10.3: Application - Savings Bonds

- Page ID

- 22126

How does Canada finance its long-term debt? One way is through savings bonds, or SBs for short, which are longterm financial instruments with 10-year maturities issued only by the federal Canadian government. Approximately $8.8 billion of savings bonds were outstanding in August 2012, representing approximately 1.4% of the gross national debt. Compare this with the 27% of Canada’s national debt financed through treasury bills, the short-term instrument you studied in Section 8.6. For up-to-date information on CSBs, visit http://csb.gc.ca/home.

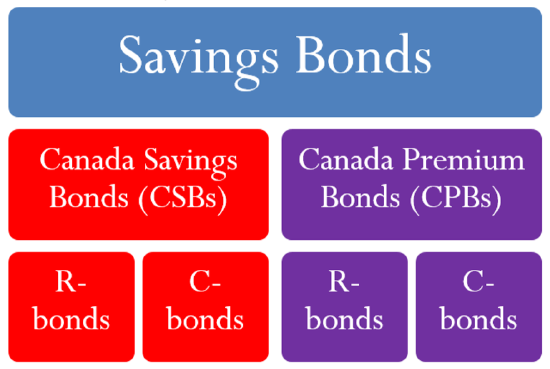

Key Characteristics of Savings Bonds

Similar to T-bills, SBs are purchased by financial institutions who, in turn, sell the SBs to investors like you and me. Savings bonds have six key characteristics:

- Denomination. SBs are issued only in denominations of $100, $300, $500, $1,000, $5,000, and $10,000.

- Term. SBs are issued with 10-year maturity dates and can be purchased only on their issue date.

- Issuance. From 1998 to 2010, SBs have been issued on the first of every month from November through April inclusive (six times per year). Starting in 2011, SBs are issued only in November and December.

- Calculation of Interest. Interest on SBs is always calculated using one of two methods:

- Regular interest SBs, called R-bonds, pay the interest annually to the owner of the bond and do not convert the interest to principal. This is identical to an interest payout GIC. The lowest denomination available for these bonds is $300.1

- Compound interest SBs, called C-bonds, annually convert the interest earned from the bond to principal. This is identical to a compound interest GIC. These bonds are available in any denomination.

- Types of Bonds. SBs are issued in two versions distinguished by when they can be redeemed. The figure to the right illustrates the combination of versions and interest calculations available.

- Canada Savings Bonds (CSBs) are redeemable at any time. If they are redeemed during an anniversary month (that is, a multiple of 12 months from the issuance date), they receive interest for the full year, according to the R-bond or C-bond rules as appropriate. If they are redeemed during a non-anniversary month, they receive the annual interest plus interest for the partial year using simple interest calculations on the basis of the number of full months. For example, if a CSB with an anniversary date of November 1 is redeemed on January 23, simple interest for the partial year is paid only for the two full months from November 1 to January 1. CSBs pay a lower interest rate because of the privilege of redemption. When they are issued, the interest rate is generally known for the first year only, though sometimes multiyear rates are posted. Usually, each subsequent year will have its new interest rate announced in a timely fashion.

- Canada Premium Bonds (CPBs) have all the same characteristics of CSBs except that they are redeemable only during the anniversary month based on the month of issue. The actual day of the month does not matter. These bonds pay a higher interest rate premium, historically 0.6% to 2.65% higher, for not being redeemable at any time. When CPBs are issued, the interest rate is known for the first three years, and thereafter announced for periods of one to three years at a time.

- Identification. All SBs when issued are assigned a series letter and number.

- CSBs start with the letter "S" and as of November 2012 were on issue number "130." This is referred to as "Series S130."

- CPBs start with the letter "P" and as of December 2012 were on issue "81." This is referred to as "Series P81."

