10.4: Application - Strip Bonds

- Page ID

- 22127

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)A strip bond is a marketable bond that has been stripped of all interest payments and is one of the many financial tools through which you may earn nontaxable income inside your Registered Retirement Savings Plan (RRSP). A marketable bond is a long-term debt of a corporation or government and represents a means by which large sums of money are "borrowed" from investors. In a marketable bond, interest is regularly paid out to investors. For example, since 1989 Manitoba Hydro has issued over $5.3 billion in bonds. A more detailed discussion on marketable bonds is found in Chapter 14.

Characteristics of Strip Bonds

Mathematically, a strip bond essentially is a long-term version of the treasury bill. Whereas T-bills are found with terms of less than one year, strip bonds have longer terms because of the large sums of money that governments or large corporations require. These large sums take a long time to pay back (think of how long it takes most Canadians to pay off a mortgage, for example). In fact, Canada holds the record of the longest strip bond, with a 99-year term!

Much like T-bills, strip bonds have the following characteristics:

- Strip bonds do not earn interest. They are sold at a discount and redeemed at full value. This follows the line of "buy low, sell high." The compound percentage by which the value of the strip bond grows from sale to redemption is called the yield or rate of return. From a mathematical perspective, you calculate the yield in the exact same manner as an interest rate. Yields are normally specified in nominal form, that is, as a numerical rate followed by words stating the compounding frequency, which is semi-annual unless otherwise specified. Yields remain fixed for the entire term.

- The face value of a strip bond is the maturity value payable at the end of the term. It includes both the principal and yield together.

- Strip bonds are traded between investors at any point in secondary financial markets according to prevailing strip bond rates at the time of sale. Historical strip bond yields can be found at www.bankofcanada.ca/en/rates/yield_curve.html (note that the Bank of Canada refers to strip bonds as zero-coupon bonds). Current yields on strip bonds are found on any online financial source and are usually published daily in the financial sections of newspapers such as the Globe and Mail.

- No minimum investment is required for strip bonds, which are available in any increment of $1.

Purchase Price of a Strip Bond

Strip bonds are financial investment tools that have a known payout (face value) upon maturity. The most common mathematical application involving strip bonds is to calculate the price that must be paid today, or the purchase price, to acquire the strip bond.

The Formula

When you work with strip bonds, you may need up to four formulas that have been previously introduced:

- Formula 8.3 Interest Amount for Single Payments: \(I = FV − PV\)

- Formula 9.1 Periodic Interest Rate: \(i=\dfrac{I Y}{C Y}\)

- Formula 9.2 Number of Compound Periods for Single Payments: \(N = CY × \text {Years}\)

- Formula 9.3 Compound Interest for Single Payments: \(FV = PV(1 + i)^N\)

How It Works

The future value of a strip bond is always known since it is the face value. You calculate the present value or purchase price by applying the following steps:

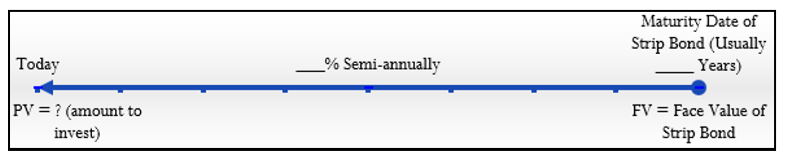

Step 1: Determine the face value (\(FV\)) of the strip bond, the years between the date of the sale and the maturity date (Years), the yield (\(IY\)) on the date of the sale, and the compounding frequency (\(CY\)). If needed, draw a timeline similar to the one below, which illustrates a typical strip bond timeline.

Step 2: Calculate the periodic interest rate (\(i\)) and the number of compounding periods (\(N\)) using Formula 9.1 and Formula 9.2, respectively.

Step 3: Calculate the present value of the strip bond using Formula 9.3, rearranging for \(PV\).

Step 4: If you are interested in the actual dollar amount that the investor gains by holding onto the strip bond until maturity, apply Formula 8.3.

Assume that when prevailing market rates are 4.1153% you want to invest in a $5,000 face value strip bond with 13½ years until maturity. How much money is required to purchase the strip bond today?

Step 1: The known variables are \(FV\) = $5,000, Years = 13½, \(IY\) = 4.1153%, and \(CY\) = 2. The timeline illustrates the strip bond.

Step 2: The periodic interest rate is \(i\) = 4.1153%/2 = 2.05765%. The number of compounding periods remaining on the strip bond is \(N\) = 2 × 13½ = 27.

