.3, \(\$ 3,000=PV(1+0.01375)^{6} \text { or } PV=\dfrac{\$ 3.000}{1.01375^{6}}=\$ 2,763.99\).

If The Brick will accept $2,763.99 as full payment, then pay your bill today. If not, keep your money, invest it yourself, and then pay the $3,000 three years from now while retaining all of the interest earned.

Important Notes

You use the financial calculator in the exact same manner as described in Section 9.2. The only difference is that the unknown variable is \(PV\) instead of \(FV\). You must still load the other six variables into the calculator and apply the cash flow sign convention carefully.

Paths To Success

Did you notice the following?

- Future Value This calculation takes the present value and multiplies it by the interest factor. This increases the single payment by the interest earned.

- Present Value This calculation takes the future value and divides it by the interest factor (rearranging Formula 9.3 for PV produces \(\dfrac{FV}{(1+t)^{N}}=PV\)). This removes the interest and decreases the single payment.

Castillo’s Warehouse will need to purchase a new forklift for its warehouse operations three years from now, when its new warehouse facility becomes operational. If the price of the new forklift is $38,000 and Castillo’s can invest its money at 7.25% compounded monthly, how much money should it put aside today to achieve its goal?

Solution

You aim to calculate the amount of principal that Castillo’s must put aside today such that it can grow with interest to the desired savings goal. The principal today is the present value (\(PV\)).

What You Already Know

Step 1:

The maturity value, interest rate, and term are known: \(FV\) = $38,000; \(IY\) = 7.25%; \(CY\) = monthly = 12 times per year; Term = 3 years

How You Will Get There

Step 2:

Calculate the periodic interest by applying Formula 9.1.

Step 3:

Calculate the number of compound periods by applying Formula 9.2.

Step 4:

Calculate the present value by substituting into Formula 9.3 and then rearranging for \(PV\).

Perform

Step 2:

\[i=\dfrac{7.25 \%}{12}=0.6041 \overline{6} \%=0.006041 \overline{6} \nonumber \]

Step 3:

\[N=12 \times 3=36 \nonumber \]

Step 4:

\[\begin{aligned}

&\$ 38,000=PV(1+0.006041 \overline{6})^{36}\\

&PV=\frac{\$ 38,000}{(1+0.0060416)^{36}}=\$ 30,592.06

\end{aligned} \nonumber \]

Calculator Instructions

| N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|

| 36 | 7.25 | Answer: $30,592.06 | 0 | 38000 | 12 | 12 |

If Castillo’s Warehouse places $30,592.06 into the investment, it will earn enough interest to grow to $38,000 three years from now to purchase the forklift.

Present Value Calculations with Variable Changes

Addressing variable changes in present value calculations follows the same techniques as future value calculations. You must break the timeline into separate time segments, each of which involves its own calculations.

Solving for the unknown \(PV\) at the left of the timeline means you must start at the right of the timeline. You must work from right to left, one time segment at a time using Formula 9.3, rearranging for \(PV\) each time. Note that the present value for one time segment becomes the future value for the next time segment to the left.

How It Works

Follow these steps to calculate a present value involving variable changes in single payment compound interest:

Step 1: Read and understand the problem. Identify the future value. Draw a timeline broken into separate time segments at the point of any change. For each time segment, identify any principal changes, the nominal interest rate, the compounding frequency, and the segment’s length in years.

Step 2: For each time segment, calculate the periodic interest rate (\(i\)) using Formula 9.1.

Step 3: For each time segment, calculate the total number of compound periods (\(N\)) using Formula 9.2.

Step 4: Starting with the future value in the first time segment on the right, solve Formula 9.3.

Step 5: Let the present value calculated in the previous step become the future value for the next time segment to the left. If the principal changes, adjust the new future value accordingly.

Step 6: Using Formula 9.3, calculate the present value of the next time segment.

Step 7: Repeat steps 5 and 6 until you obtain the present value from the leftmost time segment.

Important Notes

To use your calculator efficiently in working through multiple time segments, follow a procedure similar to that for future value:

- Load the calculator with all the known compound interest variables for the first time segment on the right.

- Compute the present value at the beginning of the segment.

- With the answer still on your display, adjust the principal if needed, change the cash flow sign by pressing the ± key, then store the unrounded number back into the future value button by pressing \(FV\). Change the \(N\), \(I/Y\), and \(C/Y\) as required for the next segment.

Return to step 2 for each time segment until you have completed all time segments.

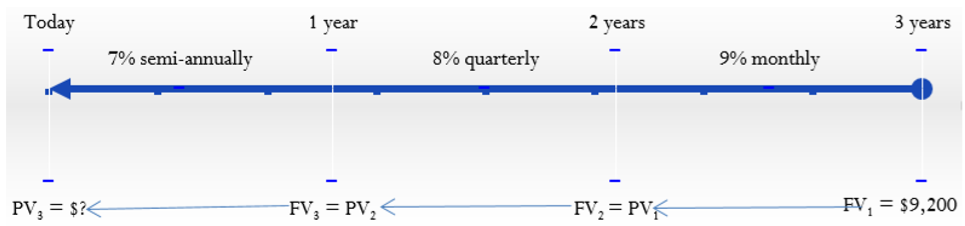

Sebastien needs to have $9,200 saved up three years from now. The investment he is considering pays 7% compounded semi-annually, 8% compounded quarterly, and 9% compounded monthly in successive years. To achieve his goal, how much money does he need to place into the investment today?

