15.S: Summary

- Page ID

- 22161

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Key Concepts

Section 15.1: Net Present Value (What Is the Value of My Decision?)

- The characteristics of making decisions including decision types, monetary sources, and interest rates

- Making decisions through net present value

- Handling calculations involving regular cash flows

- Making multiple choices when resources are limited

Section 15.2: Other Measures for Making Decisions (How Else Can I Do It?)

- Choosing between projects of different lengths

- Using internal rate of return to choose whether to pursue one course of action

The Language of Business Mathematics

- cash flow

- A movement of money into or out of a particular project

- cost of capital

- A weighted average of all of the debt and equity financing rates used to provide needed funds for a project.

- equivalent annual cash flow

- An annual annuity payment amount that, when present valued using the cost of capital, arrives at the same \(NPV\) as all of the original cash flows.

- hard capital rationing

-

A process that requires the calculation of the net present value for each possible project and then the allocation of limited capital resources to these projects efficiently to maximize the combined net present value.

- internal rate of return (IRR)

- The annual rate of return on the investment being made such that the net present value of all cash flows in a particular project equals zero.

- net present value (NPV)

- The difference in today's dollars between all benefits and costs for any given project.

The Formulas You Need to Know

Symbols Used

\(NPV\) = net present value

\(NPV_{RATIO}\) = net present value ratio

\(CF_o\) = initial cash flow

Formulas Introduced

Formula 15.1 Net Present Value: \(\text { NPV }=\text { (Present Value of All Future Cash Flows) - (Initial Investment) }\)

Formula 15.2 Net Present Value Ratio: \(\mathrm{NPV}_{\mathrm{RATIO}}=\dfrac{\mathrm{NPV}}{\mathrm{CFo}}\)

Technology

Calculator

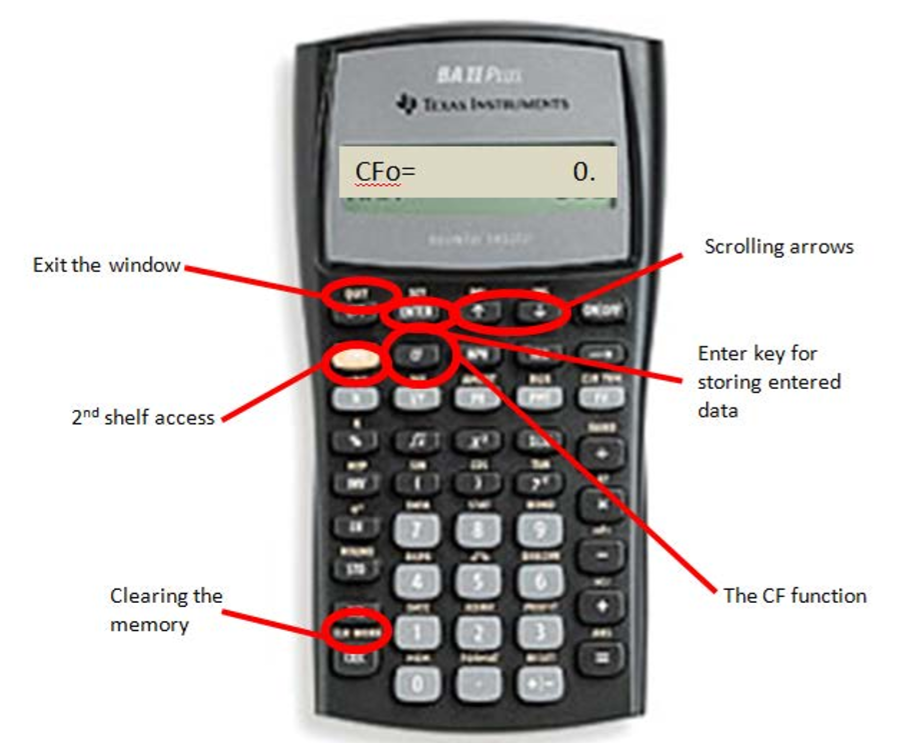

Cash Flow Worksheet (\(CF\))

- Access the cash flow function by pressing \(CF\) on the keypad.

- Always clear the memory using 2nd CLR Work so that any previously entered data is deleted.

- Use the ↑ and ↓ arrows to scroll through the various lines.

- Strictly adhere to the cash flow sign convention when using this function and press Enter after keying in the data.

- To exit the window, press 2nd Quit.

The various lines are summarized below:

- \(CF_o\) = any cash flow today.

- \(CXX\) = a particular cash flow, where \(XX\) is one of a series of cash flow numbers starting with 01. You must key in cash flows in order from the first time segment to the last. You cannot skip a time segment, even if it has a value of zero, because each time segment is a placeholder on the timeline.

- \(FXX\) = the frequency of a particular cash flow, where XX is the cash flow number. It is how many times in a row the corresponding cash flow amount occurs. This allows you to enter recurring amounts together instead of keying them in separately. By default, the calculator sets this variable to 1.