Interest Rates on Savings Bonds

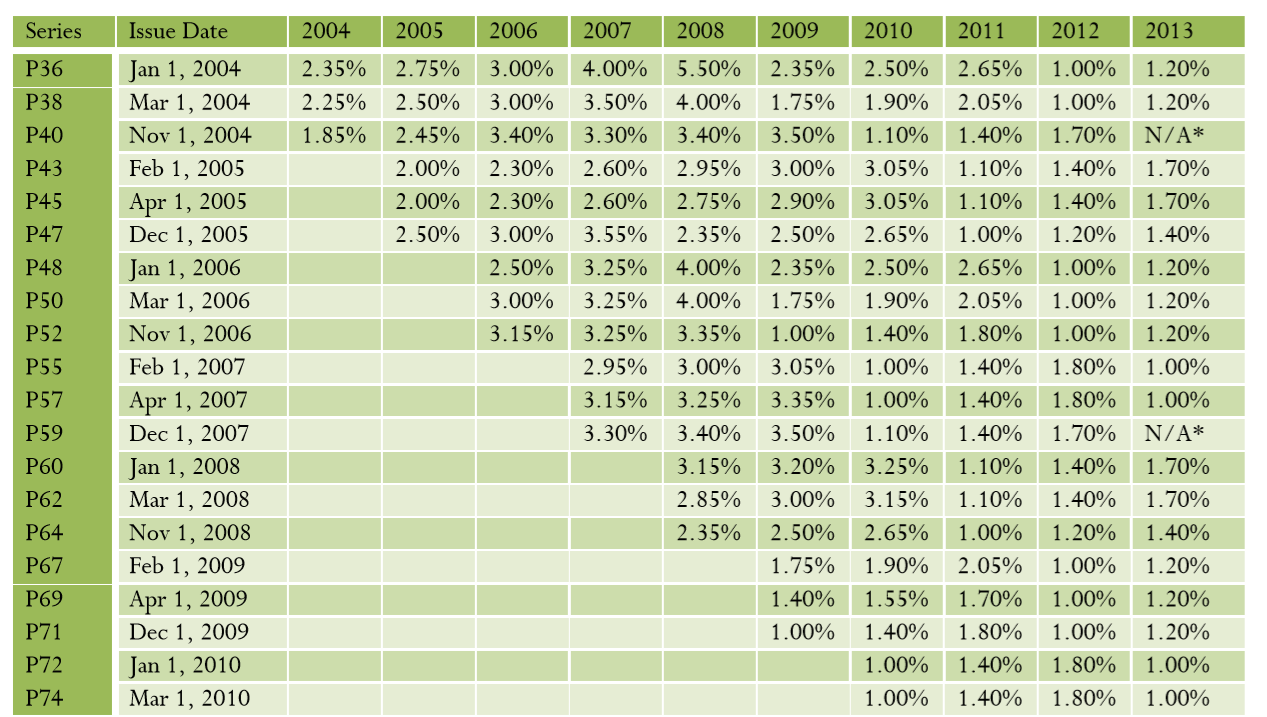

The posted interest rates on savings bonds are based on current market conditions either at the time of issue or upon each anniversary. The rates are related to the Bank of Canada interest rate. Generally, for CSBs the interest rate set is slightly above the Bank of Canada rate by approximately 0.15% to 0.25%, though this margin is not fixed. Similarly for CPBs, the rate is commonly 0.5% to 1% higher than the Bank of Canada rate, though again the margin is not fixed. The historic interest rates since 2004 for CSBs are listed in the table below. Since 2004, all series of CSBs (starting with S86 up to S130) have received the same annual interest rate based on their month of issue. Series prior to 2004 (S85 and earlier) may have individually different interest rates; you should not use this table for those bonds.

Interest Rates on Savings Bonds

The posted interest rates on savings bonds are based on current market conditions either at the time of issue or upon each anniversary. The rates are related to the Bank of Canada interest rate. Generally, for CSBs the interest rate set is slightly above the Bank of Canada rate by approximately 0.15% to 0.25%, though this margin is not fixed. Similarly for CPBs, the rate is commonly 0.5% to 1% higher than the Bank of Canada rate, though again the margin is not fixed.