Solution

Take the maturity amount and bring it back to today by removing the interest. Notice you are dealing with a single lump sum with multiple successive interest rates. The amount of money to be invested today is the principal (\(PV\)).

What You Already Know

Step 1:

The maturity amount, terms, and interest rates are on the timeline:

\(FV_1\) = $9,200

Starting from the right end of the timeline and working backwards:

First time segment: \(IY\) = 9%; \(CY\) = monthly = 12 Term = 1 year

Second time segment: \(IY\) = 8%; \(CY\) = quarterly = 4 Term = 1 year

Third time segment: \(IY\) = 7%; \(CY\) = semi-annually = 2 Term = 1 year

How You Will Get There

Step 2:

For each time segment, calculate the periodic interest rate by applying Formula 9.1.

Step 3:

For each time segment, calculate the number of compound periods by applying Formula 9.2.

Step 4:

Calculate the present value of the first time segment using Formula 9.3 and rearrange for \(PV_1\).

Step 5:

Assign \(FV_2 = PV_1\).

Step 6:

Reapply Formula 9.3 and isolate \(PV_2\) for the second time segment.

Step 7:

Assign \(FV_3 = PV_2\). Reapply Formula 9.3 and isolate \(PV_3\) for the third time segment.

Perform

Step 2:

First segment: \(i=\dfrac{9 \%}{12}=0.75 \%\)

Second segment: \(i=\dfrac{8 \%}{4}=2 \%\)

Third segment: \(i=\dfrac{7 \%}{2}=3.5 \%\)

Step 3:

First segment: \(N=12 \times 1=12\)

Second segment: \(N=4 \times 1=4\)

Third segment: \(N=2 \times 1=2\)

Step 4:

\[\begin{aligned} \$ 9,200&=PV_{1} \times(1+0.0075)^{12} \\ PV_{1}&=\dfrac{\$ 9,200}{1.0075^{12}}\\ &=\$ 8,410.991026 \end{aligned} \nonumber \]

Step 5:

\[FV_{2}=\$ 8,410.991026 \nonumber \]

Step 6:

\[\begin{aligned}

\$ 8,410.991026&=PV_{2} \times(1+0.02)^{4} \\

PV_{2}&=\dfrac{\$ 8,410.91026}{1.02^{4}}\\

&=\$ 7,770.455587

\end{aligned} \nonumber \]

Step 7:

\[\begin{aligned}

&\mathrm{FV}_{3}=\$ 7,770.455587\\

&\begin{array}{l}

{\$ 7,770.455587=\mathrm{PV}_{3} \times(1+0.035)^{2}} \\

{\mathrm{PV}_{3}=\dfrac{\$ 7,770.455587}{1.035^{2}}=\$ 7,253.80}

\end{array}

\end{aligned} \nonumber \]

Calculator Instructions

| Time Segment | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 1 | 12 | 9 | Answer: -$8,410.991026 | 0 | 9200 | 12 | 12 |

| 2 | 4 | 8 | Answer: $7,770.455587 | \(\surd\) | 8410.991026 | 4 | 4 |

| 3 | 2 | 7 | Answer: -$7,253.803437 | \(\surd\) | 7770.455587 | 2 | 2 |

Sebastien needs to place $7,253.80 into the investment today to have $9,200 three years from now.

Paths To Success

When you calculate the present value of a single payment for which only the interest rate fluctuates, it is possible to find the principal amount in a single division:

\[PV=\dfrac{FV}{\left(1+i_{1}\right)^{N_{1}} \times\left(1+i_{2}\right)^{N_{2}} \times \ldots \times\left(1+i_{n}\right)^{N_{n}}}\nonumber \]

where \(n\) represents the time segment number. Note that the technique in Example \(\PageIndex{2}\) resolves each of these divisions one step at a time, whereas this technique solves them all simultaneously. You can calculate the same principal as follows:

\[PV=\dfrac{\$ 9,200}{(1.0075)^{12} \times(1.02)^{4} \times(1.035)^{2}}=\$ 7,253.80\nonumber \]