Step 3: The present value or purchase price of the strip bond is calculated as \(\$5,000 = PV(1 + 0.0205765)^{27}\) or \(PV\) = $2,884.96. Thus, you can purchase the strip bond for $2,884.96

Step 4: If you hold onto the strip bond for the remaining 13½ years, you will receive $5,000 upon maturity. This represents a gain of \(I\) = $5,000.00 − $2,884.96 = $2,115.04 over the term of the investment.

Things To Watch Out For

Don't forget that the compounding on strip bonds is assumed to be semi-annual unless stated otherwise. Thus, \(CY\) = 2 in most scenarios.

- If the yield remains constant, what is the relationship between the purchase price of a strip bond and the time to maturity?

- What happens to the purchase price of a strip bond if the yield increases while the time to maturity remains constant?

- Answer

-

- The longer the strip bond needs to be discounted, the lower the purchase price becomes; the shorter the time to maturity, the greater the purchase price.

- The purchase price becomes lower since the future value is discounted using a higher yield

Johansen is considering purchasing a $50,000 face value Government of Canada strip bond with 23½ years until maturity. The current market yield for these bonds is posted at 4.2031%. What is the price of the strip bond today, and how much money is gained if the bond is held until maturity?

Solution

Calculate the purchase price (\(PV\)) of the strip bond today along with the total interest (\(I\)).

What You Already Know

Step 1:

The face value, years to maturity, and nominal interest rate are known: \(FV\) = $50,000, Years = 23.5, \(IY\) = 4.2031%, \(CY\) = default = semi-annual = 2

How You Will Get There

Step 2:

Apply Formula 9.1 and Formula 9.2.

Step 3:

Apply Formula 9.3 and rearrange for \(PV\).

Step 4:

To calculate the total gain, apply Formula 8.3.

Perform

Step 2:

\(i=\dfrac{4.2031 \%}{2}=2.10155 \%\), \(N\) = 2 × 23.5 = 47

Step 3:

\(PV=\$ 50,000(1+0.0210155)^{-47}=\$ 18,812.66\)

Step 4:

\(I\) = $50,000 − $18,812.66 = $31,187.34

Calculator Instructions

| N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|

| 47 | 4.2031 | Answer: -18,812.66199 | 0 | 50000 | 2 | 2 |

The strip bond has a purchase price of $18,812.66 today. If you hold onto the strip bond until maturity, you will receive a payment of $50,000 23½ years from today. This represents a $31,187.34 gain.

Nominal Yields on Strip Bonds

In two instances it is common to calculate the nominal yield on strip bonds:

- At times, various newspapers or online sites may list a purchase price per $100 of face value but not actually publish the yield on the strip bond. A smart investment decision always requires you to know the interest rate being earned.

- Strip bonds are actively traded on a market. Many investors sell strip bonds to other investors prior to maturity. In these cases, the investor selling the bond needs to calculate the actual yield realized on the investment.

To calculate nominal yields you need the same four formulas as for the strip bond's purchase price.

How It Works

Follow these steps to calculate the nominal yield of a strip bond:

Step 1: How much was paid for the strip bond? Determine the present value or purchase price of the strip bond (\(PV\)). This may already be known, or you may have to calculate this amount using the previously introduced steps for calculating the present value.

Step 2: How much did the strip bond sell for? This is the future value (\(FV\)) of the strip bond. If it is the maturity of the strip bond, then the future value is the face value of the bond. If the investor is selling the strip bond prior to maturity, then this number is based on a present value calculation using the yield at the time of sale and time remaining until maturity.

Step 3: Determine the years (Years) between the purchase and the sale of the strip bond. Using \(CY\) = 2 (unless otherwise stated), apply Formula 9.2 and calculate the number of compounding periods between the dates (\(N\)).

Step 4: Calculate the periodic interest rate (\(i\)) using Formula 9.3, rearranging for \(i\).

Step 5: Convert the periodic interest rate to its nominal interest rate by applying Formula 9.1 and rearranging for \(IY\).

Step 6: If you are interested in the actual dollar amount that the investor gained while holding the strip bond, apply Formula 8.3.

Assume that when market yields were 4.254% an investor purchased a $25,000 strip bond 20 years before maturity. The purchase price was $10,772.52. The investor then sold the bond five years later, when current yields dropped to 3.195%. The selling price was $15,539.94. The investor wants to know the gain and the actual yield realized on her investment.

Step 1: The \(PV\) is known at $10,772.52. This is the purchase price paid for the strip bond.

Step 2: The \(FV\) is known at $15,539.94. This is the selling price received for the strip bond.

Step 3: Between the purchase and sale, the Years = 5. With \(CY\) = 2, the strip bond was held for \(N\) = 2 × 5 = 10 compounding periods.