The historic interest rates since 2004 for CSBs are listed in the table below. Since 2004, all series of CSBs (starting with S86 up to S130) have received the same annual interest rate based on their month of issue. Series prior to 2004 (S85 and earlier) may have individually different interest rates; you should not use this table for those bonds. Issue

| Issue/Anniversary Date* | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|---|---|

| January 1 | 1.65% | 1.65% | 2.62% | 2.90% | 3.10% | 1.65% | 0.40% | 0.65% | 0.65% | 0.5% |

| February 1 | 1.55% | 1.55% | 2.68% | 2.80% | 2.85% | 1.25% | 0.40% | 0.65% | 0.65% | 0.5% |

| March 1 | 1.30% | 1.55% | 2.75% | 3.10% | 2.50% | 1.00% | 0.40% | 0.65% | 0.65% | 0.5% |

| April 1 | 1.25% | 1.65% | 2.75% | 3.10% | 2.45% | 0.75% | 0.40% | 0.65% | 0.65% | 0.5% |

| November 1 | 1.50% | 2.50% | 3.00% | 3.25% | 2.00% | 0.40% | 0.65% | 0.5% | 0.5% | N/A** |

| December 1 | 1.50% | 2.56% | 3.00% | 3.25% | 1.85% | 0.40% | 0.65% | 0.5% | 0.5% | N/A** |

| Series Issued (in monthly order) | S86 to S91 | S92 to S97 | S98 to S103 | S104 to S109 | S110 to S115 | S116 to S121 | S122 to S127 | S128 to S129† | S130‡ | No series issued** |

All interest rates are annual.

* This table is only valid for all CSBs with issue dates of January 1, 2004, and later, starting with S86 up to S130.

† In 2011, the Canadian Government ceased issuing CSBs in January through April. The series numbers represent November and December series.

‡ No CSBs were issued in December 2012. Thus, the series number is for November 2012.

** At time of writing, these rates were not available yet.

From 1998 to 2010, six series were issued annually, with the posted interest rate lasting for only one year. For example, Series S105 was issued on February 1, 2007, at an interest rate of 2.80%, with annual changes on February 1 to 2.85% in 2008, 1.25% in 2009, 0.40% in 2010, and 0.65% in both 2011 and 2012. As another example, Series S113 was issued on April 1, 2008, at an interest rate of 2.45%, with annual changes on April 1 to 0.75% in 2009, 0.40% in 2010, and 0.65% in both 2011 and 2012.

The historic interest rates for a sample of CPBs since 2004 are listed in the next table. Unlike their CSB counterparts, each CPB has its own individual interest rate. To see more information on historic CPB rates or rates on older CSBs, visit http://csb.gc.ca/about/rates.

All interest rates are annual.

* At time of writing, these rates were not available yet.

Calculating Interest Amounts and Maturity Values on Savings Bonds

The mathematics of savings bonds focuses on the two things most important to investors:

- What amount of interest is earned?

- What is the maturity value?

The Formula

Savings bonds require a combination of seven previously introduced formulas:

- Formula 8.1 Simple Interest: \(I = PVrt\)

- Formula 8.2 Simple Interest for Single Payments: \(FV = PV(1 + rt)\)

- Formula 8.3 Interest Amount for Single Payments: \(I = FV − PV\)

- Formula 9.1 Periodic Interest Rate: \(i=\dfrac{I Y}{C Y}\)

- Formula 9.2 Number of Compound Periods for Single Payments: \(N = CY × \text {Years}\)

- Formula 9.3 Compound Interest for Single Payments: \(FV=PV(1+i)^N\)

- Formula 10.1 Periodic Interest Amount: \(I = PV × i\)

Savings bonds are always compounded annually, or \(CY = 1\). Therefore, it is possible to simplify a few variables and calculations in these formulas:

- In Formula 9.1, the periodic interest rate (i) is always the same as the nominal interest rate (\(IY\)), or \(i = IY\).

- When you calculate the future value using Formula 9.2 and Formula 9.3, each time segment is one year in duration, or Years = 1. Therefore, Formula 9.2 always produces \(N\) = 1. Additionally, you can then simplify Formula 9.3 to read \(FV = PV(1 + i)\).

How It Works

Follow these steps to work with regular interest savings bonds:

Step 1: Determine the principal (\(PV\)) invested in the bond on the issue date.

Step 2: Locate the historic interest rates for the applicable CSB or CPB. Once for each complete year that the bond is held, apply Formula 10.1 to calculate the annual interest amount paid out to the investor that year as of the most recent anniversary month. Round all amounts to two decimals.