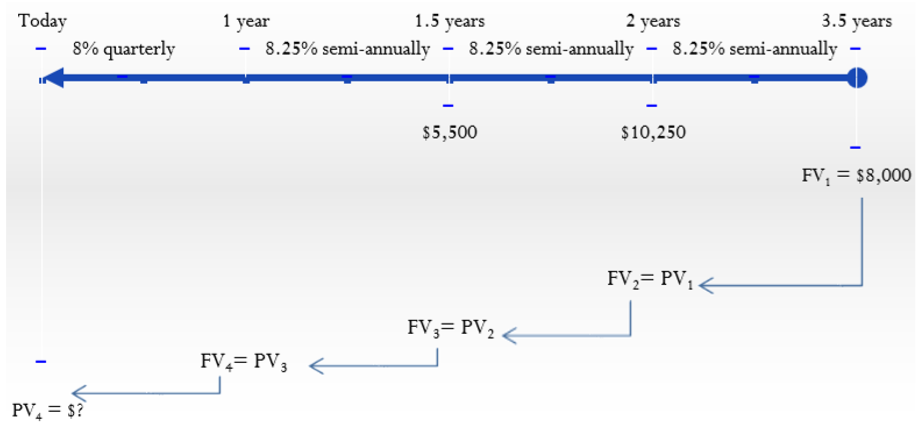

Birchcreek Construction has three payments left on a debt obligation in the amounts of $5,500, $10,250, and $8,000 due 1.5 years, 2 years, and 3.5 years from today. Prevailing interest rates are projected to be 8% compounded quarterly in the first year and 8.25% compounded semi-annually thereafter. If Birchcreek wants to settle the debt today, what amount should the creditor be willing to accept?

Solution

Take the three lump-sum payments in the future and remove the interest back to today to find the fair amount that Birchcreek Construction should pay. This is the present value (\(PV\)).

What You Already Know

Step 1:

With multiple amounts and interest rates, the timeline displays the changing variables. There are four time segments. The \(IY\), \(CY\), and Term are identified for each.

How You Will Get There

Step 2:

For each segment, calculate the periodic interest rate by applying Formula 9.1.

Step 3:

For each segment, calculate the number of compound periods by applying Formula 9.2.

Step 4:

Calculate the present value of the first time segment using Formula 9.3 and rearrange for \(PV_1\).

Step 5:

Assign \(FV_2 = PV_1\) and increase by the additional lump-sum payment.

Step 6:

Reapply Formula 9.3 and isolate \(PV_2\) for the second time segment:.

Step 7:

Assign \(FV_3 = PV_2\) and increase by the additional lump-sum payment. Reapply Formula 9.3 and isolate \(PV_3\) for the third time segment.

Repeat Step 7: Assign \(FV_4 = PV_3\). Reapply Formula 9.3 and isolate \(PV_4\) for the final time segment.

Perform

Step 2:

First segment: \(i=\dfrac{8.25 \%}{2}=4.125 \%\)

Second segment: \(i=\dfrac{8.25 \%}{2}=4.125 \%\)

Third segment: \(i=\dfrac{8.25 \%}{2}=4.125 \%\)

Fourth segment: \(i=\dfrac{8 \%}{4}=2 \%\)

Step 3:

First segment: \(N=2 \times 1.5=3\)

Second segment: \(N=2 \times \dfrac{1}{2}=1\)

Third segment: \(N=2 \times \dfrac{1}{2}=1\)

Fourth segment: \(N=4 \times 1=4\)

Step 4:

\[\begin{aligned}

\$ 8,000&=PV_{1} \times(1+0.04125)^{3} \\

P V_{1}&=\dfrac{\$ 8,000}{1.04125^{3}}\\

&=\$ 7,086.388265

\end{aligned} \nonumber \]

Step 5:

\[FV_{2}=\$ 7,086.388265+\$ 10,250.00=\$ 17,336.38826 \nonumber \]

Step 6:

\[\begin{aligned}

&\$ 17,336.38826=PV_{2} \times(1+0.04125)^{1}\\

&P V_{2}=\dfrac{\$ 17,336.3826}{1.04125}=\$ 16,649.59257

\end{aligned} \nonumber \]

Step 7:

\[\begin{aligned}

FV_{3}&=\$ 16,649.59257+\$ 5,500.00=\$ 22,149.59257 \\

\$ 22,149.59257&=PV_{3} \times(1+0.04125)^{1} \\

PV_{3}&=\dfrac{\$ 22,149.59257}{1.04125}=\$ 21,272.11772

\end{aligned} \nonumber \]

Repeat Step 7:

\[\begin{aligned}

&FV_{4}=\$ 21,272.11772\\

&\$ 21,272.11772=PV_{4} \times(1+0.02)^{4}\\

&PV_{4}=\dfrac{\$ 21,272.11772}{1.02^{4}}=\$ 19,652.15

\end{aligned} \nonumber \]

Calculator Instructions

| Time Segment | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 1 | 3 | 8.25 | Answer: -\$7,086.388265 | 0 | 8000 | 2 | 2 |

| 2 | 1 | \(\surd\) | Answer: -$16,649.59257 | \(\surd\) | 17336.38826 | \(\surd\) | \(\surd\) |

| 3 | \(\surd\) | \(\surd\) | Answer: -$21,272.11772 | \(\surd\) | 22149.59257 | \(\surd\) | \(\surd\) |

| 4 | 4 | 8 | Answer: -$19,652.14865 | \(\surd\) | 21272.11772 | \(\surd\) | \(\surd\) |

Using prevailing market rates, the fair amount that Birchcreek Construction owes today is $19,652.15.