Step 4: Applying Formula 9.3, \(\$15,539.94 = $10,772.52(1 + i)^{10}\) or\(i\) = 0.037321.

Step 5: Converting to the nominal rate, \(0.037321 = IY ÷ 2\) or \(IY\) = 7.4642%.

Step 6: The actual gain is \(I\) = $15,539.94 − $10,772.52 = $4,767.42.

The investor gained $4,767.42 on the investment, representing an actual yield of 7.4642% compounded semiannually.

Important Notes

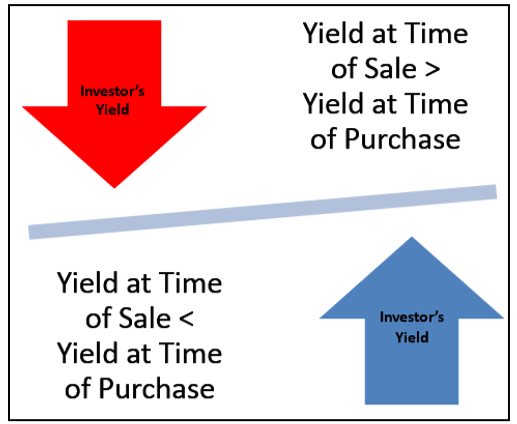

The relationship between the yield at which you purchased the strip bond versus the current yield in the market at the time of sale is illustrated in the figure below.

Each relationship illustrated in the figure is discussed below:

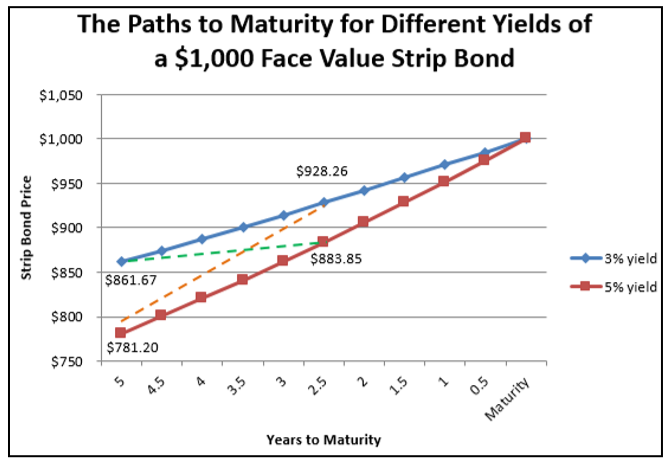

Current Yield > Purchase Yield. If the current yield is higher at the time of sale than the yield at time of purchase, then the strip bond price at the time of sale is pushed downward from the original path to maturity. Consider two situations to illustrate this point, demonstrated in the figure on the next page. If $1,000 is present valued over five years at a 3% semi-annual yield, the price is $861.67. At a 5% semi-annual yield, the same strip bond would have a lower price of $781.20. In both of these cases, though, as the time of sale advances toward the maturity date over the next five years, the prices will gradually increase toward $1,000. However, the price of the 5% yield strip bond will always be lower than that of the 3% strip bond. Thus, if you purchase a 3% strip bond and sell when yields are 5%, the original sale price is lowered from the blue line to the red line. Thus, if the sale occurs with 2.5 years remaining until maturity, the price drops from $928.26 to $883.85. Since the future value drops, the actual investor's yield will become lower than the original purchase yield (as reflected by the dashed green arrow).

Current Yield < Purchase Yield. If the current yield is lower at the time of sale than the yield at the time of purchase, then correspondingly the strip bond price at the time of sale is pushed upward from the original path to maturity. Using the same example from above, recall that the price on the 3% yield strip bond is always higher than the 5% yield strip bond. Thus, if you had purchased the strip bond when yields were 5%, selling the strip bond when yields are 3% means that the future value jumps upward from the red line to the blue line. Thus, if the sale occurs with 2.5 years remaining until maturity, the price increases from $883.85 to $928.26. Therefore, the actual investor's yield will become higher than the original purchase yield (as reflected by the dashed orange line). This concept is exemplified by the investor above. She originally purchased when discount rates were 4.254% and sold when rates had dropped to 3.195%. This increased the sale price of her strip bond and translated into the investor actually realizing 7.4642% instead of the original yield of 4.254%!

In each of the following situations, determine whether the investor achieves a yield higher than, lower than, or equal to the yield at the time of purchase.

- Yield at time of purchase = 5.438%; Yield at time of sale = 6.489%

- Yield at time of purchase = 2.888%; Yield at time of sale = 2.549%

- Yield at time of purchase = 4.137%; Yield at time of sale = 4.137%

- Answer

-

- Lower than; current yield > purchase yield.