Step 3: Sum the annual interest amounts that you calculated in step 2 to arrive at the total interest (\(I\)). Note that the maturity value (\(FV\)) is the same as the principal (\(PV\)). If the bond is being redeemed in an anniversary month, this is the last step. For CSBs being redeemed in a non-anniversary month, proceed with step 4.

Step 4: Calculate the number of complete months (\(t\)) that the CSB is held after the most recent anniversary date. Using the interest rate (\(r\)) for the partial year, apply Formula 8.1 to calculate the interest payment amount for the partial year. Add this amount to the previously totaled interest amount in step 3 to arrive at a final total interest earned (\(I\)). The maturity value (\(FV\)) remains the same as the principal (\(PV\)).

Follow these steps to work with compound interest savings bonds:

Step 1: Determine the principal (\(PV\)) invested in the bond on the issue date.

Step 2: Locate the historic interest rates for the applicable CSB or CPB. Once for each complete year that the bond is held, apply Formula 9.3 to calculate the maturity amount as of the most recent anniversary month. Recall in each repetition that the \(FV\) of a prior calculation becomes the new \(PV\) in the subsequent calculation.

Step 3: The maturity value (\(FV\)) is the final result of step 2. If the interest amount (\(I\)) earned to date is required, apply Formula 8.3. If the bond is being redeemed in an anniversary month, this is the last step. For CSBs being redeemed in a non-anniversary month, proceed with step 4.

Step 4: Take the unrounded maturity value from step 3 and make it the new present value (\(PV\)). Calculate the number of complete months (\(t\)) that the CSB is held after the most recent anniversary date. Using the interest rate (\(r\)) for the partial year, apply Formula 8.2 to arrive at the final maturity value (\(FV\)) for the CSB. To calculate the total interest on the bond from purchase to redemption, take this final maturity value (\(FV\)) and subtract the principal (\(PV\)) that you identified in step 1.

Things To Watch Out For

When working with the simple interest formulas (8.1 and 8.2), recall that the interest rate (\(r\)) and the time (\(t\)) need to be in the same units. With annual interest rates on savings bonds, you must convert the monthly time to an annual format by taking the number of months and dividing by 12 (\(t = \text{months} / 12\)).

Paths To Success

Two methods can be used to speed up the calculations required for compound interest savings bonds.

- Step 2 Formula Adaptation: Recall that when calculating the future value of a single payment for which only the interest rate fluctuates, you can calculate the maturity amount by formula in a single multiplication: \[FV=PV \times\left(1+i_{1}\right)^{N_{1}} \times\left(1+i_{2}\right)^{N_{2}} \times \ldots \times\left(1+i_{n}\right)^{N_{n}} \nonumber \]where \(n\) represents the total complete years that the savings bond is held. With annual compounding where \(N = 1\) and \(IY = i\), you can simplify this further: \[FV=PV \times\left(1+IY_{1}\right) \times\left(1+IY_{2}\right) \times \ldots \times\left(1+IY_{n}\right) \nonumber \]

- Step 4 Simple Interest BAII Plus Calculator Adaptation: If you have used the calculator for compound interest calculations, you can continue to use it to compute the \(FV\) for the final partial year at simple interest. Just input \(r × t\) into the I/Y button while leaving \(N\), \(P/Y\), and \(C/Y\) all equaling one.

- What is the maturity value of a $10,000 Series S91 CSB R-bond redeemed on December 1, 2009?

- Look at Table \(\PageIndex{1}\). As an example, note that S86 received a new interest rate of 0.40% on January 1, 2010. Also note that S122 was issued on January 1, 2010, at the same rate of 0.40%. Why do older CSBs such as S86 receive the same interest rate as newer CSBs such as S122?

- Which of the following investment amounts are not possible for R-bonds?

- $300

- $400

- $500

- $600

- $700

- $800

- Answer

-

- $10,000. An R-bond does not convert interest to principal, resulting in \(PV = FV\).

- Since CSBs can be redeemed at any time, if a newer CSB is given a more favourable interest rate than an older CSB, all investors would cash in their old CSBs and purchase the new CSB, effectively cancelling the old CSB.

