19.3: Introduction to Markov Models

- Last updated

- Sep 17, 2022

- Save as PDF

( \newcommand{\kernel}{\mathrm{null}\,}\)

Login with LibreOne to run this code cell interactively.

If you have already signed in, please refresh the page.

from urllib.request import urlretrieve

urlretrieve('https://raw.githubusercontent.com/colbrydi/jupytercheck/master/answercheck.py',

'answercheck.py');

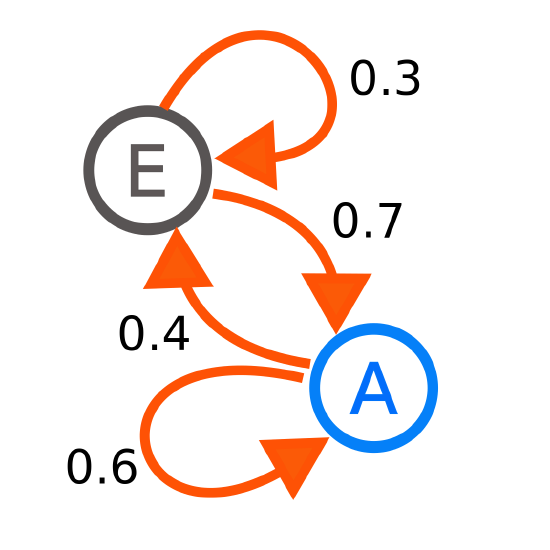

In probability theory, a Markov model is a stochastic model used to model randomly changing systems. It is assumed that future states depend only on the current state, not on the events that occurred before it.

Each number represents the probability of the Markov process changing from one state to another state, with the direction indicated by the arrow. For example, if the Markov process is in state A, then the probability it changes to state E is 0.4, while the probability it remains in state A is 0.6.

The above state model can be represented by a transition matrix.

At each time step (t) the probability to move between states depends on the previous state (t−1):

At=0.6A(t−1)+0.7E(t−1)

Et=0.4A(t−1)+0.3E(t−1)

The above state model (St=[At,Et]T) can be represented in the following matrix notation:

St=PS(t−1)

Create a 2×2 matrix (P) representing the transition matrix for the above Markov space.

Login with LibreOne to run this code cell interactively.

If you have already signed in, please refresh the page.

#Put your answer to the above question here

Login with LibreOne to run this code cell interactively.

If you have already signed in, please refresh the page.

from answercheck import checkanswer checkanswer.matrix(P,'de1c99f4b4a8d7ea541a084d836ba7e4');