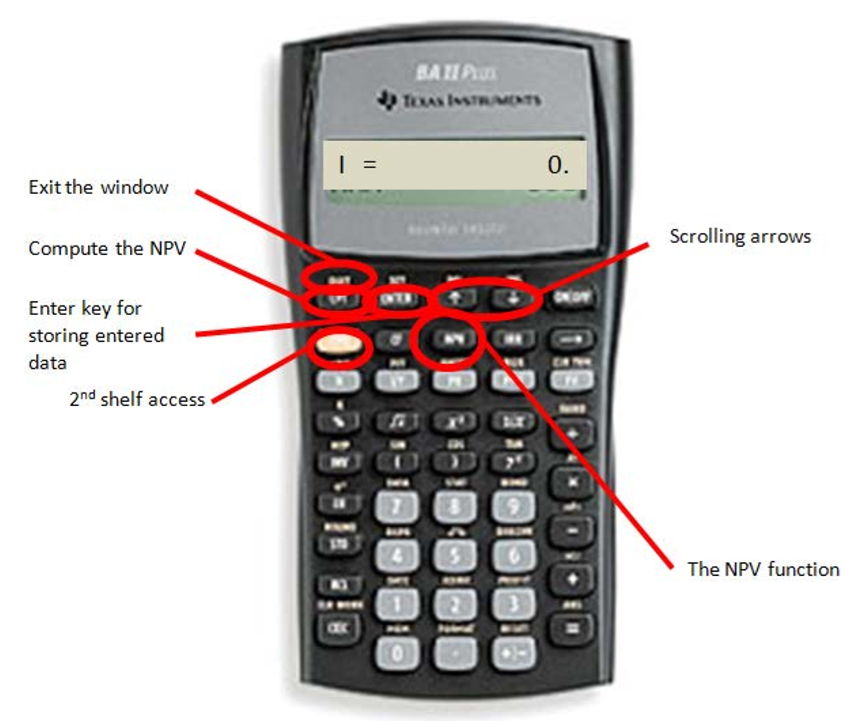

Net Present Value (\(NPV\))

- Use this function after you have entered all cash flows.

- Press \(NPV\) on the keypad to access the function.

- Use the ↑ and ↓ arrows to scroll through the window.

- To exit the window, press 2nd Quit.

This window has two lines:

- \(I\) = the matching periodic interest rate for the interval of each time segment.

- \(NPV\) = the net present value. Press CPT to calculate this amount.

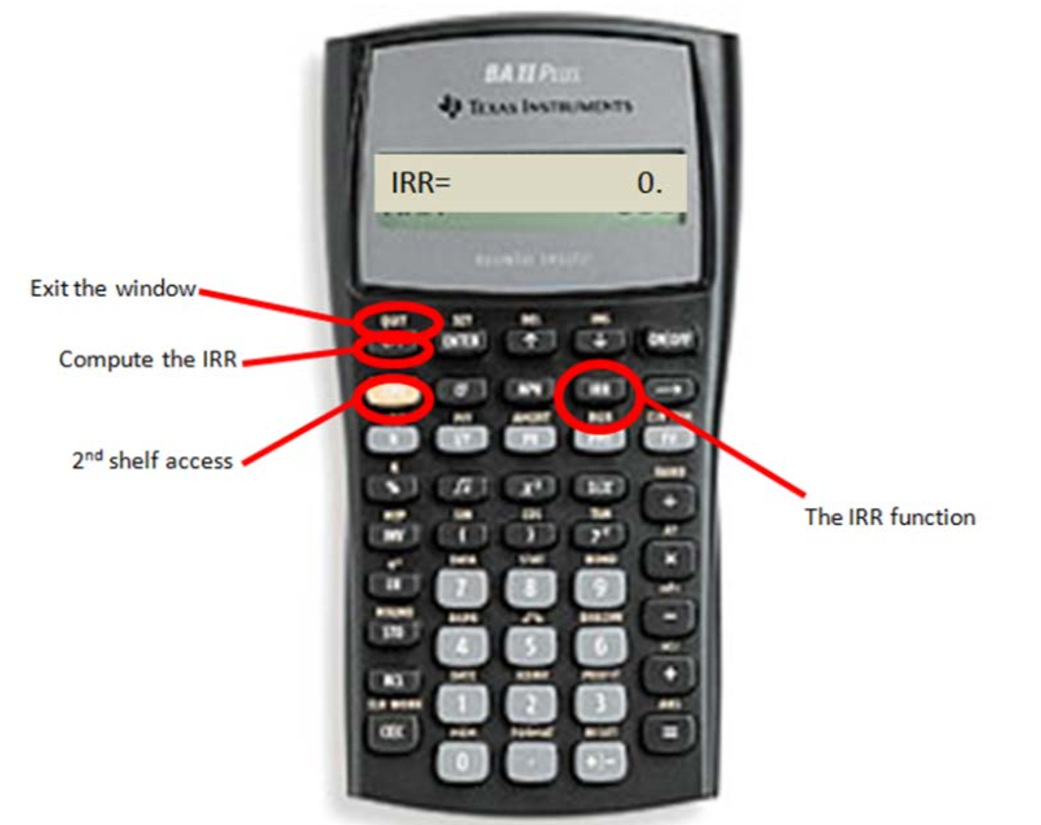

Internal Rate of Return (IRR)

- Use this function after you have entered all cash flows.

- Press IRR on the keypad to access the function.

- Press CPT button to perform the calculation. The output is in percent format.

- To exit the window, press 2nd Quit.