- $400 and $700. The smallest denominations of R-bonds are $300 and $500.

Elisabeth invested in five $10,000 denomination Series S106 R-bond CSBs. How much interest will she earn in total if she redeems the bond on the following dates:

- March 1, 2011

- June 23, 2011

Solution

Calculate the total interest (\(I\)) that Elisabeth earned while in possession of the bond for each date.

What You Already Know

Step 1:

She has five bonds at $10,000 each, or \(PV\) = $50,000.

How You Will Get There

Step 2:

From the savings bond table, S106 was issued on March 1, 2007. The annual interest rates (\(i\)) from that point are 3.1% in 2007, 2.5% in 2008, 1.00% in 2009, 0.40% in 2010, and 0.65% in 2011. Remembering that \(i = IY\), for each of 2007, 2008, 2009, and 2010 apply Formula 10.1. This calculates all of the annual interest amounts paid each year up to March 1, 2011.

Step 3:

Total all of the interest from the previous step. This answers part (a).

Step 4:

For the second question, calculate t, which is the number of complete months after March 1, 2010. Then taking the new interest rate (\(r\)), apply Formula 8.1. Add this to the interest from Step 3 to arrive at the total interest for part (b).

Perform

Step 2:

\(PMT\)(2007) = $50,000 × 0.031 = $1,550

\(PMT\)(2008) = $50,000 × 0.025 = $1,250

\(PMT\)(2009) = $50,000 × 0.01 = $500

\(PMT\)(2010) = $50,000 × 0.004 = $200

Step 3:

\(I\) = $1,550 + $1,250 + $500 + $200 = $3,500 (if redeemed on March 1, 2011)

Step 4:

June 23 − March 1 = 3 complete months = \(t\); \(r\) = 0.65%

\(I\) = $50,000(0.0065)(3 12) = $81.25

Total \(I\) = $3,500 + $81.25 = $3,581.25 (if redeemed on June 23, 2010)

If Elisabeth redeems her five $10,000 S106 R-bond CSBs on March 1, 2011, she will have earned $3,500 in total interest. By holding onto it until June 23, 2011, she acquires an additional $81.25 of interest for a total of $3,581.25.

Dusty invested into two $10,000, three $1,000, and one $500 denomination Series P60 C-bond CPBs. She redeemed the bond in 2012.

- What was the maturity value?

- How much interest did she earn?

Solution

Calculate the maturity value of the bond (\(FV\)). Then determine the total interest (\(I\)).

What You Already Know

Step 1:

Her total investment was: \(PV\) = 2 × $10,000 + 3 × $1,000 + 1 × $500 = $23,500.

How You Will Get There

Step 2:

From the premium bond table, P60 was issued on January 1, 2008. The annual interest rates (\(i\)) from that point were 3.15% in 2008, 3.2% in 2009, 3.25% in 2010, and 1.10% in 2011. Since this is a CPB bond, the redemption in 2012 must be in January 2012 (the only month it can be redeemed). Remembering that \(N\) = 1 and \(i = IY\), adapt Formula 9.3 to calculate the maturity value of the bond:

\[FV=PV \times\left(1+i_{2008}\right) \times\left(1+i_{2009}\right) \times\left(1+i_{2010}\right) \times\left(1+i_{2011}\right) \nonumber \]

Step 3:

To calculate the interest, apply Formula 8.3.

Perform

Step 2:

\(FV\) = $23,500 × (1 + 0.0315) × (1 + 0.032) × (1 + 1.0325) × (1 + 1.011) = $26,113.07

Step 3:

\(I\) = $26,113.07 − $23,500.00 = $2,613.07

Calculator Instructions

| Year | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 2008 | 1 | 3.15 | -23500 | 0 | Answer: 24,240.25 | 1 | 1 |

| 2009 | \(\surd\) | 3.2 | \(\pm F V\) | \(\surd\) | Answer: 25,015.938 | \(\surd\) | \(\surd\) |

| 2010 | \(\surd\) | 3.25 | \(\pm F V\) | \(\surd\) | Answer: 25,828.95599 | \(\surd\) | \(\surd\) |

| 2011 | \(\surd\) | 1.1 | \(\pm F V\) | \(\surd\) | Answer: 26,113.0745 | \(\surd\) | \(\surd\) |

On her investment of $23,500, Dusty will have a maturity value of $26,113.07 in January of 2012. She earned $2,613.07 of interest.