- Higher than; current yield < purchase yield.

- Equal to; both yields are the same.

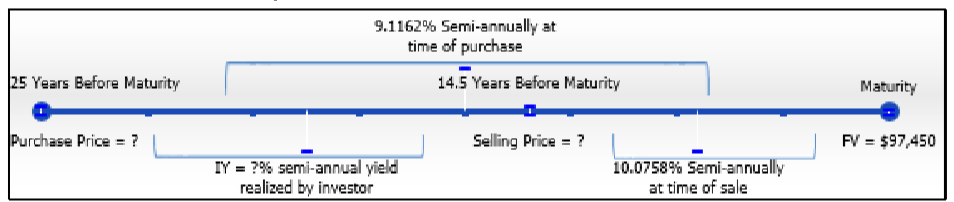

Cameron invested in a $97,450 face value Government of British Columbia strip bond with 25 years until maturity. Market yields at that time were 9.1162%. Ten and half years later Cameron needed the money, so he sold the bond when current yields were 10.0758%. Calculate the actual yield and gain that Cameron realized on his investment.

Solution

Calculate the nominal interest rate (\(IY\)) that Cameron realized while in possession of the strip bond. Also calculate the total gain (\(I\)).

What You Already Know

The following information is known about the bond at the time of purchase:

\(FV\) = $97,450, Years = 25, \(IY\) = 9.1162%, \(CY\) = 2

The following information is known about the bond at the time of sale:

Years strip bond held = 10.5, \(FV\) = $97,450, \(CY\) = 2, Years = 25 − 10.5 = 14.5, \(IY\) = 10.0758%

How You Will Get There

Step 1:

To figure out the purchase price, apply Formula 9.1, Formula 9.2, and Formula 9.3 based on the purchase date.

Step 2:

To figure out the selling price, apply Formula 9.1, Formula 9.2, and Formula 9.3 based on the selling date. Note that once the \(PV\) is calculated, it becomes the \(FV\) for subsequent calculations.

Step 3:

Taking the years the strip bond was held, apply Formula 9.2 to determine the number of compounding periods.

Step 4:

Calculate the periodic interest rate by applying Formula 9.3, rearranging for \(i\).

Step 5:

Calculate the nominal interest rate by applying Formula 9.1, rearranging for \(IY\).

Step 6:

Calculate the total gain by applying Formula 8.3.

Perform

Step 1:

\(i\) = 9.1162%/2 = 4.5581%; \(N\) = 2 × 25 = 50

\[\begin{aligned}

\$ 97,450 &=PV(1+0.045581)^{50} \\

PV &=\$ 97,450 \div 1.045581^{50}\\

&=\$ 10,492.95

\end{aligned} \nonumber \]

Step 2:

\(i\) = 10.0758%/2 = 5.0379%; \(N\) = 2 × 14.5 = 29

\[\begin{aligned}

\$ 97,450 &=PV(1+0.050379)^{29} \\

PV &=\$ 97,450 \div 1.050379^{29}\\

&=\$ 23,428.63

\end{aligned} \nonumber \]

Step 3:

\(CY\) = 2; \(N\) = 2 × 10.5 = 21

Step 4:

\(PV\) = $10,492.95; \(FV\) = $23,428.63

\[\begin{aligned}

\$ 23,428.63 &=\$ 10,492.95(1+i)^{21} \\

i &=\left(\dfrac{\$ 23,428.63}{\$ 10,492.95}\right)^{\frac{1}{21}}=0.038991

\end{aligned} \nonumber \]

Step 5:

0.038991 = \(IY\) ÷ 2 or \(IY\) = 0.038991 × 2 = 7.7982%

Step 6:

\(I\) = $23,428.63 − $10,492.95 = $12,935.68

Calculator Instructions

| Step | N | I/Y | PV | PMT | FV | P/Y | C/Y |

|---|---|---|---|---|---|---|---|

| 1 | 50 | 9.1162 | Answer: -10,492.95246 | 0 | 97450 | 2 | 2 |

| 2 | 29 | 10.0758 | Answer: -23,428.63365 | \(\surd\) | \(\surd\) | \(\surd\) | \(\surd\) |

| 4 and 5 | 21 | Answer: 7.798240 | -10492.95 | \(\surd\) | 23428.63 | \(\surd\) | \(\surd\) |

Cameron sold the strip bond when prevailing market rates were higher than the rate at the time of purchase. He has realized a lower yield of 7.7982% compounded semi-annually, which is a gain of $12,935.68.