What is the maturity value and amount of interest earned on a $10,000 denomination Series S95 C-bond CSB if it is redeemed on the following dates:

- April 1, 2011

- December 28, 2011

Solution

Calculate the maturity value (\(FV\)) and the total interest (\(I\)) on each of the noted dates.

What You Already Know

Step 1:

\(PV\) = $10,000.

How You Will Get There

Step 2:

From the savings bond table, S95 was issued on April 1, 2005. The annual interest rates (\(i\)) from that point on were 1.65% in 2005, 2.75% in 2006, 3.1% in 2007, 2.45% in 2008, 0.75% in 2009, 0.40% in 2010, and 0.65% in 2011. Remembering that \(N\) = 1 and \(i = IY\), adapt Formula 9.3 to calculate the maturity value of the bond:

\[FV=PV \times\left(1+i_{2005}\right) \times\left(1+i_{2006}\right) \times\left(1+i_{2007}\right) \times\left(1+i_{2008}\right) \times\left(1+i_{2009}\right) \times\left(1+i_{2010}\right) \nonumber \]

Step 3:

To calculate the interest as of April 1, 2011, apply Formula 8.3.

Step 4:

For the second question, calculate \(t\), which is the number of complete months after April 1, 2010. The \(FV\) from step 2 becomes the new \(PV\). Then take the new interest rate (\(r\)) and apply Formula 8.2. Reapply Formula 8.3 to calculate the interest at this point.

Perform

Step 2:

\(FV\) = $10,000 × (1 + 0.0.0165) × (1 + 0.0275) × (1 + 1.031) × (1 + 1.0245) × (1 + 1.0075) × (1 + 1.004)= $11,159.34255

Step 3:

\(I\) = $11,159.34 − $10,000.00 = $1,159.34 (on April 1, 2011)

Step 4:

December 28, 2011 − April 1, 2011 = 8 complete months = \(t\); \(r\) = 0.65%

\(FV=\$ 11,159.34255(1+0.0065)\left(\dfrac{8}{12}\right)=\$ 11,207.70\)

\(I\) = $11,207.70 − $10,000.00 = $1,207.70 (on December 28, 2011)

Calculator Instructions

| Year | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 2005 | 1 | 1.65 | -10000 | 0 | Answer: 10,165 | 1 | 1 |

| 2006 | \(\surd\) | 2.75 | \(\pm F V\) | \(\surd\) | Answer: 10,444.5375 | \(\surd\) | \(\surd\) |

| 2007 | \(\surd\) | 3.1 | \(\pm F V\) | \(\surd\) | Answer: 10,768.31816 | \(\surd\) | \(\surd\) |

| 2008 | \(\surd\) | 2.45 | \(\pm F V\) | \(\surd\) | Answer: 11,032.14196 | \(\surd\) | \(\surd\) |

| 2009 | \(\surd\) | 0.75 | \(\pm F V\) | \(\surd\) | Answer: 11,114.88302 | \(\surd\) | \(\surd\) |

| 2010 | \(\surd\) | 0.4 | \(\pm F V\) | \(\surd\) | Answer: 11,159.34255 | \(\surd\) | \(\surd\) |

| 2011 Partial Year | \(\surd\) | \(0.65 \times 8 \div 12=\) | \(\pm F V\) | \(\surd\) | Answer: 11,207.69971 | \(\surd\) | \(\surd\) |

If the bond is redeemed on April 1, 2011, it matures at $11,159.34, earning $1,159.34 in interest. If the bond is redeemed on December 28, 2011, it matures at $11,207.70, earning $1,207.70 in interest.

References

- Like interest payout GICs, these R-bonds essentially apply the concepts of simple interest. However, because of the long-term nature of savings bonds, this concept is discussed here instead of with simple interest in Chapters 7 and 8.